Disclaimer: this is not an equity research report and it is not a buy, sell or hold recommendation on any mentioned stock. Views mentioned in this article is the authors’ views solely for the purpose of education and should not be construed as financial advice. Views presented also do not necessarily reflect the view of Recompound as a company. Purpose of this blogpost is to highlight a brief overview of our thought process of getting a better picture of a public company.

PT Total Bangun Persada Tbk. is a privately owned (non-government) construction company in Indonesia.

It specializes in building commercial high-rise & office buildings.

If you live in Jakarta, you should not be a stranger to some of their high profile projects:

Central Park

The Pakubuwono Residence

Astra Tower

Pondok Indah Mall 3 & Office Tower

I have to admit, the term “construction company” may not have the best reputation in Indonesia. This is understandable, considering the negative news surrounding them (especially so for state-owned ones):

At a glance, construction sector is one of the hardest-hit sectors by COVID-19 because mobility and outdoor business activities were greatly reduced. Consequently, their earnings plummeted, including those of TOTL (all figures in the table below are in billion IDR).

Fast forward to 2023, mobility and outdoor business activities recovered. TOTL was able to turn around its earnings, while most of its state-owned peers are still struggling (all figures in the table below are in billion IDR):

Same business model, different outcomes in their earnings (and consequently, their long-term stock price performance). How come?

Company Profile & Structure

Total Bangun Persada was initially established under the name PT Tjahja Rimba Kentjana on September 4, 1970.

To this day, the company has been engaged in construction business for more than 50 years. In 1981, the company restructured its business and changed its name into PT Total Bangun Persada Tbk.

They officially became public on July 25 2006.

When analyzing a company, it is of paramount importance to be familiar with the people who run the company. Specifically, we are interested in finding out TOTL’s Ultimate Beneficial Owners (UBO).

UBOs are the people who ultimately owns and controls the company. Therefore, it is very important to us that these people:

Have good track record

Are competent in running their business

Are fair to their minority shareholders (like us!)

As the saying goes: “Good people make good times possible” 🙂

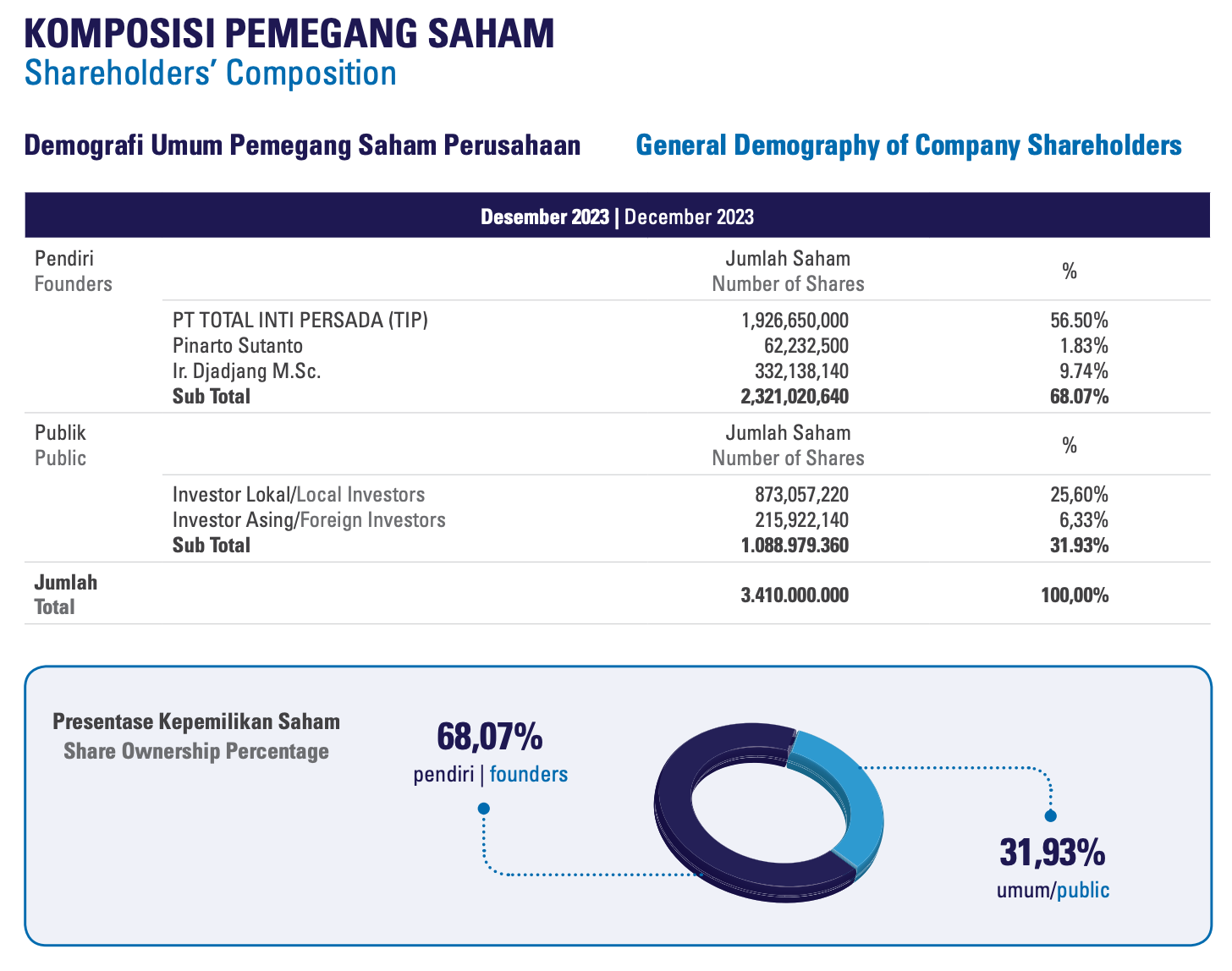

Let’s first take a look at their shareholder composition list:

PT Total Inti Persada is the majority shareholder of PT Total Bangun Persada Tbk.

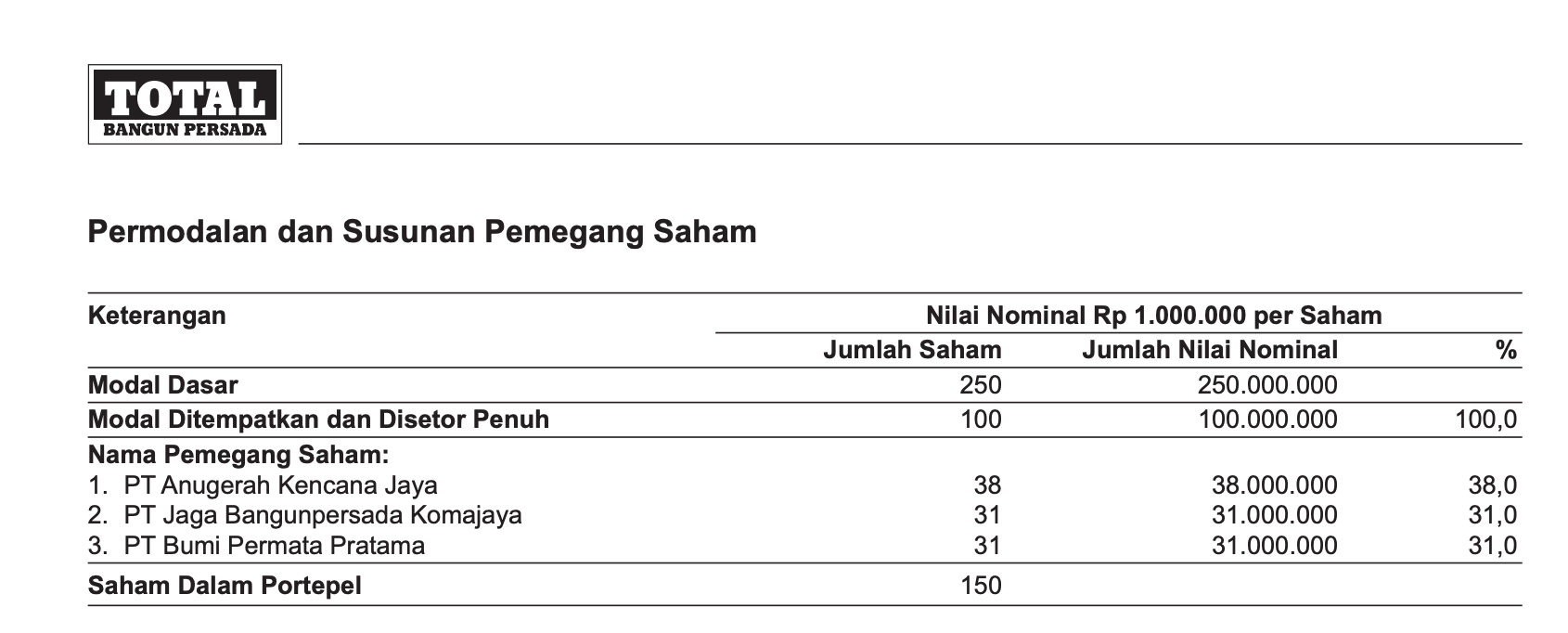

Let’s find out the controlling shareholders of PT Total Inti Persada (TOTL’s controlling shareholder):

…And here is the list of directors and commissioners of PT Total Inti Persada (TOTL’s controlling shareholder):

Let’s move up 1 more level, who are the controlling shareholders of:

PT Bumi Permata Pratama

PT Jaga Bangunpersada Komajaya

PT Anugerah Kencana Jaya ?