As always, this is not an investment advice on the mentioned ticker. This is for educational purposes only. Always do you own research or consult your investment advisor before making your own investment decisions.

Let’s get into this.

Part of my 2026 new year’s resolution was to get better at running. What better way for me to get better at running by forcing myself to join big running events, so that I could get my coveted 10K or HM Personal Best. One competition for me that stood out was JAKIM 2026. It looked legit as I recalled in the previous years where the competition was organised, there were plenty of road closures in Jakarta area, around the running event.

So when I saw in a running calendar event that JAKIM 2026 was open for registration, I speedily rushed to my phone and attempted to register. The registration process was awful. The instructions was vague and the website load was slow. The worst part? I have to download yet another banking app to register. So I downloaded Bale from BBTN, opened an account and… failed to register because tickets were sold out. I thought to myself, “wow running has been super popular nowadays in Jakarta” but again I thought to myself “wow this Bale app by BBTN must have gotten a lot of users from this running event” so let’s take a look at BBTN.

The app itself must be properly built because it handled large amounts of traffic quite smoothly. As people are forced to make a bank account and settle ticket payments there, I wonder how’s their Current Account / Savings Account ratio (CASA ratio). Banks love low cost funds because they are in the lending business. You’d want the cost of your funds to be low (giving people less interest) so that you can have higher spread when you lend the money out to people, giving you higher net interest margins. So if you hold super established running events and make participants bank with you as a pre-requisite to purchasing those tickets, you’d get access to cheap funds.

Quick note: CASA Ratio measures the proportion of current and savings accounts in a bank’s total deposits. Current accounts are low-cost funds (little to no interest paid), while time deposits are more expensive for banks. The higher the CASA Ratio, the cheaper the bank’s funding base — and generally, the better.

In marketing words, Running is top of funnel (TOFU) and as people get acquainted with the bank’s app and its usability, they get pushed down the funnel as they use the app more extensively for other banking services (like getting a mortgage).

So I went to look at the CASA ratio numbers since 2022 (the first time they held a JAKIM marathon was in 2023).

Desember 2022: 48.5%

Desember 2023: 53.7%

Desember 2024: 54.1%

December 2025: 48.7%

I’d say the CASA ratio growth is not too shabby, although I have seen better numbers in other banks. But given BBTN’s price to earning’s ratio about ~5 and BBTN’s price to book value which is about ~0.5, it might be interesting for me to go deeper because the bank is showing signs that it wants to stay relevant, but the market is rating it as if it is filled with super bad assets in a sunset industry. So it makes me curious as to what is BBTN’s main business. Why market seems to be quite harsh on BBTN. I don’t think there will be a right or wrong answer to this, but it is fun to explore.

Investors are forward looking

We invest today not to get the returns immediately. There is usually an underlying thesis why the company we invest today will be more valuable tomorrow. We’d be more inclined to invest if the company is poised to grow. So what are the growth drivers for BBTN?

Well, BBTN is a specialised bank that is focused on mortgages. So it really is more of like a property business but with a much faster sales cycle (you don’t have to wait for developers to build and handover to their customer for you to acknowledge sales in your books), the moment a customer takes in a mortgage, the bank gets revenue (remember, you pay the bank an interest if you take mortgages!!). For BBTN’s case, the moment a real estate developer develops their houses, they also get revenue. So they get revenue from both property buyer and real estate developer. But it also has its downside where property developer would get their money as soon as there is a buyer, BBTN has to deal with the uncertainty of home buyers defaulting on their mortgages. Then they are left with illiquid real estate assets.

But what type of property is BBTN focusing on? Affordable housing.

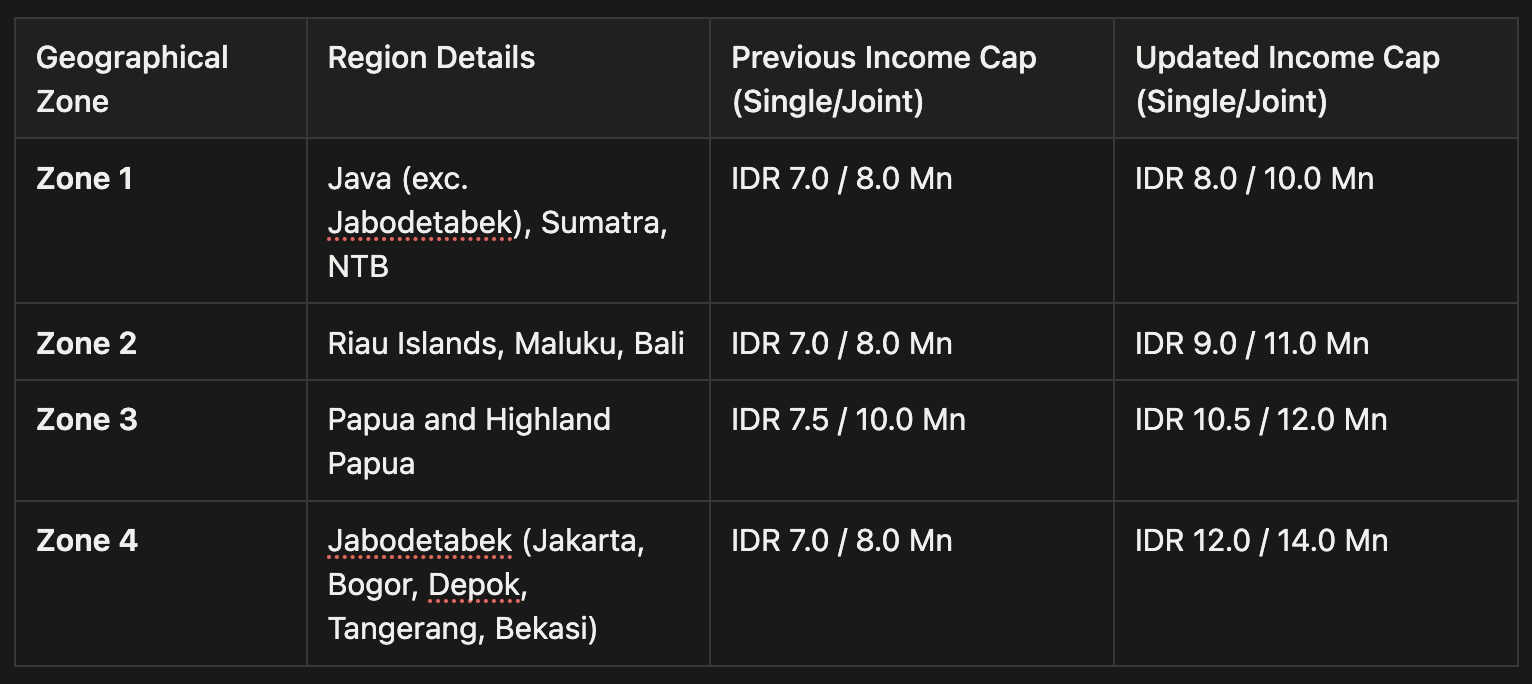

The core portfolio is split between subsidized (FLPP) and non-subsidized mortgages, with the former representing approximately 64% of the total loan book as of 9M25.

Who’s buying the houses? Well we have seen that millennials represent ~79% of the subsidized customer base. This demographic focus typically results in higher Loan-to-Value (LTV) stability and long-term customer retention. But because this is subsidized housing, it follows that not everyone (especially the bourgeoisies) can participate. Your monthly income cannot exceed a certain threshold, otherwise you will have to pay non-subsidised interest on your mortages. But if you do qualify, interest is super attractive and your likelihood to default is also minimised. More encouragingly, the income cap to qualify for FLPP has been raised.

FLPP Income Eligibility Criteria (Updated April 2025)

This tells us that the number of people who can qualify for this loans would also increase. Which translates to better quality loan books for the bank.

Cool, now that the bank potentially will have access to more quality borrowers qualifying for FLPP program, does the bank has enough liquidity to make the loan? Well yes, we can see that the deposit growth is outpacing loan growth. You might think is it because the Finance Minister Purbaya who placed Rp 25 Trillion into the bank? You are correct, but even if we exclude the massive government fund placement, the core deposit growth still stood at a very healthy 9.2% year on year (up to 10.0% in specific institutional/retail metrics).

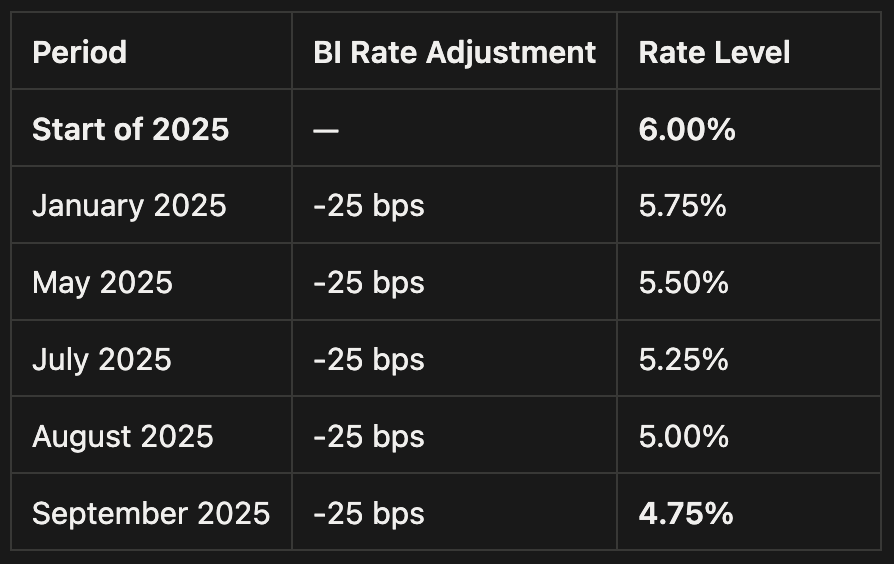

So it looks like it is going to be very good for shareholders isn’t it? On the cost side we are seeing that macroeconomic factors are giving that extra “ooomph” for the bank to grow. For example, Bank Indonesia lowered its policy rate to 4.75% in Q3 2025.

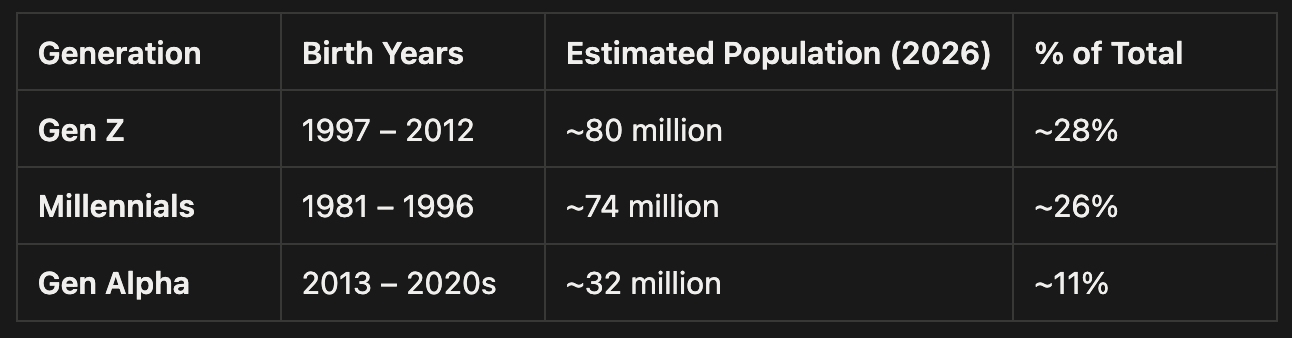

On the revenue side, we are also seeing the FLPP program growing from the government’s 3 million housing program for millennials who by the way makes up a growing chunk of the population (Indonesia is experiencing a bonus demography).

Since 2015 (back then it was still one million house), BBTN is the dominant contributor to these national figures, consistently contributing ~60% of the national housing realization annually through both demand-side financing (Subsidized Mortgages/KPR) and supply-side financing (Construction Loans for developers)

According to BBTN’s sustainability data, the national achievement of the program per year is as follows:

2015: 699,770 units

2016: 805,169 units

2017: 904,758 units

2018: 1,132,621 units

2019: 1,257,852 units

2020: 965,217 units

2021: 632,373 units

2022: 875,832 units

2023: 878,727 units

Rest assured, BBTN is highly specialised in supporting government programs like this and supporting FLPP would require expertise in cashflow management. Which means it is likely that it will be more and more favoured vehicle to realise the government’s program into the future (2026 and so on). Now we could see that the narrative is there and the case for increase of profitability from higher net interest margin is also there.

But what’s with the market valuing the company as if the company is in a sunset industry? Are investors in IDX crypto bros who believe that blockchain and DeFi will make banks a dinosaur? Jokes aside, let’s try to find out more about potential setbacks that BBTN is facing.

So what are the setbacks

Well COVID. If you noticed during COVID years the number of units that got constructed above took a dip. But more important than that, it is reasonable to believe that COVID would affect the quality of mortgages because many people lost their jobs during that time of lock downs and ceasing of business operations.

During COVID, Bank Indonesia allowed banks to "restructure" loans. This meant a loan could be "non-paying" but still classified as "performing" on the balance sheet. This allows a company to keep booking "accrued interest" as profit even if the customer hasn't paid a single Rupiah in cash.

We see this clearly when we compared accounting profits and actual cash generation. Accounting profits was relatively stable at Rp 1.6 Trillion (ignoring the anomaly in 2019). But Cash receipts dropped from Rp 3.4 Trillion in 2019 to 1.8 Trillion in 2020. So this is already telling me that the bank was hit by a double-whammy: a collapse in new loans (seen in the construction dip) and a deterioration of the existing loan book because of COVID.

If I were in the CEO’s seat, my first priority would be to clean up the balance sheet. Bad assets should be dealt with decisively so they don’t become a structural drag on profitability for years. When Pahala N. Mansury handed over to Nixon L. P. Napitupulu, who assumed the role of Acting CEO in February 2021, the signals suggest that this is precisely what management began to focus on.

One area that reflects this effort is the Loan at Risk (LAR) coverage ratio.

A loan categorized as “at risk” (LAR) has elevated probability of becoming a Non-Performing Loan (NPL), so prudent management would increase provisions to cushion against that possibility.

Historically, throughout the 2010s, LAR coverage hovered around ~15%. Since Mr. Nixon’s appointment, it has been raised to the 19–21% range. Directionally, this is the right move — it signals greater conservatism.

However, as outside investors, we do not know whether this level of coverage is sufficient. Asset quality risk is dynamic, not static. If underlying borrower stress resurfaces, or if post-restructuring performance deteriorates, LAR coverage may need to be increased again. That would come with consequences: higher provisioning, lower near-term earnings, and potentially weaker returns on equity.

In other words, while management appears to be acting prudently, there remains uncertainty around whether current reserves are adequate for the true embedded risk in the loan book. Until that uncertainty clears, the market is unlikely to assign a premium valuation — and as investors, we must acknowledge that limitation.

For now, there seems to be quite a number of puzzle pieces that remain unresolved:

Is the management going to be able to continue executing the program 3 juta rumah well? Is the management going to steer clear from the non-subsidized mortgages (which is known to be taking a hit nowadays due to recent layoffs)?

Has the COVID asset quality deterioration been handled well?

Is the management going to be able to be less reliant on time deposits as source of funds? It is heading towards that direction with the running events, Bale, and corporate initiatives but we need to see a stronger signal while there are other banks are already showing more sexy CASA numbers.

If you are an investor, how would you value this kind of company? Do you think it has enough margin of safety? Multiples wise its cheap but it feels less firm because a number of things could go wrong although the tailwind is right in front of our eyes. Especially given the fact that we are seeing signs that management has been doing the right thing. Do they deserve to be appreciated better? Or no? But regardless, we haven’t made ourselves comfortable in building a position.