Disclaimer: this is not an equity research report and it is not a buy, sell or hold recommendation on any mentioned stock. This article is co-authored with Gupita Candra, one of our investment analysts. Views mentioned in this article is the authors’ views solely for the purpose of education and should not be construed as financial advice. Views presented also do not necessarily reflect the view of Recompound as a company.

If you want to learn more about Recompound head over here. If you want to commit 30 days to learn 30 lessons about investing, you can click here.

Business Model

PT Adira Dinamika Multi Finance Tbk (ADMF) is a financing company. The model of a financing company is simple.

Imagine a fictional character Alex wants to buy a new car. Since everybody is talking about BYD, let’s talk about the all new Toyota Prius that has a solar panel at the top.

After watching the car review by MKBHD, Alex is in love with this car and he wants it badly. So he goes to his favourite car dealer, Bob, with the intention of buying it.

Alex: “Hi, I’d like to buy the all new Toyota Prius”

Bob the Dealer: “Cool, it sells for Rp 300 mio”

Alex (thinking): “Aw darn, I only have Rp 100 mio in my bank account right now”

Bob the Dealer: “I can read your mind, don’t worry we have Adira as one of your financing options”

So Alex opens the adiraku app and submits his application, he will have his Toyota Agya as his collateral (worth Rp 60 mio) and when the application is approved, Adira will purchase the car upfront for Alex. Then Alex will only need to pay in instalments to Adira based on Alex’s finances (lets say in 24 months).

How does Adira makes money then? Well, Alex needs to pay Adira Rp 300 mio + interest. The interest in this case is 20%. So in total, Alex needs to pay Rp 360 mio, divided by 24 months which is Rp 15 mio per month.

In 2022, Adira charges about 13-17% of interest for new 4 wheel (4W for short) and their revenue comes from the interest paid by Alex the debtor. So to recap, if we construct a diagram to represent the relation, we see that Adira makes money from Alex through interest in exchange for financing.

As a matter of fact, Adira is very experienced in doing financing. Leasing process can be done in less than one day thanks to Sistem Layanan Informasi Keuangan (SLIK) by OJK. They also finance a wide variety of products that Alex might want to buy such as:

New Cars (4W)

Used Cars (4W)

New Motorcycle (2W)

Used Motorcycle (2W)

Furniture

Umroh

Gadget

Wedding

Bulk of their financing business, however, is in automotive products so we’ll primarily focus on that. The table below is a 2022 snapshot of interest and their average selling price (ASP) per category.

So how does the company calculate and account for the money they make exactly? The revenue of the company can be computed as follows:

Lets make sense of the equation by providing a concrete example. Btw, the scary looking greek symbol sigma just means summation (”=sum()” in excel).

On a given year, Adira provides new financing (e.g. to Alex) and payments will be made by the debtors. Let’s say in total Adira provides Rp 100T worth of financing and 10% of it has been paid because instalments start immediately (Alex immediately starts paying for his new Toyota).

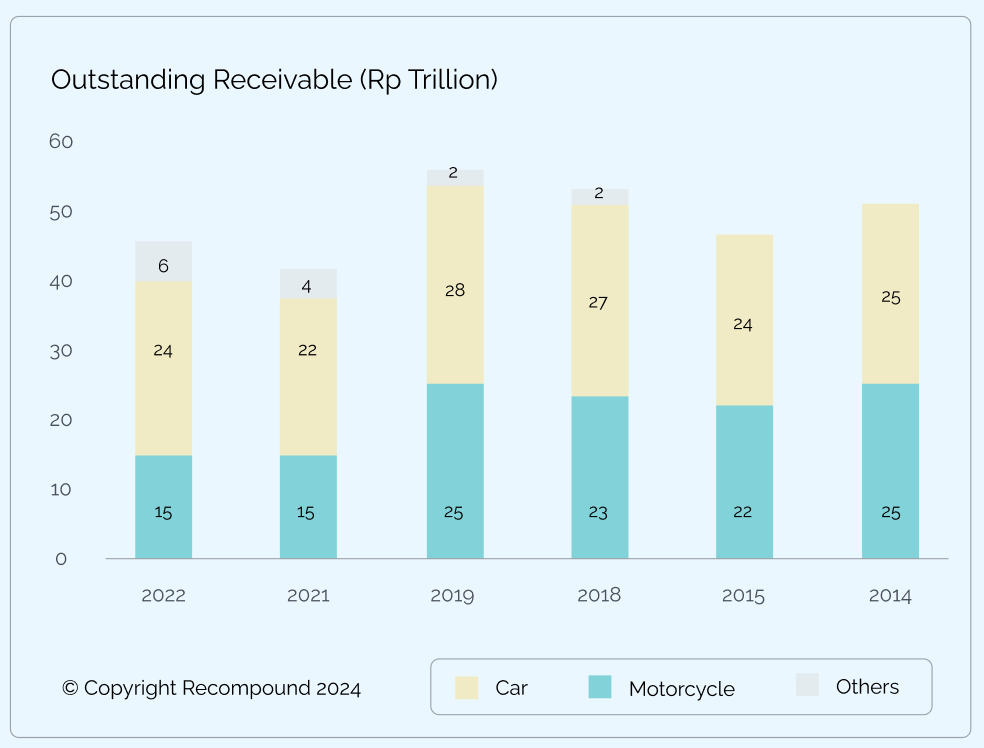

That means, Rp 100T * 10% or Rp 90T is Adira’s outstanding receivable. Outstanding receiveable is only a fancy term to say that Adira is expecting to receive Rp 90T worth of money in the future.

What counts as Adira’s revenue? It is that Rp 90T multiplied by the interest that is charged (let’s say 10%). This means that Adira’s revenue is Rp 9T.

However that is not all. Instalments begin immediately but does not have to end on that same year. In previous years, Adira might provide financing as much as Rp 80T. Lets assume in the current year, 25% of that financing has been paid. Which means, Adira has an outstanding receivable of Rp 60T (Rp 80T * (100% - 25%)).

What counts as Adira’s revenue? It is that Rp 9T that we got earlier plus Rp 6T (Rp 60T times 10% interest) which gives us Rp 15T.

Now just to make things crystal clear, we have 3 types of financial metrics here:

Outstanding receivable: this is the total amount of payment Adira expects to receive from its customers from its financing activities. For simplicity (assume Alex is the only customer), this comprises total financing minus payment that has been collected from Alex (e.g., 360 mio for Prius - instalment money collected from Alex so far).

Revenue: is outstanding receivable multiplied by interest Adira expects to receive from from Alex

Profit: this is the revenue minus the cost (more about the cost later). The profit is what we are concerned with as an indicator of how financially healthy Adira is as a company

Kudos for reading and re-reading the previous paragraph, because now you have conceptually understood how Adira accounts for their revenue. Now let’s put in some real figures.

From the outstanding receivable, we can derive the revenue based on interest that is payable to Adira (multiply each financing that has not been paid by the interest) and obtain the revenue track record.

For each segment of financing, there is a cost that is associated. We will discuss about the cost structure in the later part of the blog. But once we figure this out, we can calculate the profit per each segment of financing displayed below.

From the numbers above, we can highlight a couple of trends (insights).