Claude and an 80 year old man (almost)

Howard Marks' thoughts on AI, my thoughts on Howard Marks, and a stock analysis competition between me and AI

A sequel to “I had lunch with a cinema owner.”

Since we are talking about the use of AI in my line of work, I would like to preface this write up by clearly communicating what this write up is not.

It is not an expert opinion about how the investment industry is going to take shape in the future

It is not an editorial whether AI will replace more knowledge workers in Jakarta

It is also not about financial advice as there will be a brief discussion about a stock research that was conducted using AI.

You can treat this writeup as a data point for how AI is currently used by Co-Founder of an early stage wealth tech startup in Indonesia.

With that, let’s get cracking.

There is a wise 80 year old man

Who likes to write memos documenting his thoughts embroided with his investing philosophy that he has accumulated for more than 5 decades. He manages close to $200 billion of funds and he generously publishes his thoughts to the public free of charge. One day, a fellow value investor shared with me his most recent memo. He writes a memo about his experience using Claude. I dropped everything and went on to read what he has to say.

In his latest memo, Howard Marks describes asking Claude to write him a tutorial about AI. What came back was 10,000-word essay that referenced his past memos, anticipated counterarguments and Claude even sprinkled humor here and there. I couldn’t imagine being in his shoes, witnessing the amount of technological progress in his life time. I mean he was born in an era where digital photography was not invented yet. Now he is dealing with a machine that writes a note as good as what a competent colleague would do.

But Marks being Marks, did not stop at awe. He pushes further. He questions deeply into what is the likely implication of AI to the field of investing. If AI is so good at gathering and synthesizing data, is there a place for mere mortals like Toby and Budi?

Note: Marks didn’t say Toby and Budi in the memo because we are really just mere mortals

Well the answer comes from a person who studies the spread of diseases, an epidemiologist Marc Lipsitch. He observed that humans make decision using three core components:

Facts,

Informed extrapolation from analogies to prior experience, and

Opinion or speculation

Marks is saying that AI is beyond this world for (1) and (2). Perhaps even better than any human alive. Just like Stockfish (the chess AI) is better than Magnus Carlsen. But he says that AI is genuinely weaker in novel situations. In other words, AI is probably not as good as humans who have lived experience with minimal data in the internet (information used to train AI models).

He further went on to say that humans (at least the best humans) still hold an edge in situations that are genuinely novel, where there is no historical pattern to rely on.

But here is what I kept thinking about after reading the memo.

If AI is this impossible to beat at facts and extrapolation, shouldn’t we trust its opinion too? It does not have anchoring bias. It does not have fear or greed. It does not hold onto a losing position because its ego cannot stomach the loss. It is not swayed by narratives — the very thing Shiller described to us in Part 1.

In the mean time, look at us. Look at the quality of judgment that human beings produce. You can think of the decisions made by leaders around the world. We are emotional, inconsistent, stubborn. We lie to ourselves. We hold onto beliefs long after data and evidence proves them wrong.

So how would humans, a being this flawed, stand a chance in having superior taste, judgement and opinion?

I didn’t fully understand what Marks said.

But above all, I was feeling very competitive. I grew up in a Singaporean kiasu (fear of losing) culture and I simply didn’t want to lose out to this 80 year old wise person. Prior to reading his memo, I never used Claude before.

So like any other kiasu person, I went on to buy the Claude max plan to give it a spin.

I want to have a better grasp of what does Marks mean. So I started where any kiasu person would start.

I wanted to test how far AI can actually go in my work. Not in theory. But in practice, on a real stock that I was actually studying. And I want to be honest — part of me was hoping AI would just be better. That would make my life a lot easier.

The company that I studied was Sarana Menara Nusantara (TOWR)

TOWR is Indonesia’s largest independent owner and operator of telecommunications infrastructure. A Djarum owned company, it owns about 30,000 towers across the country and leases space on them to telco operators like Telkomsel, Indosat, and XL. The tenants install their antennas and equipment on the tower, pay rent, and the contracts are locked in for 10 years. It is a beautifully predictable business.

The current factor that is driving TOWR’s profitability

Aside from average selling price of the lease agreements (which is not the focus in today’s discussion), is also TOWR’s colocation model. Being an independent telco tower operator, TOWR is able to host more than 1 tenants in its infrastructure (example tenants are Telkomsel, XL and Indosat).

Now the capital expenditure for having 1 tenant is large, as you have to either build a new one or acquire towers from existing industry players (TBIG is also in the same industry). But an additional tenant at the same tower involves minimal capital expenditure which has a direct contribution to its profitability. You can imagine getting additional revenue without most of its expense. It would go straight down to profits.

So to repeat, having an additional tenant or a high tenancy ratio (average number of tenants per tower) is highly desirable for the company as it is associated with higher profitability.

But of course, the market has largely been harsh.

You could see below that the price of the share has seen a 60% drop in the last 5 years as this post was written. Markets might be harsh because TOWR might be seen as having an obsolete business especially because telco companies will have lesser need of those towers.

But there’s another phenomenon that might cause immediate headwind to TOWR’s profitability that the market does not like.

Consolidation, consolidation

To give you more context, the telco industry in Indonesia has seen multiple consolidations in the past 5 years. Starting with Indosat and Hutchinson’s merger in 2022. And the most recent merger of XL and FREN back in April 2025.

Why events such as this is pertinent to TOWR’s profitability?

I suspect the answer is because consolidations would reduce tenancy ratio (discussed above). Usually we had 5 telco players prior to the consolidation. Now that we have 3, the merged telco companies no longer need to rent the same tower space.

So of course, tenancy ratio has dropped for the past few years from 1.88 in 2021 to 1.61 in 2025.

So the question: now that there was a recent merger of FREN and XL in 2025, how bad will tenancy ratio actually get, and for how long?

My plan is simple

I want to use AI to help me use Agent Based Modelling and Monte Carlo Simulation technique to model out the probable tenancy ratio outcomes.

For those unfamiliar,

Agent Based Modelling

is the idea that instead of modelling an entire system with a single math equation, you model the individual pieces and let the system emerge from their interactions.

In TOWR’s case, each tower is an “agent” with its own characteristics. Location (urban, suburban, rural), whether it has fibre connectivity, how many tenants it currently has, how much exposure it has to the merging operator.

You give each tower a set of probabilities (chance of gaining a tenant, chance of losing one, chance of getting 5G equipment) and then let all 30,000 of them play out over a period of time. The system-level result — the tenancy ratio — emerges from 30,000 individual stories, not from a top-down assumption.

Monte Carlo Simulation

is the idea that you run the same model hundreds of times, each time with slightly different random outcomes, to see the range of what could happen. Think of it like rolling dice 200 times and tracking the results. Any single roll tells you nothing. Two hundred rolls give you a distribution, what’s likely and what’s extreme.

Combine the two: 30,000 towers, each with their own probabilities, simulated 200 times per scenario. That gives you a probability distribution of where the tenancy ratio might land — not a point estimate, but a range of possible outcomes.

Now here’s where it gets interesting.

Building the model was the easy part. AI handled that quite nicely. The hard part was...

Claude was impressive

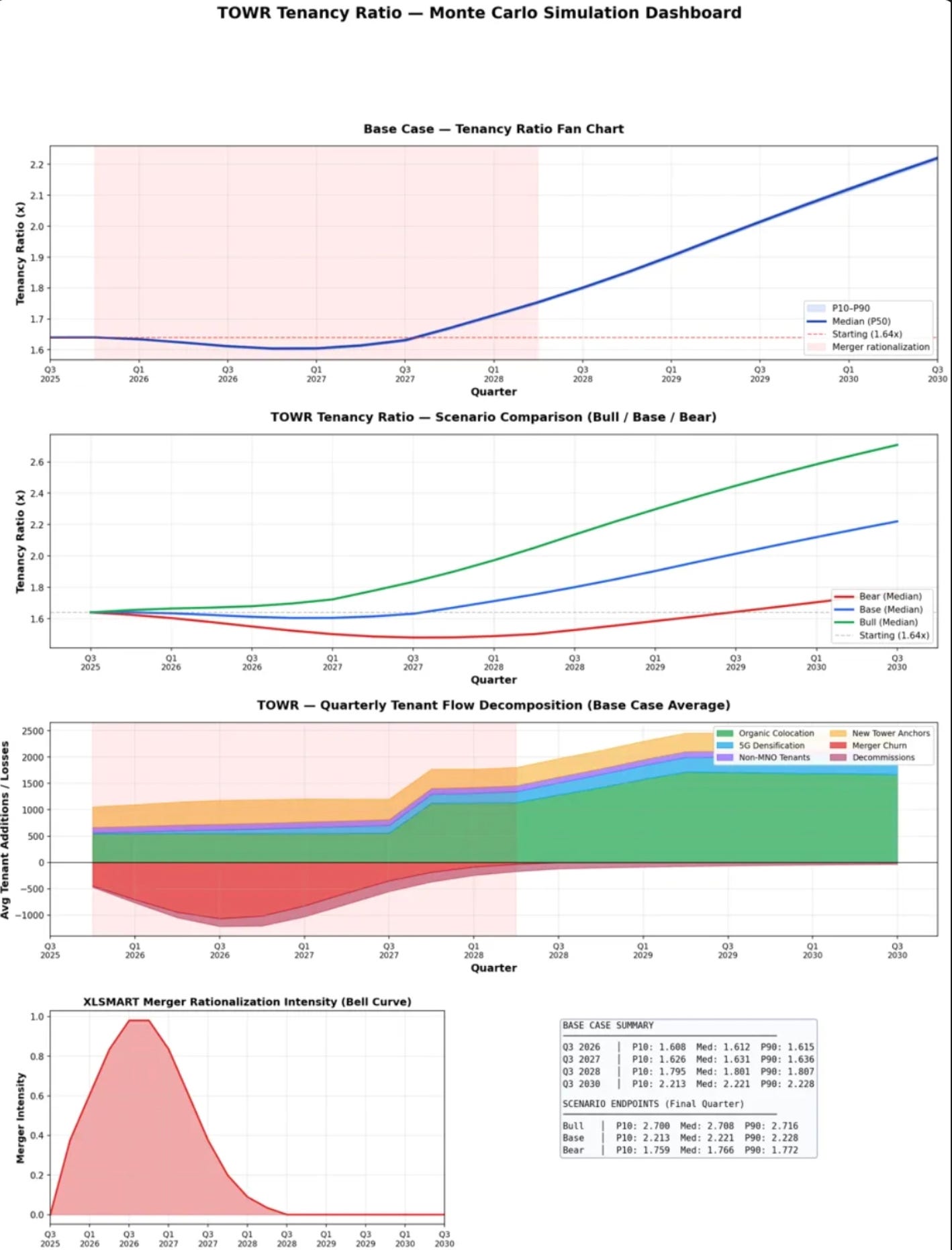

It built the entire agent-based model. It ran simulations and produced charts with confidence bands. If you saw the output, you would genuinely think a quant team produced it. Take a look.

So I started looking at the parameters. One of the key inputs was the organic colocation rate — how often a tower gains a new tenant through normal business activity.

Claude estimated this by looking at 2024 data: TOWR added 3,751 tenants across roughly 30,000 towers. That gives you about 2.5% per quarter, which makes sense.

But something about 2024 felt off. I remembered reading TOWR had acquired a competing tower company called IBST in 2024. So I went to NotebookLM — which had the actual company filings loaded — and asked it to separate the organic additions from the acquired ones.

Turns out, a significant chunk of those 3,751 tenants came from the IBST acquisition. They were bought, not won (organic). So Claude had used a contaminated year to set one of the most sensitive parameters in the entire model.

The corrected organic rate was closer to 1.0% per quarter (originally was 2.5%), which is a big shift. That single number meaningfully changed the five-year trajectory of the tenancy ratio.

But the assumptions underneath were wrong. And they were wrong in ways that sounded right.

Here’s another one. The model assumed that when the merged telco operator (XLSMART) decommissions a redundant tower, about 60% of the time they would relocate their equipment to an existing TOWR tower nearby. That sounds reasonable — why build a new tower if there’s already one available?

But it turns out TOWR has a strict no-discount policy. Whether you colocate onto an existing tower or order a brand new one, you pay the same rate. So the operator has zero financial incentive to compromise on location. They always choose the network-optimal spot, which usually means a new build. The actual number was closer to 25% colocating onto existing towers, not 60%.

Nobody would know this from the outside. It is buried in how TOWR structures its commercial relationships. NotebookLM surfaced it only because I asked the right question — and I only knew to ask because the economics felt off. Which I also don’t know how to describe myself.

This happened over and over. Non-MNO tenants that I assumed occupied tower space turned out to be purely fibre clients — the parameter should have been zero, not 0.5%. A bell-curve churn shape that I had assumed turned out to be wrong because tower contracts are irrevocable — churn is driven by contract expiry schedules, not operator discretion.

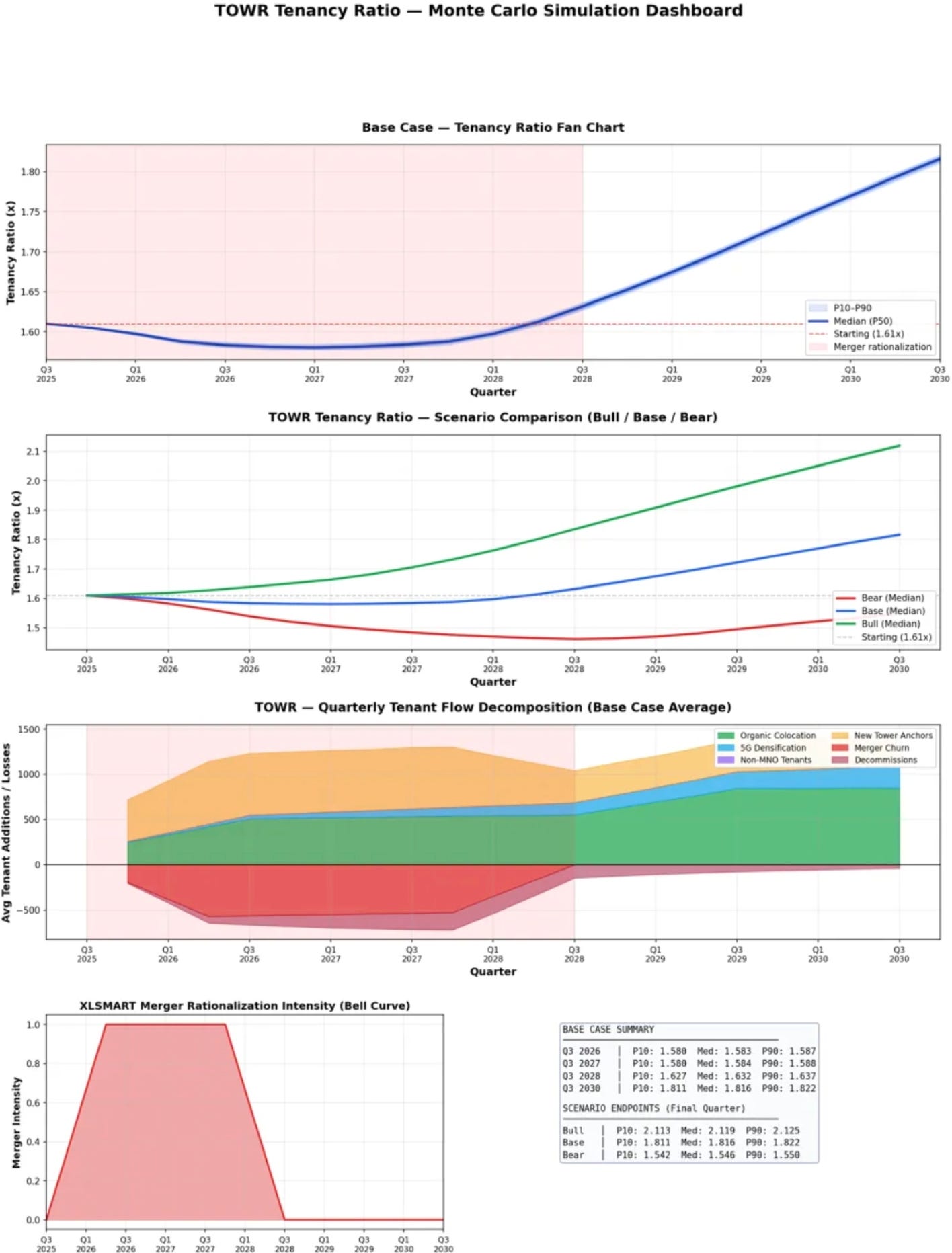

Each correction required me to ask a question that AI did not think to ask itself. And at the end… I got this results.

The results looked nearly identical to the naked eye, yes?

But the assumptions underneath the second picture have been far more closely scrutinised. I challenged every parameter and in many cases corrected them too. The organic colocation rate was halved. The swap ratio was cut by more than half. Non-MNO tenants were zeroed out. The merger intensity was redesigned entirely.

And yet, even after all that work, the interpretation of these results still differs. An AI would present the base case median as the most likely outcome. A cautious analyst might anchor to the bear case. An investor with experience in Indonesian telcos might look at these charts and see something else entirely based on relationships and context that never made it into the model. Which brings me back to the 80 year old man.

Where the human edge actually lives

Remember Marks and the Lipsitch framework? Facts, extrapolation, opinion. AI dominated the first two. The question was whether humans could still be relevant in the third.

After some time of working with Claude and NotebookLM on this analysis, I think I have a bit more understanding of what Marks was saying. It is not that humans have superior opinion. It is that humans have a bit more situated opinion.

We carry context from our own lives that no model has access to.

Every correction I made came from something I already knew or something that felt off based on lived experience or a prior reading that I came across, and so on. Perhaps from knowing what it feels like to lose money after making a wrong bet, that tends to sharpen our instincts all around and then asking the questions that turn out to be important.

So it is not uncommon to ask “are you being optimistic?” on other sub-areas of research.

It came purely from the gut, not analysis.

I don’t think any of this is genius. It is just being aware of context and applying lived experience to what we are studying.

So what helps in the age of AI

I think being hyper observant helps. We have so much lived experience, that is information we can glean right away from our senses. The internet is a huge source of information. But I don’t think it is right to underestimate the wealth of knowledge we get from walking to Indomaret, or travelling out of town from Jakarta to Manado. These experiences can often carry insights to our line of work in ways that is simply unimaginable to an AI.

I also think that willingness to try things is an important one. While researching and understanding a public company is still difficult work and reading convoluted responses of an AI could be tiring. But hey, I don’t have to write a single line of code in doing monte carlo simulations anymore. That’s bananas. AI is certainly helpful in saving huge precious time and allowing my inquiry to be more robust.

Lastly, intellectual honesty would be the most important ingredient. I don’t think there’s a point of being observant, trying new things and then lying to yourself about deriving a conclusion that I myself want to hear. The study should lead to a better understanding which hopefully would bring us to a better decision all around.

Closing remarks

That’s all folks, thanks for reading this far! If you fancy, give Claude or any other AI tools a spin. I am not just curious on how it is helpful in studying a company. But I am also curious how it applies to other lines of work, like healthcare, technology, consumer, anything. So if you are so kind to share your experience, do share them in the comments!

Cheers.

Interesting work on TOWR. My question is how involved is the Indonesian government in encouraging tower sharing? And do you think the ROICs on lower tenancy ratios still strong?

Hi Toby great writing as always! Just read Marks notes on AI hurtles Ahead :). QQ I'm starting to use Claude for researching companies for investing, but haven't tried NotebookLM. Any comparison highlight worth mentioning for these two based on your experience?