Disclaimer: this article is definitely not an investment (buy, sell or hold) recommendation on the said shares that is listed on IDX. It is purely for informational purposes only to illustrate a point about investing in general.

IPO of Gojek-Tokopedia (GOTO) has taken Indonesia and probably the world by storm. It is the largest tech startup in Indonesia that has their stock listed in IDX with a whopping market capitalization of Rp 400T or $25 Bio.

The share price of GOTO when it was first listed was at Rp 338,-. Nominally, this is a small amount which makes buying 100 shares of GOTO rather “affordable” at Rp 338.000,- compared to other bluechip stocks out there. The most natural question to ask is:

Is this share price cheap or expensive?

Unfortunately, we are not going to discuss that here because it tends to be quite subjective. What we are going to discuss is the Book Value of GOTO that is published in IDX media before GOTO was listed.

You can find the prospectus of the shares from IDX website here: https://www.idx.co.id/media/10955/15_goto-prospektus-ipo-2022.pdf

If you take a look at the assets that are owned by GOTO, you can see something that is quite attention grabbing:

Asset as of December 2018: Rp 20.5T

Asset as of December 2019: Rp 21.3T

Asset as of December 2020: Rp 30.1T

Asset as of July 2021: Rp 148.2T

Wow, asset increased almost 5 folds within the span of half a year. What happened? Let’s take a look.

If we look at the non-current asset from the image above as of July 2021, we see that the largest contributor is Goodwill that amounts to Rp 93.8 T. As a perspective, their cash in hand is Rp 20.5T. Another perspective, about 63% of GOTO’s book value is contributed by goodwill. If you include intangible assets, then about 72% GOTO is made up out of intangible assets and goodwill.

How is the Goodwill Calculated and Why is it even there?

Let’s take a look at note 34a to get a glimpse of why the goodwill is there. Page 691-692, lists the business combinations and transactions.

At page 692, there is a business combination that is widely popular TOKO/AKAB. AKAB stands for Aplikasi Karya Anak Bangsa, widely known as Gojek. TOKO is Tokopedia. In that row, you could see the figures such as:

Cash and cash equivalents

Receivables

Assets

Intangible assets

Goodwill

Figure below shows the numbers expressed in million Rupiah:

From this image you can see that Goodwill that arises from Gojek Tokopedia merger is Rp 93.1T which seems to have made its way to the book value of GOTO. There is also Rp 11.1T worth of intangible asset that has the same fine print as the goodwill at point number 1.

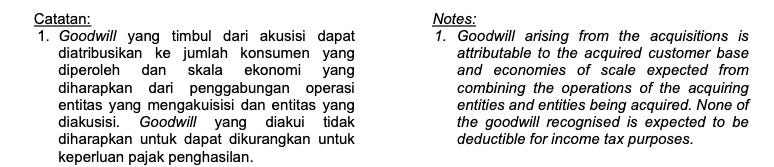

At point number 1, we see the note stating that goodwill arises from acquired customer base and the expectation of economies of scale.

Relative to other goodwill values, the Gojek and Tokopedia merger has by far the largest value which warrants another point number 9 in the notes section.

In short, the explainer says the group (GOTO) has involved an independent evaluator for the identified asset (in this case goodwill and intangible asset) and up until the financial statement was released (before the stock was listed), the analysis has not been completed.

If the analysis has not been completed, there is a chance that the goodwill itself will change in value. In fact, change in value of goodwill or impairment is expected to happen once a year.

As of release of GOTO 2022 financial report, EY has attached their audit response:

We obtained an understanding of the Group’s goodwill impairment analysis process. We evaluated the competence, capabilities, and objectivity of management’s external expert involved in the preparation of the goodwill impairment analysis. We evaluated and tested, with the assistance of our internal expert, the methodology and key assumptions used in the determination of the recoverable amounts of cash-generating units. We also tested the mathematical accuracy of the goodwill impairment analysis prepared by management and the related underlying data used in such analysis. Moreover, we evaluated the related disclosures of goodwill impairment in the accompanying consolidated financial statements

Taken from GOTO Annual Report page 330

What is the value of the goodwill now?

The value now stands at Rp 82.8T which shrinks around Rp 10.3T since the company was listed based on unaudited Q3 2023 financial statement.

What is the reason behind the shrinkage? What is the shrinkage rate going to be like in the coming years? That perhaps will require further research that I might do :)

So what is the point of this blog post?

In this article, we have highlighted that merger of Gojek and Tokopedia has contributed to notable amount of portion of GOTO’s asset from goodwill.

This brings home the point that investing is not 100% science and is subjective.

There is a case to be made that GOTO is an absolutely great investment because of the technological innovation, widespread use and so forth. However, there is another type of investors that perhaps require more clarity in finding out more information about the assets that the company own, including how the goodwill is computed.

Which type of investor are you?