Disclaimer: Everything in this post is written for educational purposes and reflects data available as of July 11, 2026. It is not financial advice, and nothing here is a recommendation to buy, sell, or hold any security. Probability estimates are our own judgment based on public data — please do your own research before making investment decisions.

Update — July 13, 2026: after this post was drafted, S&P completed its scheduled review and affirmed Indonesia at BBB/A-2 with a Stable outlook — projecting ~5.1% growth for 2026, pointing to relatively low government debt and the H1 revenue recovery, and calling the current fiscal and external strains temporary. The JCI rose about 1.9% the next session. We’ve updated the relevant sections below; the rest of the analysis is unchanged.

If your group chats look anything like ours lately, you’ve heard the whisper: Indonesia is about to be labeled “junk.”

The rupiah has broken past 18,000. The stock market, from its peak, has at one point fallen about 40%. And in March, Fitch — one of the three big credit rating agencies — cut its outlook on Indonesia to Negative, weeks after Moody’s did the same. Somewhere between the headlines and the WhatsApp forwards, this has curdled into something close to panic.

So we did the unglamorous thing. We sat down with the actual rulebooks — S&P’s own criteria document, Moody’s official definitions, Fitch’s methodology, and an EU regulation that governs all three agencies — plus the history of every major country that has actually fallen to junk. Then we ran Indonesia through it.

TLDR: the fear is running well ahead of the math. Let’s get into it fellas.

First, what actually happened (and what didn’t)

A sovereign credit rating is basically a report card on one question: how confident are we that this government will pay back its debt?

Somewhere on that report card there’s a line. Above the line, your bonds are called investment grade — safe enough that the world’s most conservative money (pension funds, insurers, central banks) is comfortable holding them. Below the line, you’re in speculative grade — the unflattering nickname is “junk.”

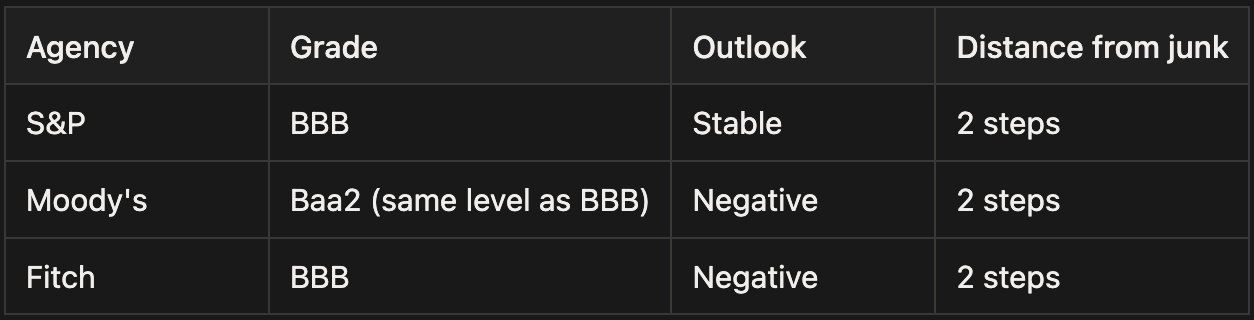

Here’s where Indonesia actually stands today:

Notice two things. First, nobody downgraded Indonesia’s rating. What Moody’s (February 5) and Fitch (March 4) changed was the outlook — the weather forecast, not the weather. The grade itself, BBB, was affirmed by all three agencies — most recently by S&P on July 13, 2026, with its outlook still Stable.

Second, Indonesia sits two full steps above the junk line at all three agencies. Think of it like a football league table: we’re not in the relegation zone. We’re two wins clear of it. What happened this year is that two of the three referees said, “we’re watching you.”

That distinction matters more than anything else in this post.

There’s an actual rulebook for this — and it’s surprisingly strict

Most people imagine rating downgrades as a guy at S&P waking up grumpy one morning because they see unfavourable news on the headline.

The reality is bureaucratic to the point of being boring. And that seems like a good news, because at least boring is more predictable than guessing the mood of an S&P analyst.

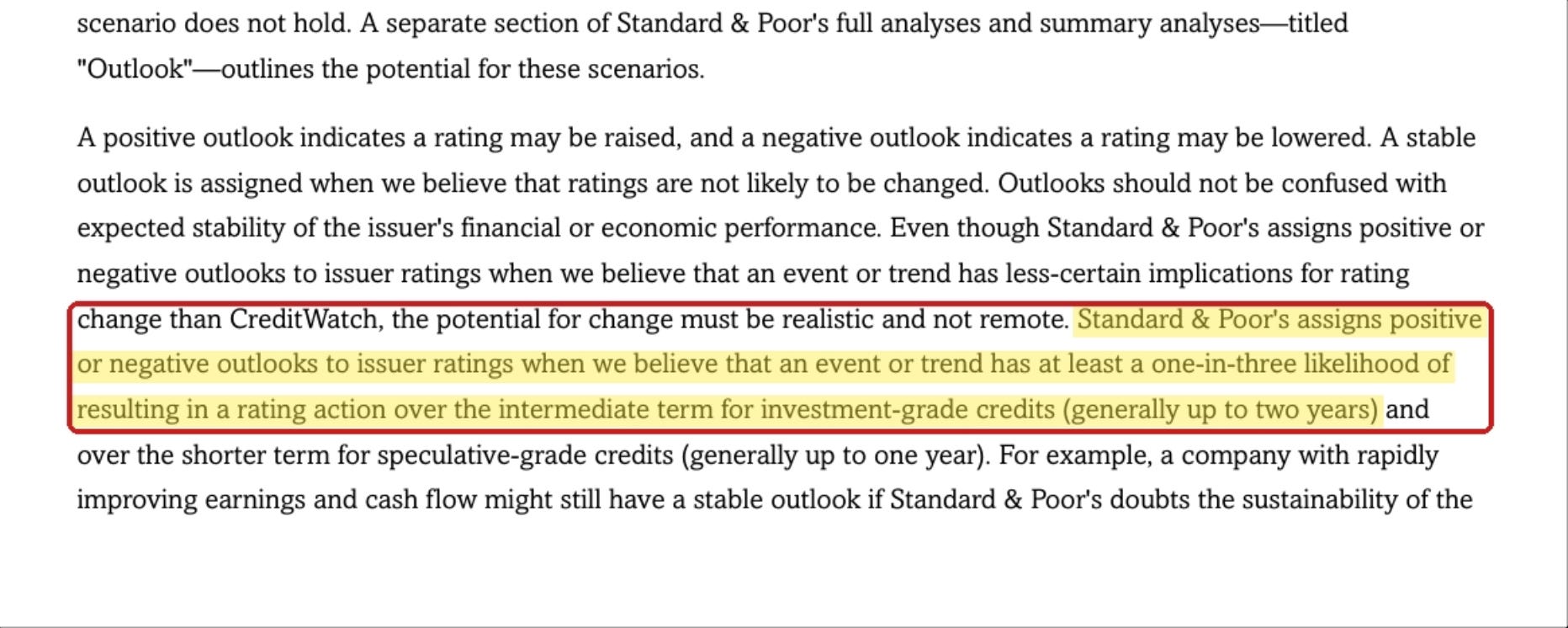

Start with what “Negative outlook” officially means. This is from S&P’s own criteria document, word for word:

“Standard & Poor’s assigns positive or negative outlooks to issuer ratings when we believe that an event or trend has at least a one-in-three likelihood of resulting in a rating action over the intermediate term for investment-grade credits (generally up to two years)...”

Read that carefully. A negative outlook means at least a 1-in-3 chance (33.3%) of a downgrade over roughly two years. Flip it around: even by the agency’s own definition, the more probable outcome is that nothing happens.

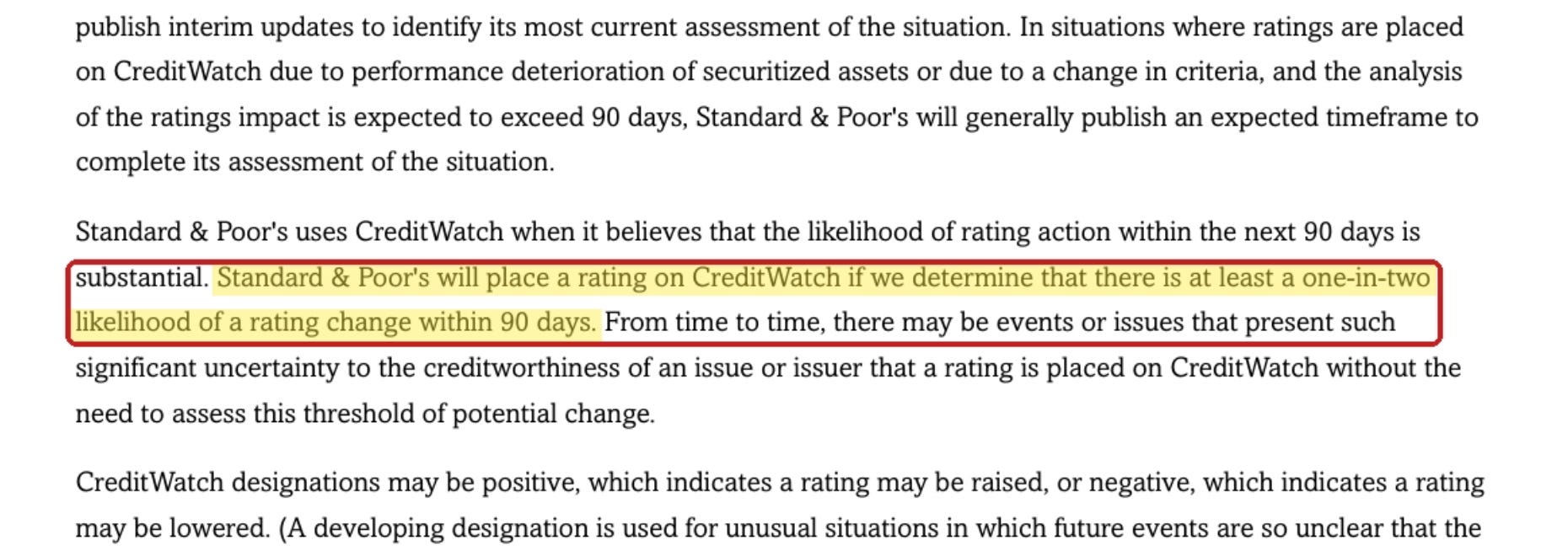

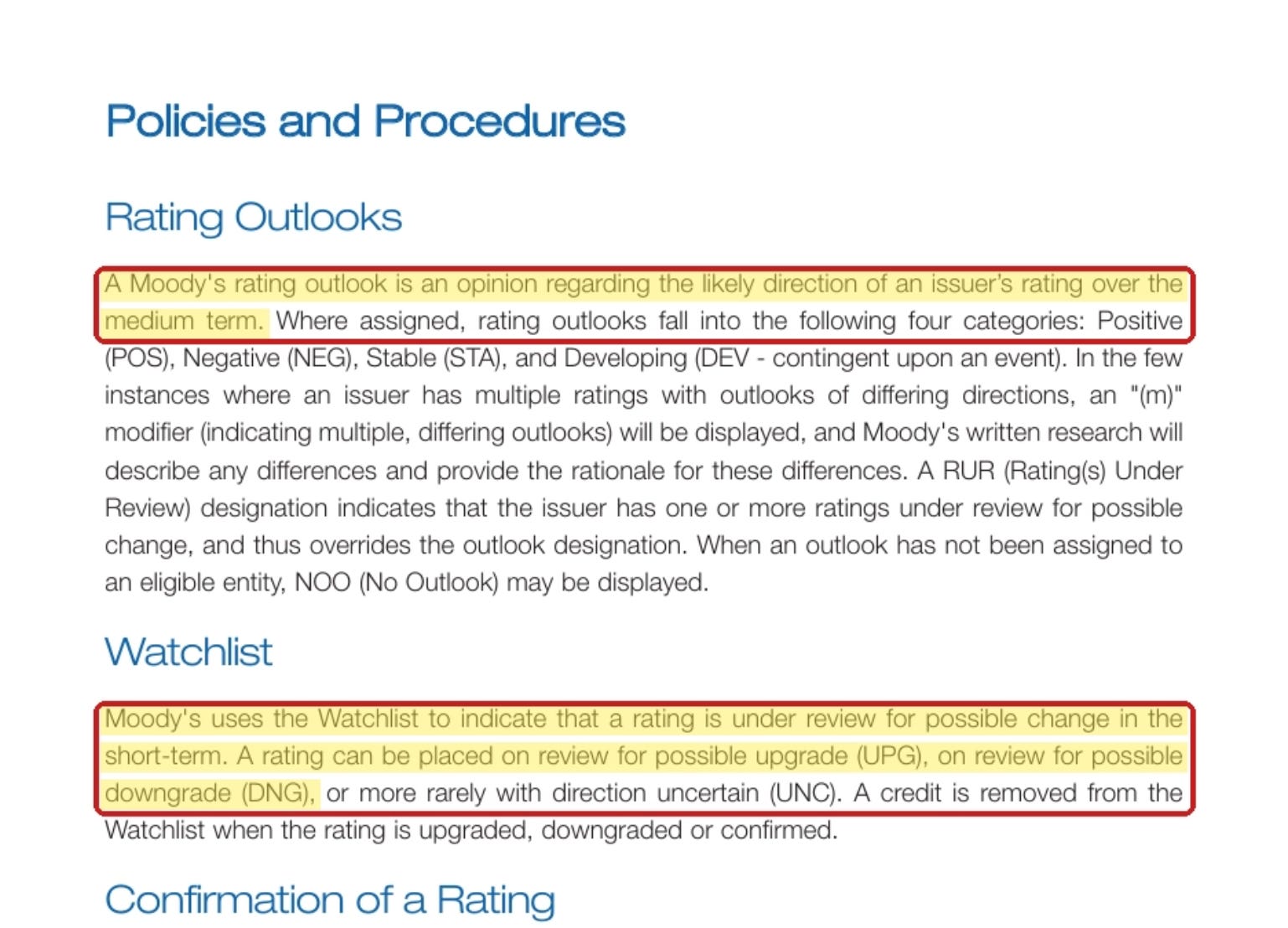

There’s also a more urgent stage called CreditWatch (Moody’s calls it the “Watchlist”) — that’s when a downgrade has at least a 1-in-2 chance within 90 days. Indonesia is not on anyone’s watchlist. We’re at the “stern warning” stage, not the “pack your bags” stage.

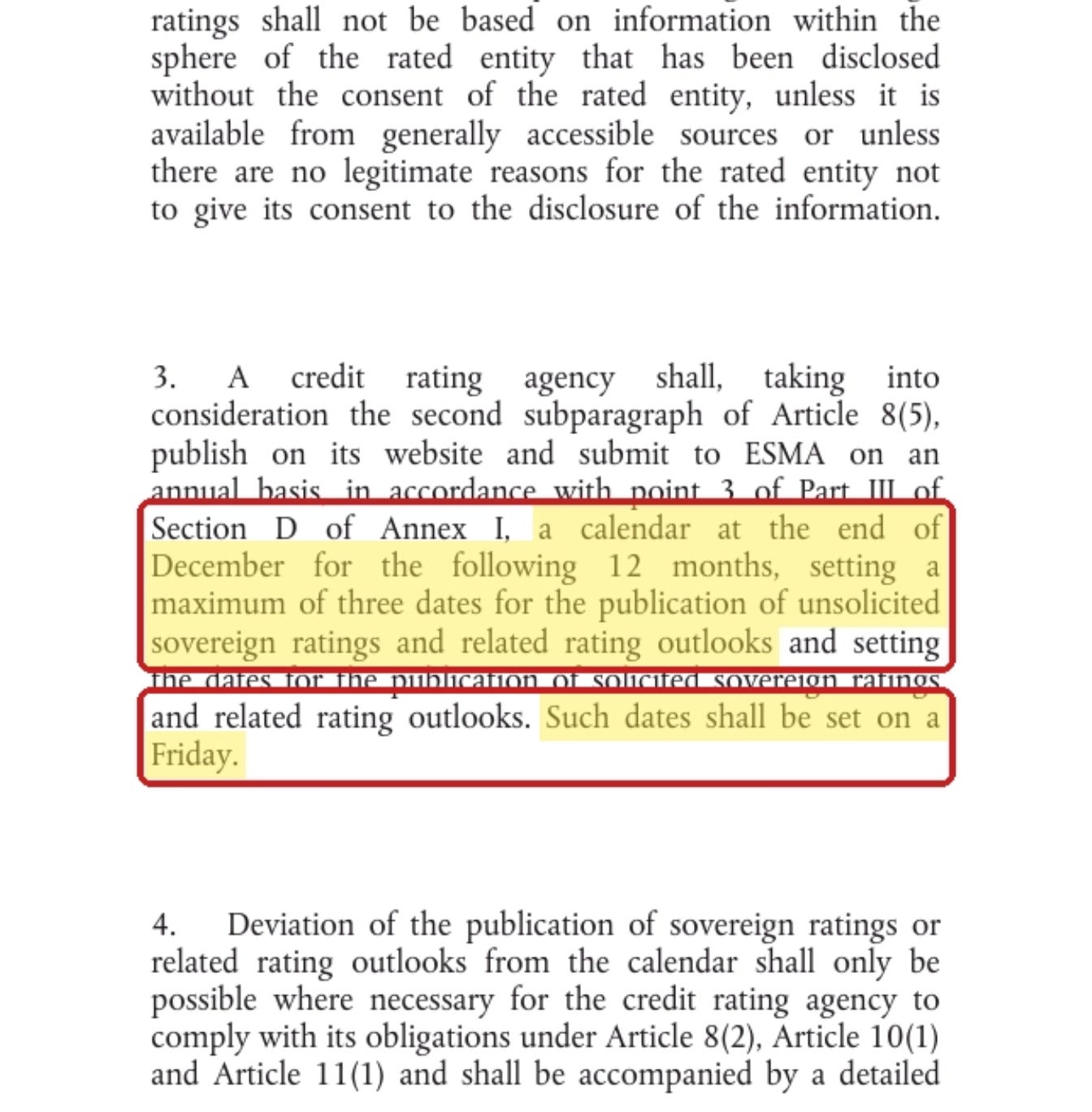

And here’s the part almost nobody knows: rating agencies are not allowed to surprise you with the timing — except in genuine emergencies.

An EU regulation (which binds S&P, Moody’s, and Fitch) requires them to publish, every December, a calendar of sovereign review dates for the following year — capped at three per country, scheduled on Fridays, announced after markets close. Deviating from that calendar is permitted only where the agency’s own monitoring obligations force it to act, and every deviation must be accompanied by a detailed written justification (Article 8a of the EU CRA Regulation; ESMA’s guidance adds that deviations “should not happen” as a matter of course). And that scheduled review has now happened: on July 13, 2026, S&P affirmed Indonesia at BBB/A-2 and kept the outlook Stable, citing solid growth prospects, prudent macro policy, and relatively low government debt — and describing the current fiscal strains as temporary. Exactly the kind of boring, scheduled, no-surprise outcome this section describes.

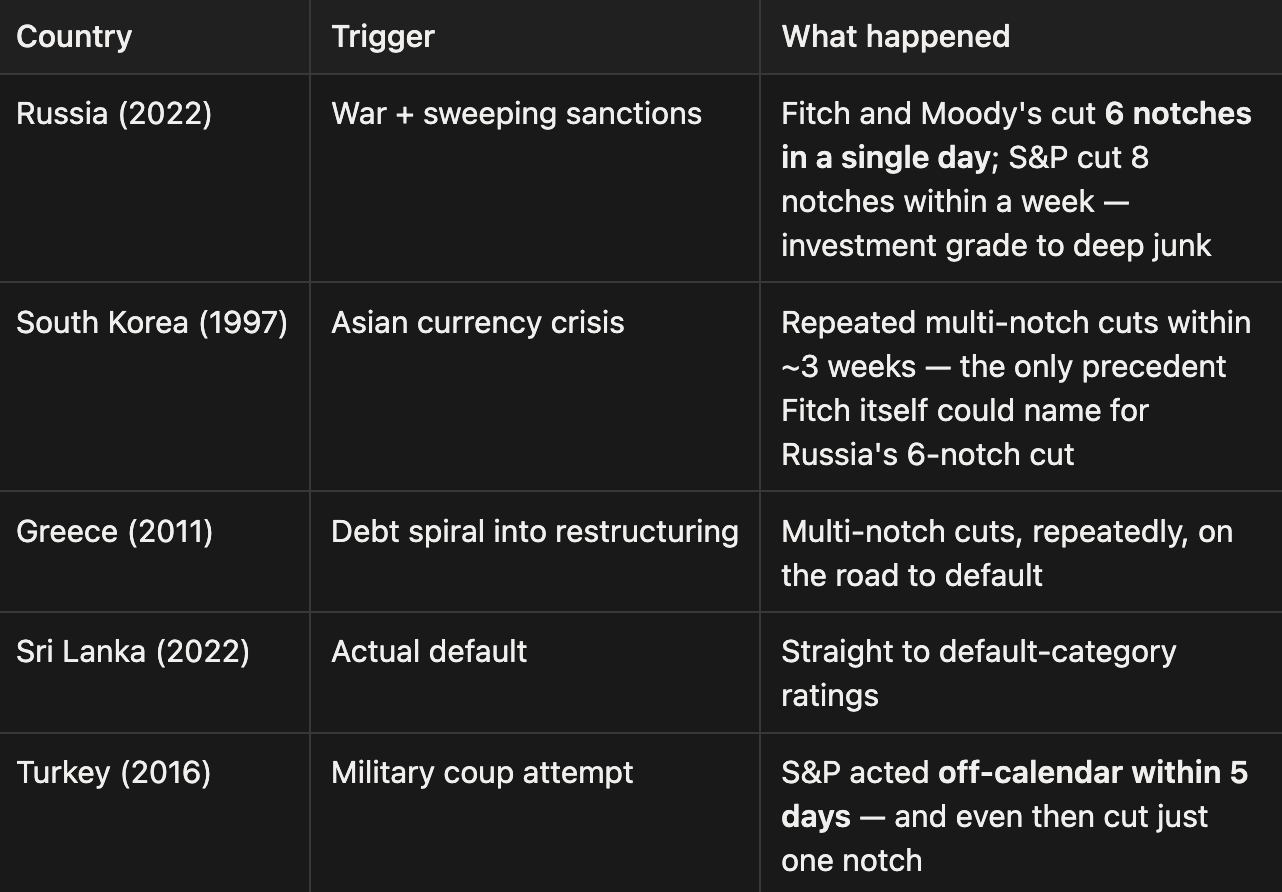

To be fair: agencies can break the calendar — and can cut several notches at once

We’d be cherry-picking if we didn’t show you the exceptions, because they’re real. Here is every notable case of a sovereign getting the “emergency treatment”:

Look at the triggers: war, sanctions, currency collapse, default, coup. That is the admission price for skipping the queue. Now hold Indonesia against that list: no war, no sanctions, no default — the economy is growing ~5%, government debt is ~41% of GDP, the primary balance just posted a first-half surplus, BBB was affirmed by all three agencies, and the market’s own insurance price on Indonesian debt (~91 bps, more on this below) is nowhere near crisis levels. The gap between Indonesia and that table isn’t a few steps. It’s a different universe.

So yes — the emergency exit exists. But every country that ever used it was already on fire. Indonesia isn’t.

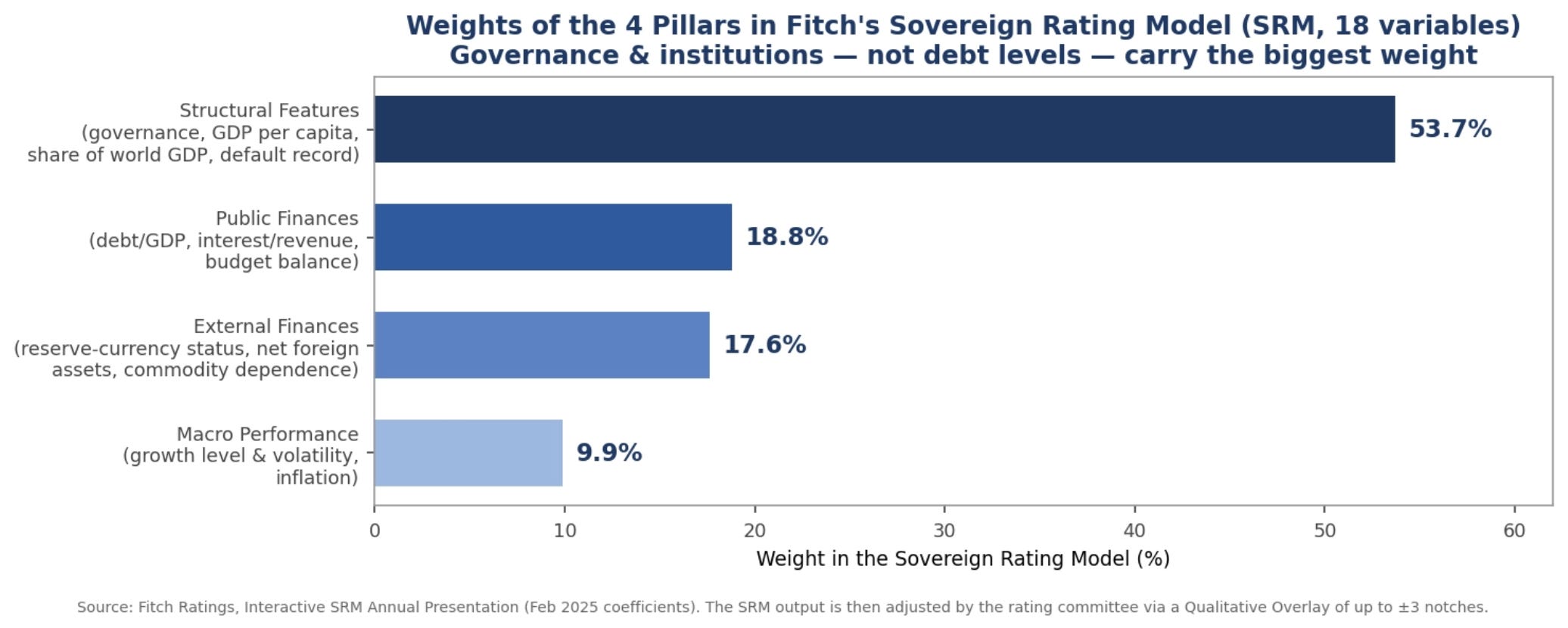

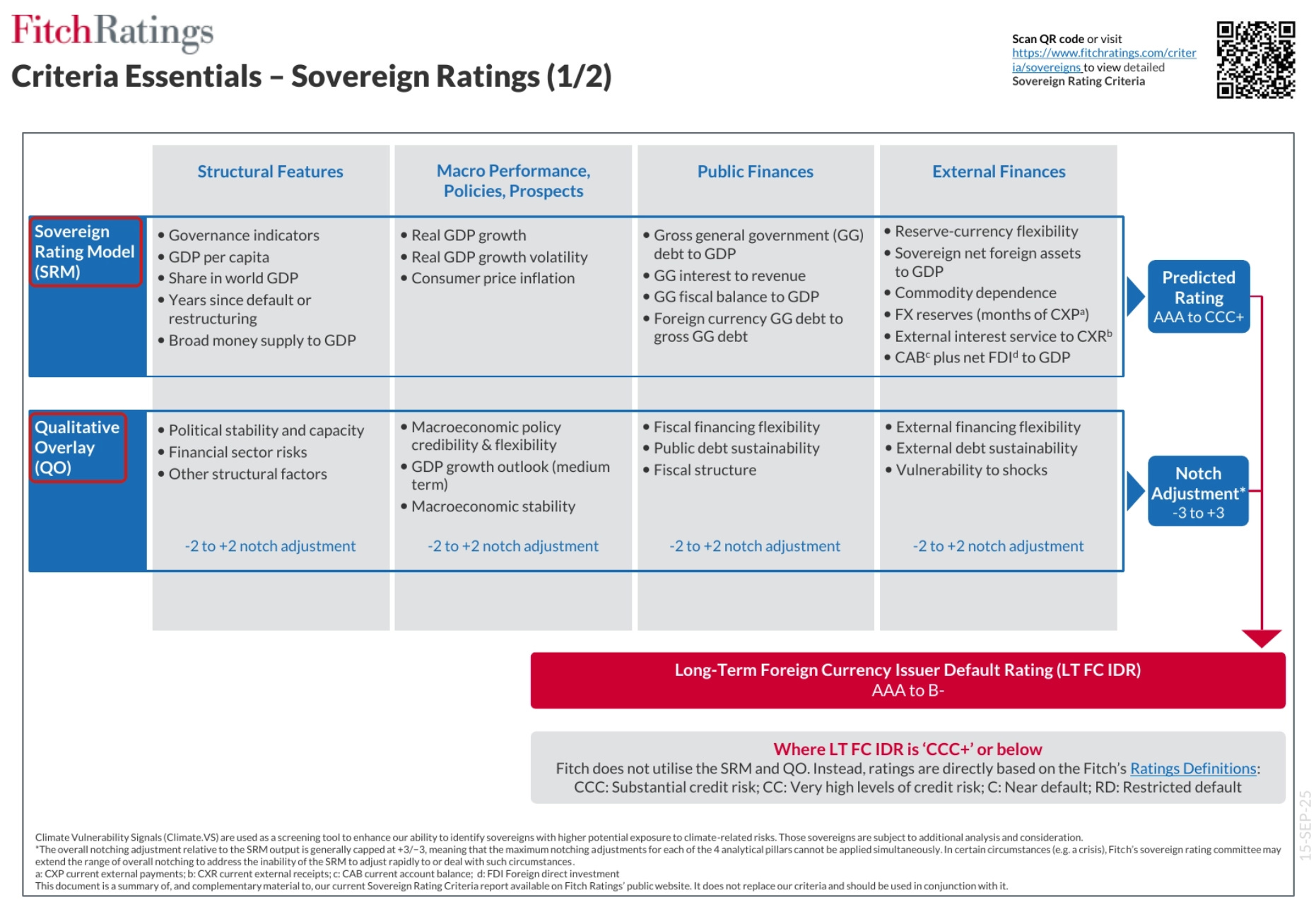

One more thing from the rulebooks that reframes the whole debate. When you look at what the agencies actually grade, the heaviest weight isn’t the size of government debt.

In Fitch’s model, governance and institutional quality carry more than half the total weight — more than public finances, external finances, and economic growth combined. Indonesia’s debt-to-GDP is around 41%, comfortably below the typical BBB country’s 58%.

Our problem was never the amount of debt. It’s that revenue is thin (roughly 13% of GDP versus 25% for BBB peers), the interest bill eats a growing slice of it, and this year’s policy noise — the fiscal program overruns, the pressure on Bank Indonesia, the Danantara questions — lands exactly on the governance box that the models weigh most heavily.

That’s what the outlook cuts were really about.

TL;DR — what the rulebook actually says:

A Negative outlook is a warning, not a verdict. By S&P’s own definition it means at least a 1-in-3 chance (33.3%) of a downgrade over roughly two years — so the single most likely outcome is that nothing happens.

The real alarm bell is CreditWatch (S&P) / the Watchlist (Moodys): The downgrade probability becomes at least a 50% chance within 90 days. Indonesia is not on it (yet).

Falling to junk requires two more cuts, at two different agencies. Indonesia is two steps above the line at all three.

No surprise ambushes in normal times. Review dates are published a year in advance — at most three per year, scheduled on Fridays. Agencies can act off-calendar or cut several notches at once, but historically only under extreme shocks (war, sanctions, default, coup) — and any deviation must be published with a written justification. S&P’s July review has since landed: rating affirmed at BBB/A-2, outlook Stable (July 13, 2026).

The agencies grade governance hardest, not debt. Indonesia’s debt is low (41% of GDP vs 58% for BBB peers); the pressure comes from thin government revenue and this year’s policy noise — which also means the fix is within the government’s own control.

And here’s the encouraging part: the course-correction has already started. In June, President Prabowo ordered the budget of his own flagship program — the Free Nutritious Meals (MBG) — cut from Rp335 trillion to Rp268 trillion, a Rp67 trillion (≈$3.8 billion) trim, in the name of “budget efficiency.” Two weeks later, Reuters reported the National Nutrition Agency was weighing another Rp40–50 trillion cut, with fewer kitchens and a refocused list of beneficiaries.

Cutting your own flagship program’s budget is politically expensive — which is precisely why rating agencies read it as a genuine signal, not lip service.

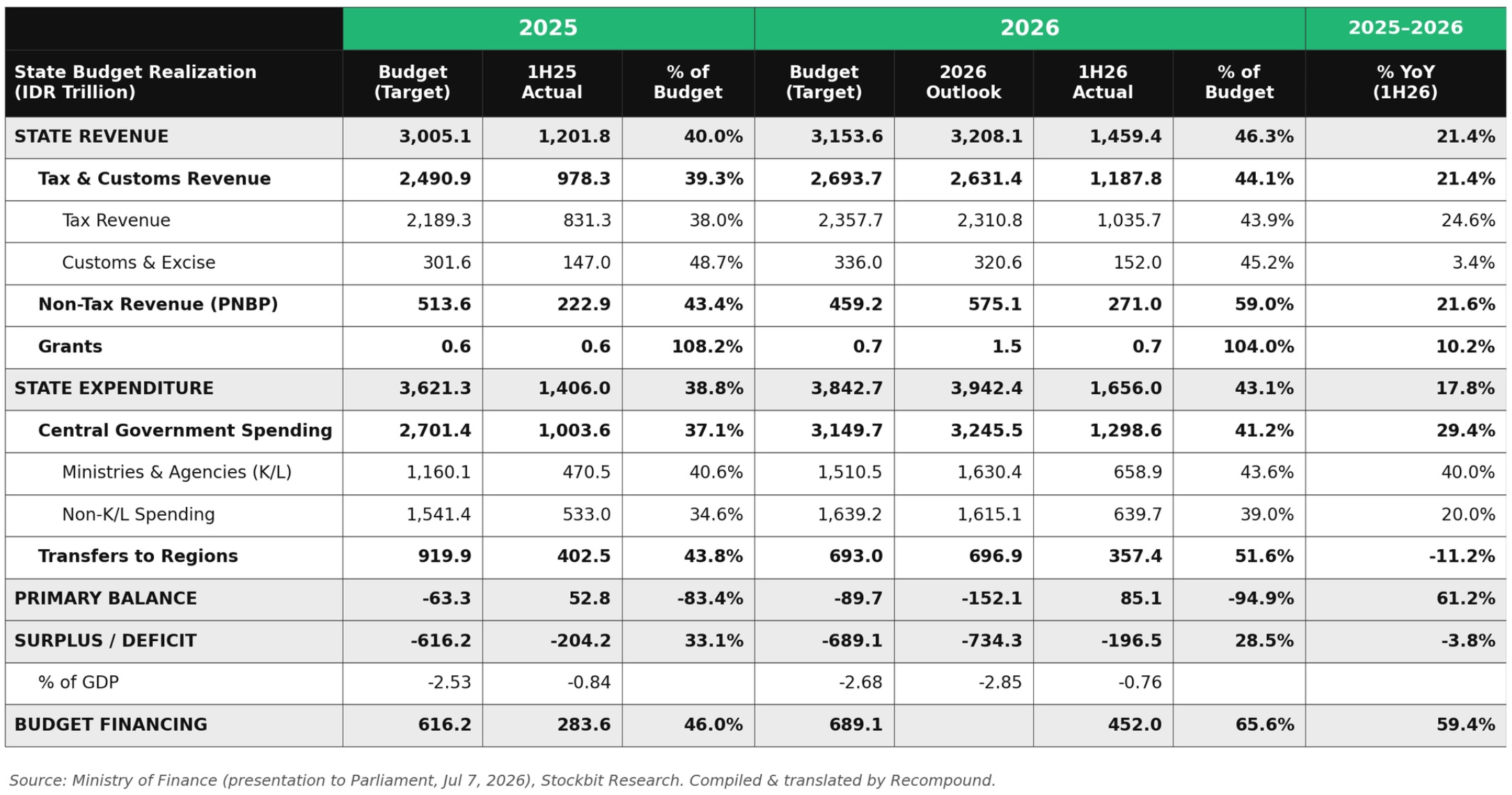

And the first-half numbers suggest it's more than talk: state revenue grew +21.4% year-on-year (tax collection +24.6%, helped by the new Coretax system), the primary balance posted a Rp85.1 trillion surplus, and the first-half deficit came in smaller than last year's (0.76% vs 0.84% of GDP) — with the Finance Minister saying the full-year deficit "can still be pushed lower."

Okay, but what if the worst actually happens?

Let’s play out the nightmare scenario properly, because this is where the social media misses.

To actually become “junk” in a way that matters, Indonesia doesn’t need one downgrade. It needs two downgrades each from at least two agencies — because the big global bond indices classify a country using the middle rating of the three. One agency getting cold feet changes almost nothing mechanically.

And about that scary phrase you’ve seen by social media fear mongerering — “forced selling.”

The fear is that index funds would be required to dump Indonesian bonds the moment we lose investment grade. We went and checked the actual index rulebooks. Three facts:

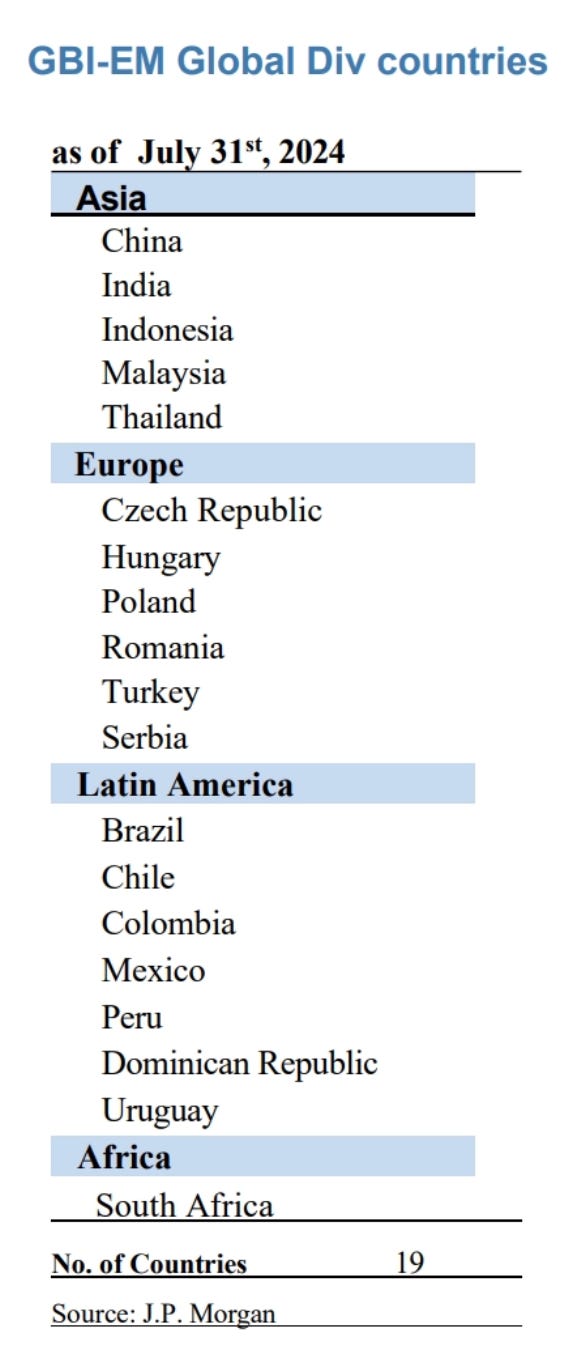

The largest pool of foreign money in Indonesian government bonds tracks an emerging-market index (JPMorgan’s GBI-EM) that has no rating requirement at all. Junk-rated Brazil and South Africa sit in it today. Nobody there is forced to sell anything.

The index with the strictest rating rules (FTSE’s world government bond index) — Indonesia isn’t in it. You can’t be kicked out of a club you never joined.

The one index that would matter (Bloomberg Global Aggregate) only ejects a country when two of the three agencies rate it junk — which is exactly why the two-step, two-agency math above matters.

Meanwhile, foreign investors hold only about 13% of Indonesian government bonds today, down from 39% at the peak in 2017-2019. The sellers, bluntly, have mostly already left. The buyers on the other side — local banks, insurers, pension funds, and Bank Indonesia — have absorbed everything foreigners have thrown at them for two years.

So where would a real downgrade actually hurt? Two places. First, state-owned companies: Pertamina’s and PLN’s ratings are chained to the government’s (agencies call this the “sovereign ceiling” — a company generally can’t be rated higher than its own government). Sovereign goes junk, they go junk, and their dollar borrowing costs jump. Second, the rupiah, through the one channel no rulebook can protect: confidence.

(And to be clear — the stock market has no rating rule at all. The separate scare you’ve read about, MSCI possibly demoting Indonesia from Emerging to Frontier market, is a different story with a different rulebook and a November deadline. Related mood, unrelated mechanism. Our friend Erik Hartanto has written a full analysis of that one: Will Indonesia get demoted to Frontier?)

What actually happened to countries that fell to junk

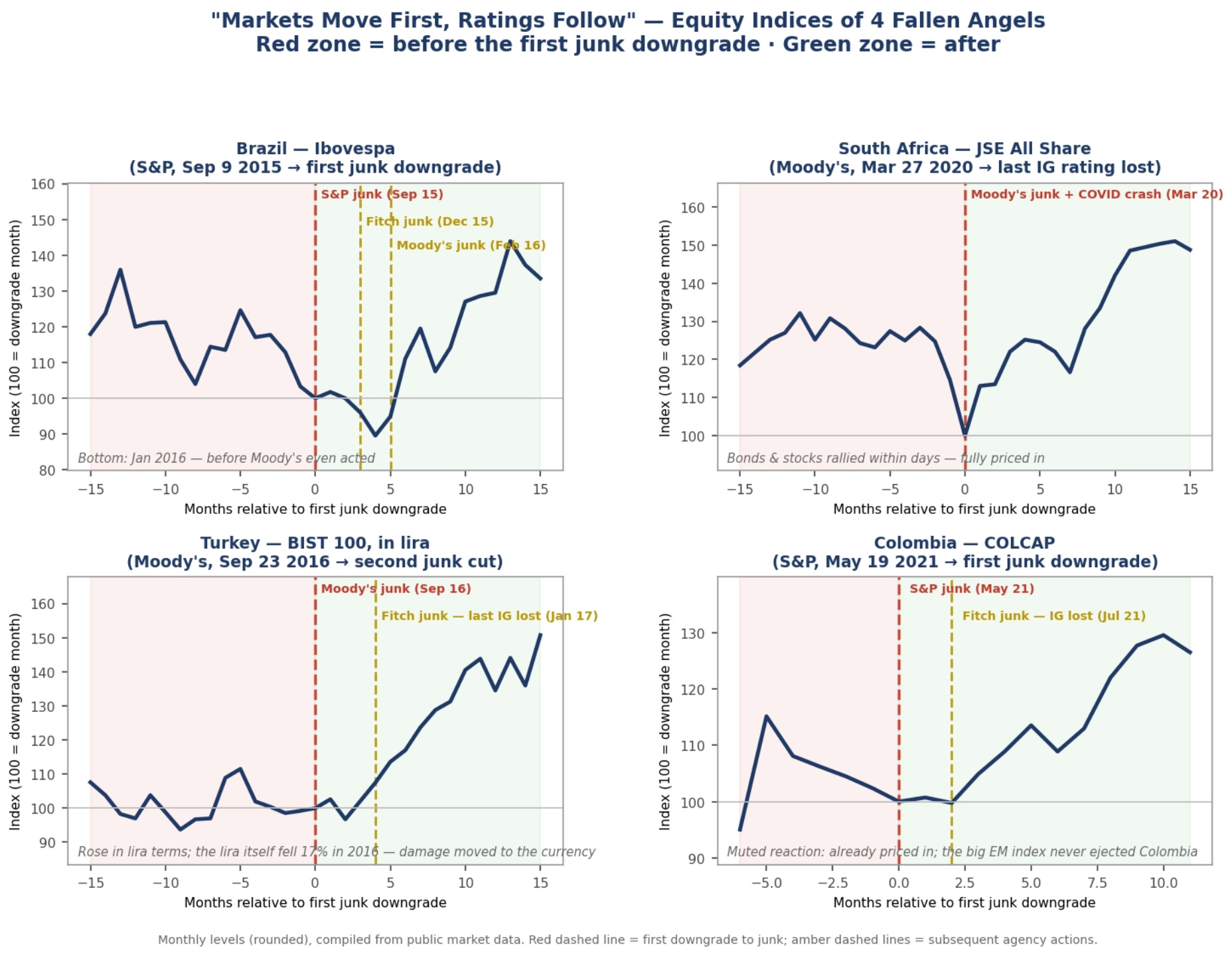

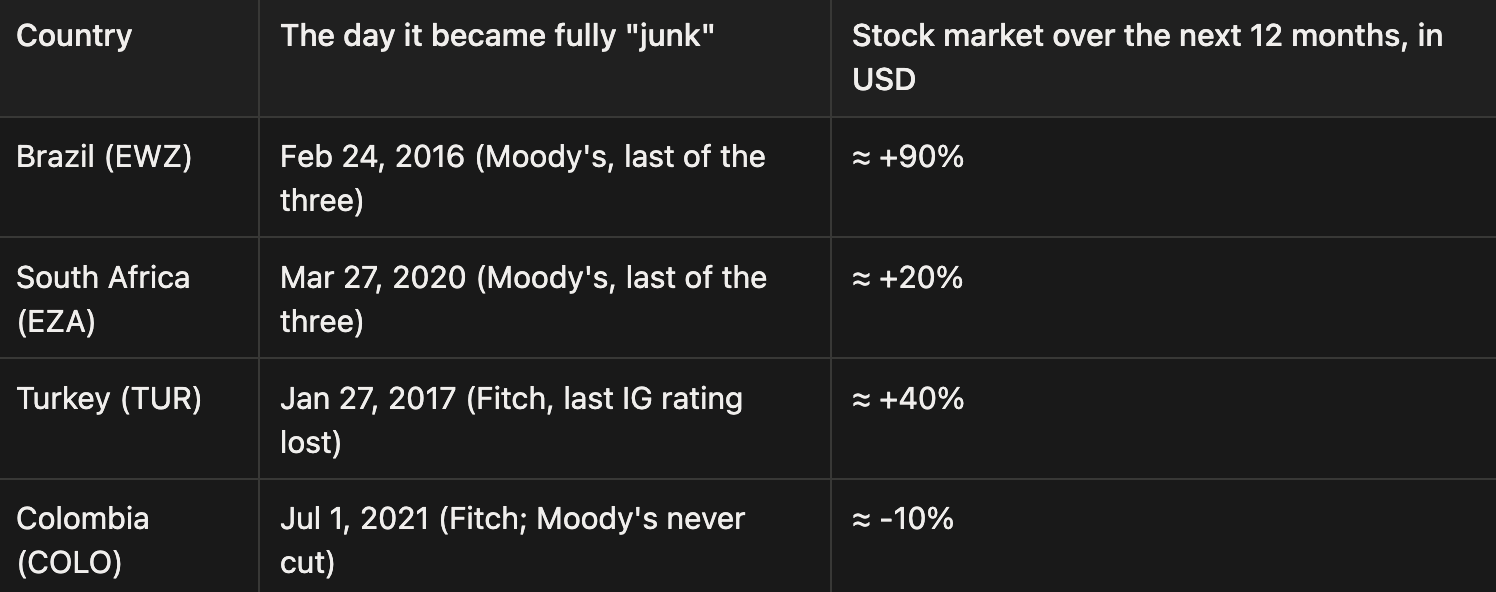

This is the part that changed how we think about the whole thing. Since 2015, four big emerging markets have lost their investment grade: Brazil (2015-16), Turkey (2016-17), South Africa (2017-2020), and Colombia (2021). We pulled the market data around each downgrade. The same pattern shows up every single time:

The crash happens before the downgrade. Not after.

Brazil lost investment grade in September 2015, after its currency had already fallen 33% and its stock market had been sliding for over a year. The market bottomed in January 2016 — before the last agency (Moody’s) even pulled the trigger — and then rallied nearly 40% that year.

South Africa dodged the final bullet for three years. When Moody’s finally cut it to junk in March 2020, bonds rallied within days. Everyone had seen it coming for years. It was fully priced.

Colombia is the closest cousin to Indonesia’s situation: solid economy, fiscal slippage after COVID, a failed tax reform. When S&P and Fitch cut it to junk in 2021, the market reaction was a shrug — its bonds had been trading at junk prices long before, and the big EM index never ejected it. Stocks were higher a year later.

Three lessons, and they’re remarkably consistent: markets sniff out downgrades months in advance (credit markets start pricing them roughly 90 days early, per academic studies); the official announcement often lands near the bottom, because by then the fear has nowhere left to go; and the real damage in every case came from the underlying fundamentals — recession, politics, commodity crashes — not from the rating action itself. The downgrade is the thermometer, not the fever.

And here’s the test that matters for an investor: what happened if you bought on the very day the last investment-grade rating was taken away — the moment of maximum bad news — and simply held for one year? Measured in US dollars, so currency collapses can’t hide anywhere:

Approximate figures, measured with US-listed country ETFs in USD: EWZ (Brazil), EZA (South Africa), TUR (Turkey), COLO (Colombia) — 12 months from the date the last investment-grade rating was lost, rounded. Honest caveats: Turkey’s gains were later wiped out by the 2018 lira crisis; Colombia’s negative year includes the mid-2022 election selloff.

Three of the four delivered positive dollar returns — one of them spectacular — to whoever bought at the moment of maximum pessimism — not because junk is good news, but because by downgrade day the bad news had been priced in for months.

And one more fact that makes the point even sharper. None of these four countries has ever regained its investment grade — Brazil is now a full decade into junk territory, South Africa and Turkey close behind, Colombia five years. The countries that did eventually claw their way back needed years of reform: South Korea took about two years after the Asian crisis, Russia three, Greece thirteen, and Indonesia itself fourteen (junked in 1997, restored in 2011). Sit with the asymmetry: the ratings stayed down for a decade or more, while the markets bottomed within months. Ratings move in decades. Prices move in months. That gap is the whole story.

Nobody posts this on Instagram: Indonesia is already priced like a crisis

If markets move before ratings do, a fair question is: how much fear is already in Indonesian prices right now?

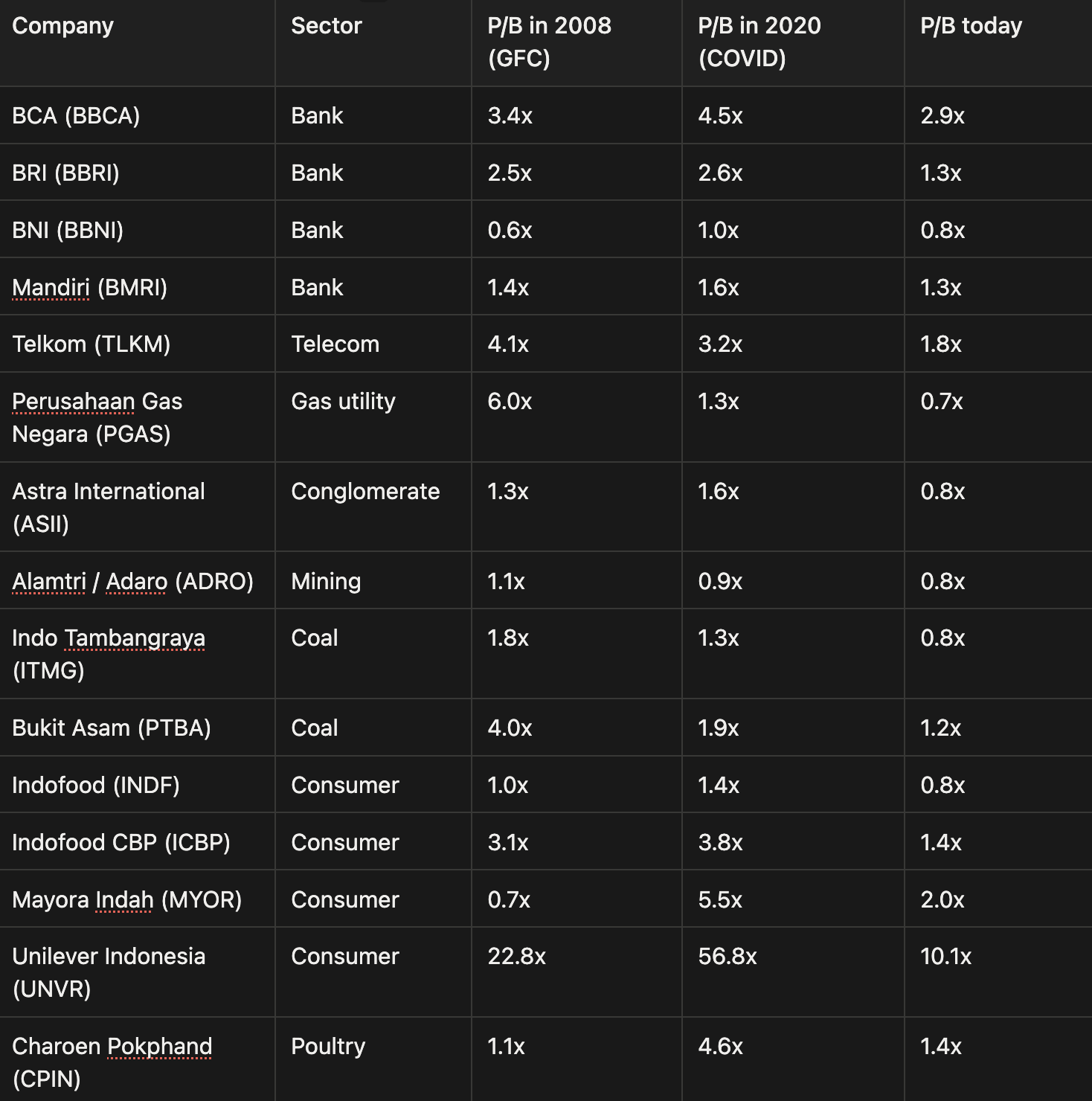

Here’s one way to measure it. Take Indonesia’s “too big to fail” companies — the biggest banks and the household names — and compare how the market values them today against the two worst crises of the past twenty years: the 2008 Global Financial Crisis and COVID in 2020.

A quick tool note: the cleanest yardstick here is price-to-book (P/B) — what you pay for each rupiah of a company’s net assets. (Price-to-earnings gets distorted in crises, because profits collapse and make the ratio look artificially high — so we deliberately use P/B throughout this table.)

Valuations for 2008 and 2020 taken around the trough of each crisis; “today” from Stockbit Key Stats as of July 11, 2026.

One honest caveat before you read too much into any single row: this table ignores company-specific fundamentals. Some of these discounts are deserved. UNVR is the clearest example — its ROE and profit growth have been declining for roughly a decade, so its de-rating from 56.8x is not pure fear; part of it is the market correctly repricing a weakening business. The same logic applies, in smaller doses, to several other names. Treat this table as a sensing tool for how much pessimism is embedded in the market as a whole — not as a list of fifteen bargains. Whether any individual stock is actually cheap still requires bottom-up work on the business itself.

Sit with this for a second. Every single one of the fifteen large-caps above is cheaper today than it was during COVID. Twelve of the fifteen are cheaper than during the global financial crisis of 2008 — a moment when the world’s banking system was genuinely collapsing.

No downgrade has happened. Indonesia is still rated investment grade by all three agencies, still growing at 5%, still running a nearly balanced current account. Yet the market has already marked its blue chips down to prices last seen when the global financial system was on fire. Whatever a downgrade is supposed to do to prices — a lot of it appears to be in there already.

What the market’s own insurance price says

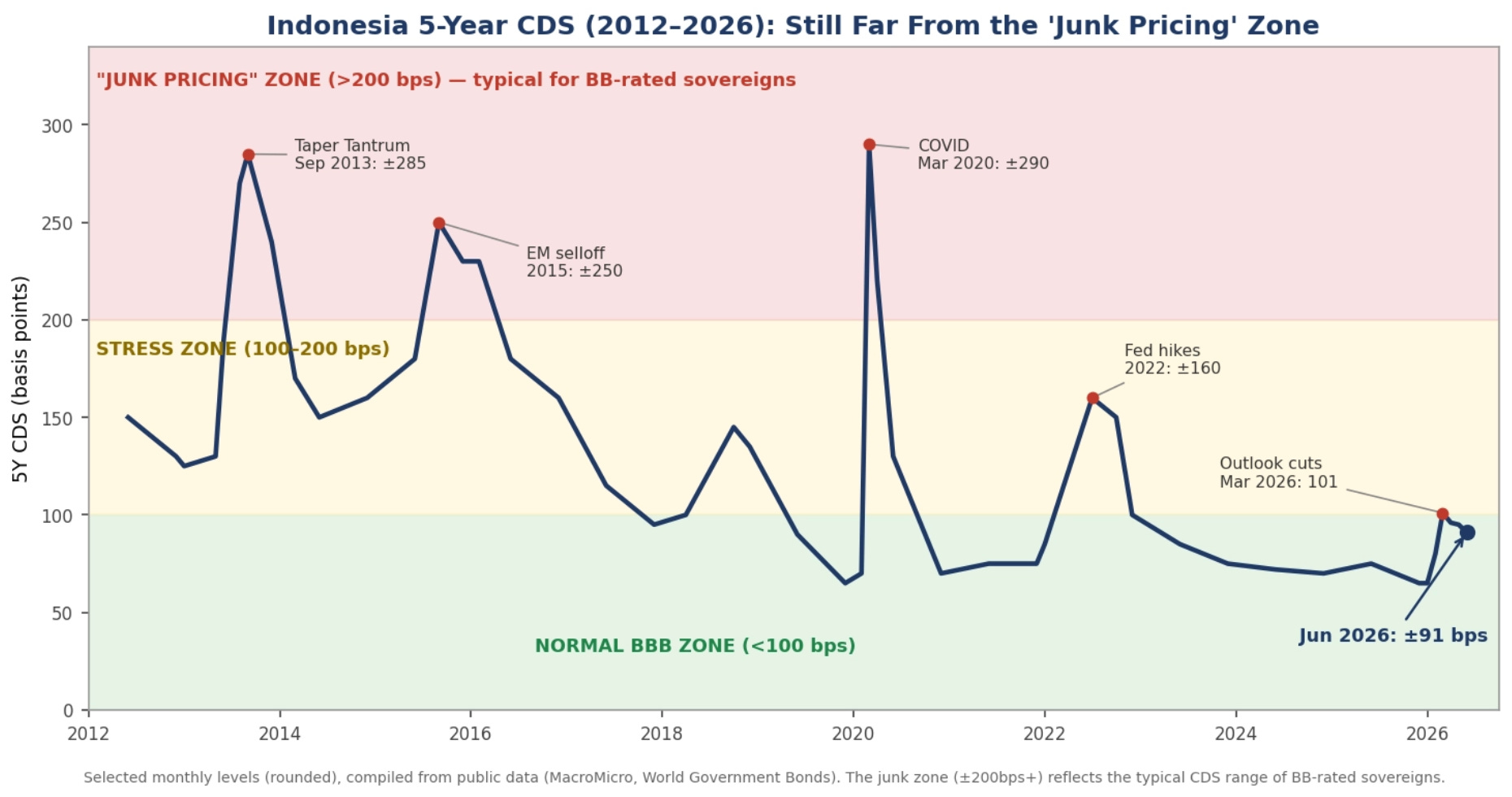

One more sanity check, and it’s our favorite because it can’t be spun: the price of insurance on Indonesian government debt.

There’s an instrument called a CDS (credit default swap) — think of it as an insurance premium that big investors pay to protect themselves if a government fails to pay its debt. The riskier the market thinks a country is, the higher the premium. It’s the closest thing to an honest, real-money opinion poll on default risk.

Countries that are rated junk — Brazil, South Africa, Turkey in their post-downgrade years — typically pay premiums of 200 basis points or more. Indonesia’s premium today: about 91. Even at the peak of this year’s panic in March, it touched just 101 — roughly half the level Indonesia itself hit during the 2013 taper tantrum (~285) and COVID (~290), both times when the premium spiked briefly and came right back down.

In plain language: the people with the most money on the line are pricing Indonesia as a normal BBB country having a rough year — not as a junk candidate.

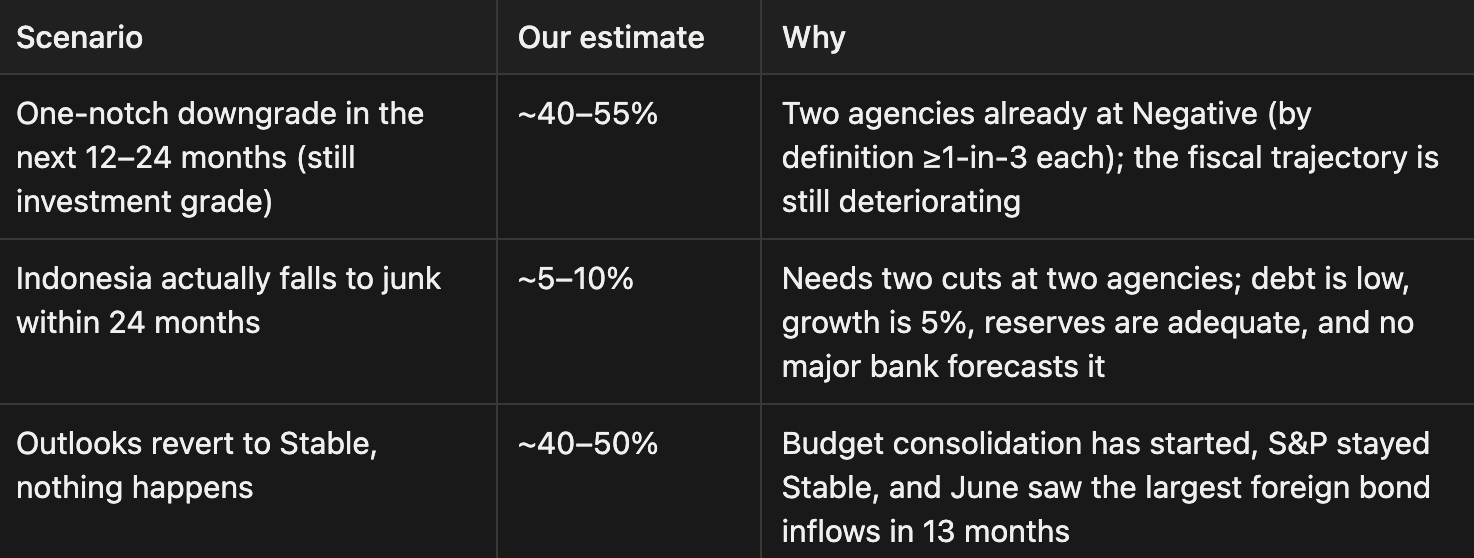

Probable Outcomes

Time to put numbers on it, with the honesty that these are estimates, not prophecy:

The single most likely bad outcome — a one-notch downgrade — would leave Indonesia exactly where Colombia, Brazil, and South Africa were years before their junk moments: still investment grade, with time and levers to fix things. And if the Colombia playbook holds, much of that scenario is already sitting in today’s prices.

Dates and numbers worth noting

S&P’s scheduled review — resolved. On July 13, 2026, S&P affirmed BBB/A-2 with a Stable outlook and called the fiscal strains temporary. The bear case needed S&P to join the other two at Negative — it didn’t. Attention now shifts to the next scheduled Moody’s and Fitch dates.

The 2026 budget deficit vs. the 3%-of-GDP legal cap. The government’s own revised outlook says 2.85%. The IMF projects 3.05%. This is the single most explicit trigger the agencies have named.

How much of the bond market Bank Indonesia ends up owning. It already holds roughly a quarter of tradable government bonds. Escalation here is the reddest of red flags in the agencies’ models.

MSCI’s November decision on Emerging vs. Frontier — different rulebook, same confidence channel.

The CDS premium. If it climbs past 150–200 and stays there, the market has changed its mind about everything we wrote above. That’s the honest kill-switch on this thesis.

The bottom line

The narrative racing around social media — “Indonesia is about to become junk” — skips about four steps of a process that is written down, regulated, and scheduled a year in advance — and which, outside of war-, default-, or coup-level shocks, has historically been slower and less dramatic than the panic that precedes it.

Could Indonesia eventually lose its investment grade? Yes — roughly a 5 - 10% chance over the next two years, by our estimate, and the watchlist above tells you exactly what would change our mind. But history’s most consistent lesson about these episodes is uncomfortable for panic-sellers: by the time the downgrade becomes official, the fear has usually peaked, the prices have usually bottomed, and the people who sold into the panic have usually handed their shares to the people who read the rulebook.

Truth be told, fear is already at crisis levels.

The rulebook, the history, and the market’s own insurance prices are not.

Sources & references

Rulebooks & regulation (primary sources)

Regulation (EU) No 462/2013 (CRA III), Article 8a — sovereign rating calendars, publication timing, and deviation requirements: EUR-Lex · ESMA interactive rulebook, Art. 8a

ESMA, Questions and Answers on the CRA Regulation (ESMA33-5-87) — guidance on calendar deviations: PDF

S&P Global Ratings, Ratings Definitions — official definitions of Outlook (≥1-in-3 over ~2 years) and CreditWatch (≥1-in-2 within ~90 days): spglobal.com/ratings

Moody’s, Rating Symbols and Definitions — Outlook and Watchlist definitions: ratings.moodys.com

Fitch Ratings, Sovereign Rating Criteria — Sovereign Rating Model pillar weights (governance ~53.7%): fitchratings.com/criteria/sovereigns

Index rulebooks: J.P. Morgan GBI-EM (no rating requirement), FTSE World Government Bond Index (rating floor; Indonesia not a member), Bloomberg Global Aggregate (middle rating of the three; ejection requires two agencies at junk) — per each provider’s published index methodology.

Rating actions & history

S&P Global Ratings — Indonesia Ratings Affirmed At ‘BBB/A-2’; Outlook Stable (July 13, 2026): press release · coverage: The Jakarta Post · IDNFinancials — JCI +1.92% on the news

Turkey 2016 off-calendar action: Bloomberg — S&P cuts Turkey credit rating, Jul 20, 2016

Russia 2022 multi-notch cuts: Bloomberg — Russia cut six levels to junk by Fitch, Mar 2022 · The National — S&P cuts Russia to CCC−, Mar 2022

Brazil (2015–16), South Africa (2017–2020), Turkey (2016–17), Colombia (2021) downgrade timelines: agency press releases and contemporary Bloomberg/Reuters coverage.

Indonesia fiscal & policy

MBG budget cut Rp335T → Rp268T: Jakarta Globe

Potential further Rp40–50T cut: Reuters via TradingView

H1 2026 APBN realization (revenue +21.4% YoY, primary surplus Rp85.1T, deficit 0.76% of GDP): Stockbit Snips

Market data

P/B valuations (”today”, as of Jul 11, 2026): Stockbit Key Stats; 2008/2020 troughs from historical financial statements and price data.

Post-downgrade 12-month USD returns measured with US-listed country ETFs: EWZ (Brazil), EZA (South Africa), TUR (Turkey), COLO (Colombia; the same fund formerly traded as GXG — full price history under COLO).

Indonesia 5Y USD CDS levels (≈91 bps today; ~101 at the March 2026 peak; ~285/~290 during the 2013 taper tantrum and COVID-2020): market data.

MSCI Emerging vs Frontier review context: Erik Hartanto — Will Indonesia get demoted to Frontier?

All data as of July 11–12, 2026 unless stated otherwise.

The forced-selling section is the one that should travel furthest. The GBI-EM point especially: no rating floor, junk-rated Brazil and South Africa sitting in it today, which deflates the scariest part of the panic. Where I'd connect it to the macro is that the rulebook floor looks solid, but the channel that seems to be doing the real damage isn't the rating, it's the rupiah past 18,000 and the confidence loop no methodology protects. So the ratings can be safer than the mood while the currency keeps paying for it. Do you see BI's bond ownership as the thing that eventually forces the agencies' hand?