Is Recompound expensive and making me bear all the risk?

We contend that Recompound is cheaper than mutual fund and is a form of insurance for you.

We still get asked a lot:

If I profit, I pay a certain portion of this profit as fee to Recompound

If I lose, shouldn’t Recompound compensate me?

Well, we contend that Recompound is actually a form of insurance for you.

Allow us to explain why.

Mutual fund fee structure

We went to Ajaib’s page to get the breakdown of the fee you pay if you buy a mutual fund in Indonesia. There are 3 types of fee included in mutual funds:

Direct charges to clients

Charges to the mutual fund itself

Charges to the asset management company

1. Direct charges to clients

One-off fee

Subscription fee (paid when you first buy the mutual fund): 2.5% of AUM

Topup fee (paid if you topup): 1% of AUM

Custodian fee: 0.2-0.25% of AUM

Redemption fee (paid if you sell your holdings): 1-1.5% of AUM

Bank transfer fee: Rp 3.500 - 7.500 (we can ignore this)

Total: 4.7 - 5.25% of AUM

Recurring fee

Management fee: 2-3.5% of AUM, charged annually

This is a fee that is factored in to the value of the mutual fund. Let’s say the mutual fund makes a clean 8% return. Subtracting 2-3.5% of the management fee, you will be told that your mutual fund makes 4.5-6% return.

Also, this is a fee that is charged annually (not a one-off fee). So you are charged multiple times based on how many years you invest in the mutual fund. But then again, you don’t know this.

So for instance, if your mutual fund’s actual 3-year return is 15%, you will be shown that your return is only 7.5% (subtract 2.5% x 3 years = 7.5% of management fee). Then from the 7.5%, you have to minus off the 5% one-off fee. So your net return is 2.5%.

2. Indirect charges: charges to the mutual fund itself

Similar to management fee, these charges will be factored into the overall returns of the mutual fund itself. They comprise of:

Fees for investment manager services

Fees for custodian bank services

Securities transaction costs

Fees for accountant (auditor) and legal consultant (notary) services

Costs of preparing financial reports

Prospectus renewal & distribution fees

Expenditure costs for urgent needs for the benefit of mutual funds

Payment of taxes relating to the above costs.

3. More indirect charges: charges to the asset management company

These are charged to the asset management companies. They are fixed costs of constructing and promoting these funds. They comprise of:

Preparation costs for establishing mutual funds (formation of KIK and required documents including fees for the services of accountants, legal consultants and notaries)

Initial prospectus printing and distribution costs

Mutual fund portfolio management administration costs (telephone, fax, photocopying, transportation from the investment manager in carrying out his business)

Marketing and promotion costs (including printing, promotion and mutual fund advertising costs)

Printing and distribution costs for transaction forms (purchase forms, resale, transfer of investment units and proof of ownership of investment units)

Fees for legal consultant services, accountants and notaries as well as other costs to third parties (if any) if the mutual fund is dissolved

Liquidation costs

The asset management company cover these costs through the fees they charged to you. This is a reasonable kind of costs to have, since any business will incur expenses to operate.

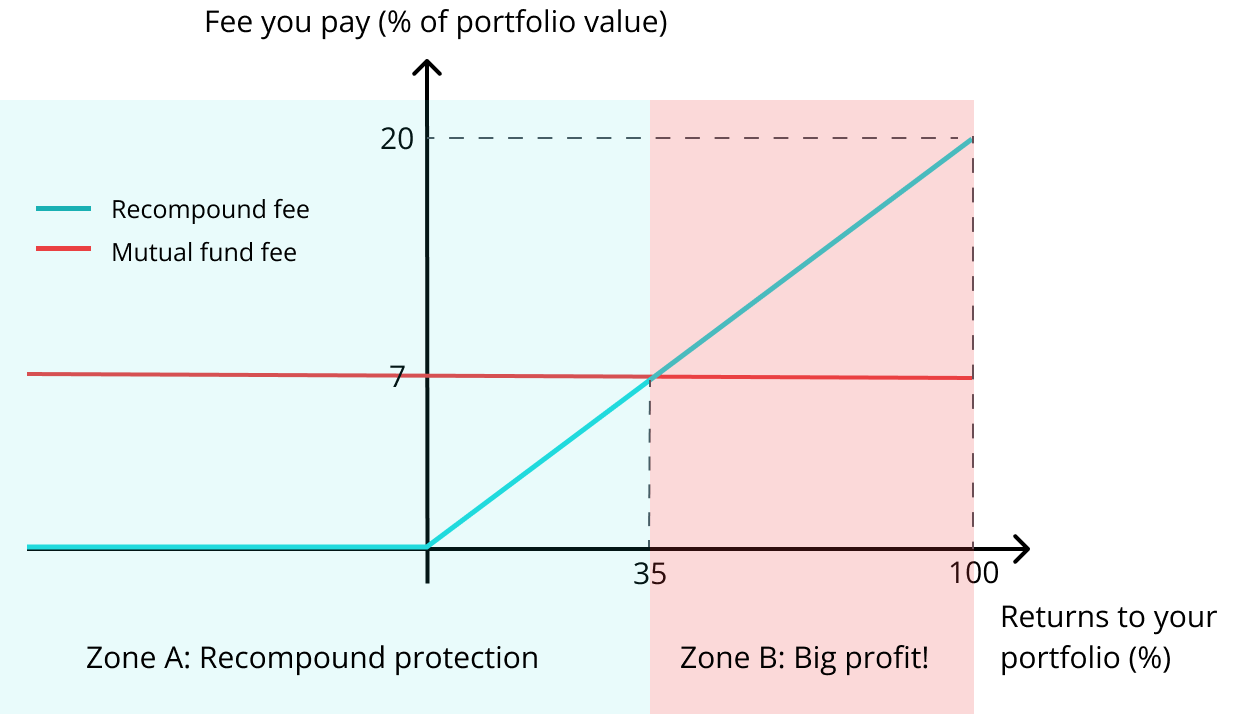

So how much fee do you pay for mutual fund vs Recompound?

This means that with mutual funds, the fee you pay is 4.7-5.25% of your portfolio value (paid once) plus 2-3.5% management fee (paid every year). Assuming you invest for a year, this means you pay 6.7-8.75% of your total AUM in fees.

With Recompound, you pay 20% of your profit. Let’s see how much fee you pay for these 2 options in a graph.

Recompound is more expensive than mutual fund at zone B

Indeed, buying mutual funds seems to be more profitable at zone B because you pay much less fee.

But the question is: will you be at zone B — will your mutual fund give you that big of a return?

Let’s look at the data.

This table from The Overpost shows that the average return of a 1-year mutual fund is 0.92%. Even if we look at the highest average return within the 1-year horizon, it’s 12.23%. We need to add the 2.5% management fee to this return to get a fair comparison. Therefore the average return is 3.42% and highest return is 12.73%.

Going back to our chart, we are still at the point where Recompound fee is lower than the mutual fund fee.

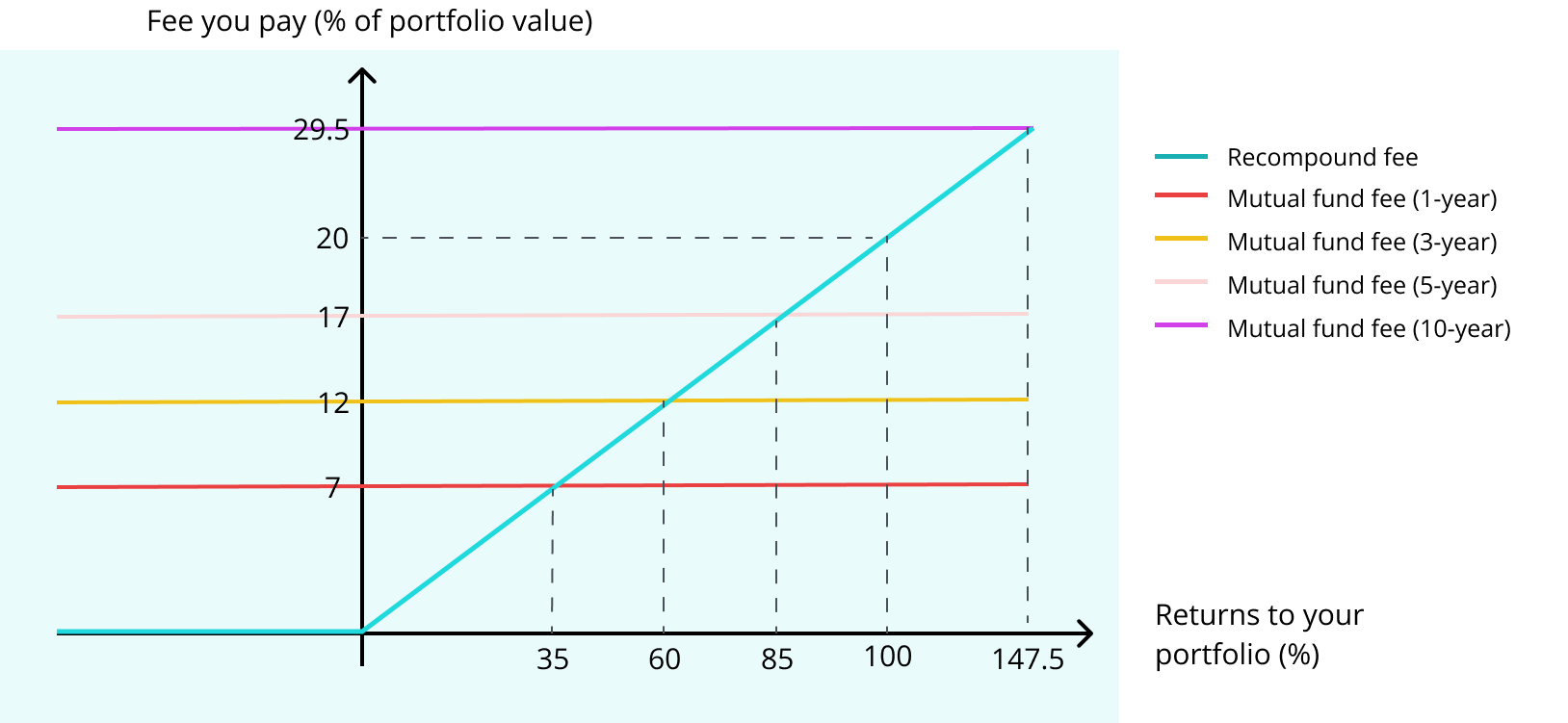

Figure 1 that we show earlier will need to be adjusted if we consider longer time horizon, because you would have paid the management fee for multiple years. Taking 2.5% management fee annually and 4.5% one-off fee, the total fee you pay for a 3-year, 5-year, and 10-year horizon mutual fund is 12%, 17% and 29.5% respectively.

From the graph above, it means that in order for Recompound to be more expensive than mutual fund, the mutual fund has to generate at least 35%, 60%, 85% and 147.5% returns for a 1-year, 3-year, 5-year, and 10-year time horizon.

Now we need to make some adjustments to the mutual fund return, based on the return shown in table .

The data itself shows that we will never be in zone B: the zone where the return given by mutual fund is high enough such that mutual fund is cheaper than Recompound.

Now the next question we have is: why is the return to mutual funds so low?

Here are a few reasons:

Mutual funds face significant restrictions in terms of the stocks composition. For instance, a mutual fund cannot hold more than 10% of stocks in a particular industry. This means that when the market is extremely bullish on (let’s say) the construction industry, they cannot take advantage of this opportunity and cannot buy more construction companies’ stocks.

No incentive to generate higher return. Imagine that you are a fund manager for that mutual fund. Your compensation scheme comprises of fixed salary and a bonus if you beat the index (IHSG). Let’s say the index’s return is at 5%. This means your salary will be the same if your fund’s return is 5.1%, 10%, 20%, or 50%. Now, would you put in your blood, sweat, and tears to get a 50% return? Of course not. You would be aiming to just get a return of 5.1% to earn that bonus, won’t you?

This means that the likelihood of you even entering zone B with mutual fund is very low.

Now that we have established that you will most likely be at zone A if you buy a mutual fund, it is clear that you will be incurring less fee with Recompound than with mutual funds.

Would Recompound optimise for sub-par returns?

Now let’s bring the attention back to Recompound.

Would Recompound do the same thing as mutual funds? That is, would we just want to give you subpar returns?

Recompound’s revenue is exactly equal to the Recompound fee you pay. So as a rational and profit-maximising firm, what we want is as much profit as possible. If possible, Recompound wants to reach a point where your return is infinity, so that our revenue is also infinity.

But let’s be realistic and go to the boundaries within the graph. As a company, Recompound is aiming for the maximum revenue, which means that we want 20% of your portfolio growth. If we set an upper bound at 100% return, this means that we want to make sure your portfolio earns 100% returns. Which means that we really, really want you to be in zone B.

What happens in bear market and we get into the negative part of zone A?

Well, it is all very clear that you don’t pay anything to Recompound. In contrast, you would still be paying 7% of your portfolio value to mutual funds.

Let’s say your portfolio suffers a 5% loss. What is your total loss then?

With a 1-year mutual fund: 5% portfolio loss + 7% fee = 12% loss

With a 3-year mutual fund: 5% portfolio loss + 12% fee = 17% loss

With a 5-year mutual fund: 5% portfolio loss + 17% fee = 22% loss

With a 10-year mutual fund: 5% portfolio loss + 29.5% fee = 34.5% loss

With Recompound: 5% portfolio loss + 0% fee = 5% loss

So Recompound is a form of protection against that mutual fund fee during bear markets.

Your expected return

Now that we have established these facts, let’s calculate your expected returns of investing through mutual fund vis-a-vis Recompound.

Because the world is uncertain, we can only calculate that expected returns based on probabilities.

This is how we construct the probability distribution for the 4 scenarios shown.

Mutual fund is optimising to just beat the index by a small margin (say 0.1%)

Recompound is optimising for inifinity return

Based on historical data shown in figure 2

We assume a normal-like distribution centered around mid-level return

The expected return is computed based on the following formula:

Where f(x) is the probability density function of the uniform distribution.

Now, why doesn’t Recompound insure your loss?

We have shown that at zone A, Recompound is cheaper than mutual fund.

At the negative part of zone A, Recompound is even insuring you against the management fee loss of mutual funds.

At zone B, Recompound is more expensive than mutual fund.

But the data shows that mutual fund is unlikely to land you in zone B.

With all these facts laid out, you can deliberate if Recompound is a good fit for you and we hope you see how Recompound can be a form of protection for you 🙂