Transfer Pricing: A Retail Investor's Nightmare

Why this is very important when investing in the public market

What is Transfer Pricing?

An act of “transferring” the “wealth” of a company (in this case its profits), to another affiliated companies, owned by the same majority shareholder.

These affiliated companies are usually private and inaccessible to us, retail investors.

Why is it Bad for Us, Retail Investors?

As minority investors, we have zero control over a company’s decision making.

We are at the mercy of the management & the owners, who are usually the majority shareholders, to not plunder the profits from the public company we are invested in into another affiliated companies they own.

Okay, but why is this bad for us?

This is because when a public company’s profits get transferred to affiliated companies they own:

We do not experience the same earnings growth like other public companies within the same sector

We get less dividends compared to the owners’ and their families. You could read this post for more reference.

A Simple Case Study

In practice there are various ways a company’s profits can be “transferred” into other private companies. There is no fixed formula. This completely depend on:

The company’s business model

The corporate structure

The integrity of the management

For the sake of brevity, we will show you one simple case study how a company’s profits can be “transferred” into another.

Welcome to the country of Wakanda

In this country, there exists an entrepreneur Mr. Mchumba who owns a highly successful instant noodle brand WakandaMie.

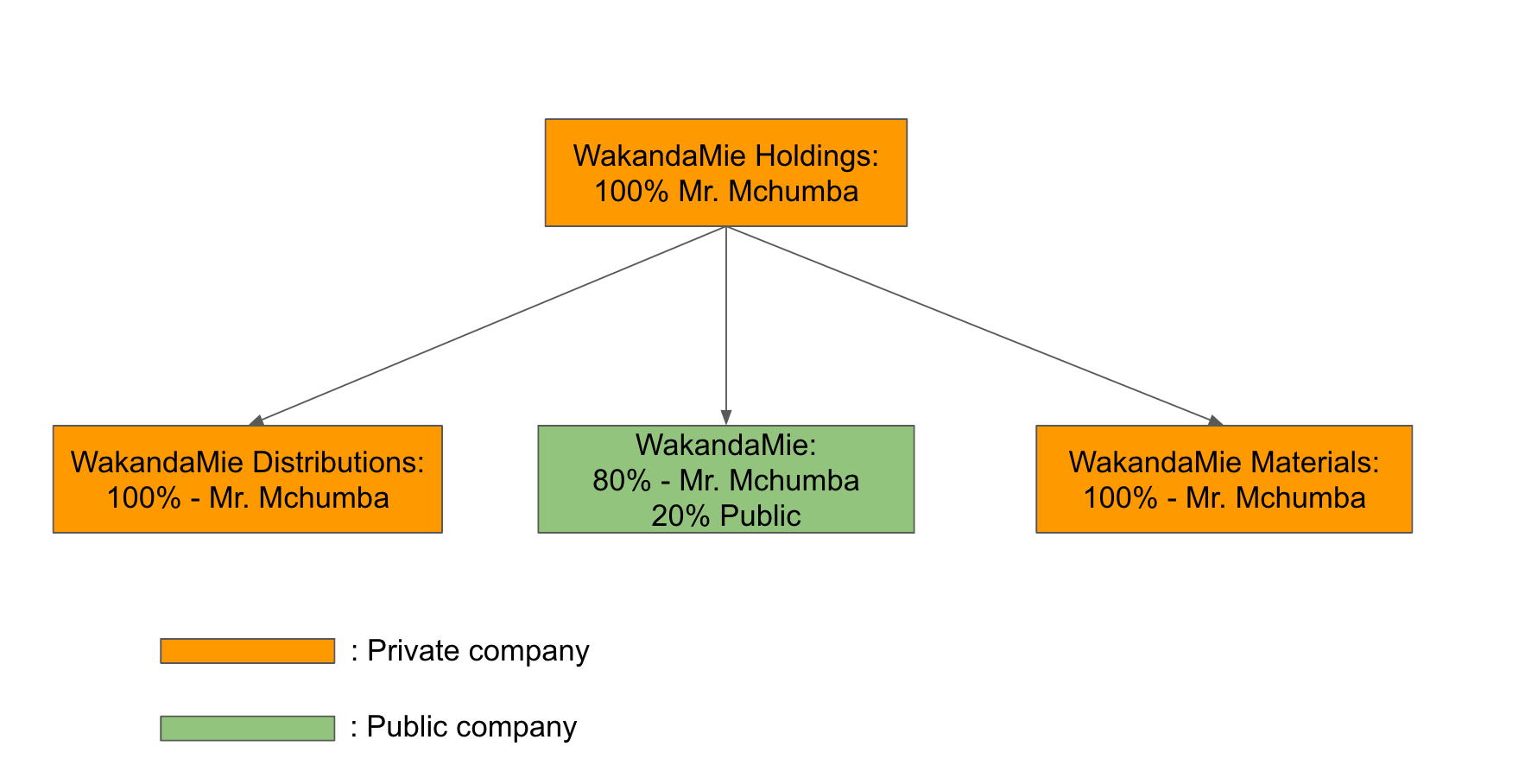

The diagram below displays the corporate structure and ownership composition of WakandaMie:

A simple explainer of each company:

WakandaMie Holdings: A holding company for its 3 child companies

WakandaMie Distributions: A privately owned, sole distributor of the WakandaMie brand

WakandaMie Materials: A privately owned, sole raw ingredient supplier of WakandaMie (flour, oil, seasonings, plastic, etc.)

WakandaMie: 20% publicly owned, the instant noodle manufacturer

Point of Failures

From this corporate structure, we can already pinpoint two potential point of failures:

Distribution cost: WakandaMie solely relies on WakandaMie Distributions to distribute its instant noodles to hundreds of stores throughout the country

What if Mr. Mchumba decides to increase its distribution cost way above market rate?

WakandaMie’s distribution cost will skyrocket, hence hampering WakandaMie’s profits and dividends

Raw material cost: WakandaMie solely relies on WakandaMie Materials (flour, oil, seasonings, plastic ) to produce their instant noodles

What if Mr. Mchumba decides to increase the price of flour way above the market price?

WakandaMie’s cost of goods sold will skyrocket, hence hampering WakandaMie’s profits and dividends

When the events above happen, retail investors suffer the most, because we are unable to invest in WakandaMie Distributions nor WakandaMie Materials.

Remeber they are private companies which enjoy profits after milking the public company WakandaMie.

Parting Words

The case study above is just one simplified example, there are other “Kungfus” on how a company owner can drain the money to benefit their other private companies at the expense of the public company owned by us.

In the real world, it’s not easy to detect these events because they are much less obvious. One must have a firm grasp on a company’s owners & business model.

At Recompound, when we are performing due diligence on a public company, we pay close attention to these events and whether or not we are disadvantaged as retail investors.

This is because we exclusively invest in public companies and we have no control over management’s decision. One fatal decision and our revenue goes down the drain.

At the end of the day, we only eat from our clients’ portfolio growth.