When I introduce myself to strangers at a dinner party in Jakarta and mention that I work as an investment advisor, I usually get a very specific reaction.

They nod knowingly and assume my life is a high-octane montage of staring at flickering stock tickers, obsessing over price charts, and frantically watching red and green candles form on six different monitors, 24/7.

But here is the boring (or perhaps, exciting) truth: contrary to popular belief, we rarely look at candle charts during market hours. In fact, we sometimes barely look at the stock price at all.

As a matter of fact, Toby sometimes get confused as to when are the holidays and the opening hours of the market. Because to be completely frank, he could not be bothered looking at the intraday movement of the stock price.

We Buy Businesses, Not Tickers

At Recompound, when we invest in stocks—even the public ones listed on the IDX—we view it as buying a piece of a business. Naturally, this means the current stock price is less interesting to us than the value behind it. We care about the price only relative to the company’s ability to produce future earnings.

Instead of asking “where will the chart go next?”, we spend our days asking:

How does this business actually make money?

What new developments are shifting the tectonic plates of their sector?

Is the management prudent with their capital allocation?

We recently deep-dived into this philosophy in our Investing Manifesto (go take a look if you haven’t yet!).

So, if I’m not staring at charts, what does a “day in the life” actually look like?

The Closed-Door Meeting

Recently, it looked like sitting in a meeting room with the management of GMF AeroAsia (GMFI)—kudos to our friends at Stockbit for the opportunity.

For context, GMFI is currently navigating a significant turnaround. Due to the pandemic, the company has been operating with a capital deficiency (negative equity).

To fix this, they are executing a Rights Issue (PMHMETD II) where Injourney Airports (PT Angkasa Pura Indonesia) will inject capital via an “inbreng” of land assets worth roughly IDR 5.66 trillion.

The goal on paper is simple: turn the equity positive so the company can improve its financial standing and eventually distribute dividends again. But during the discussion, we uncovered a much deeper insight that you won’t find on a candlestick chart.

We learned about the shifting landscape of State-Owned Enterprises (BUMN) under the new Danantara agency.

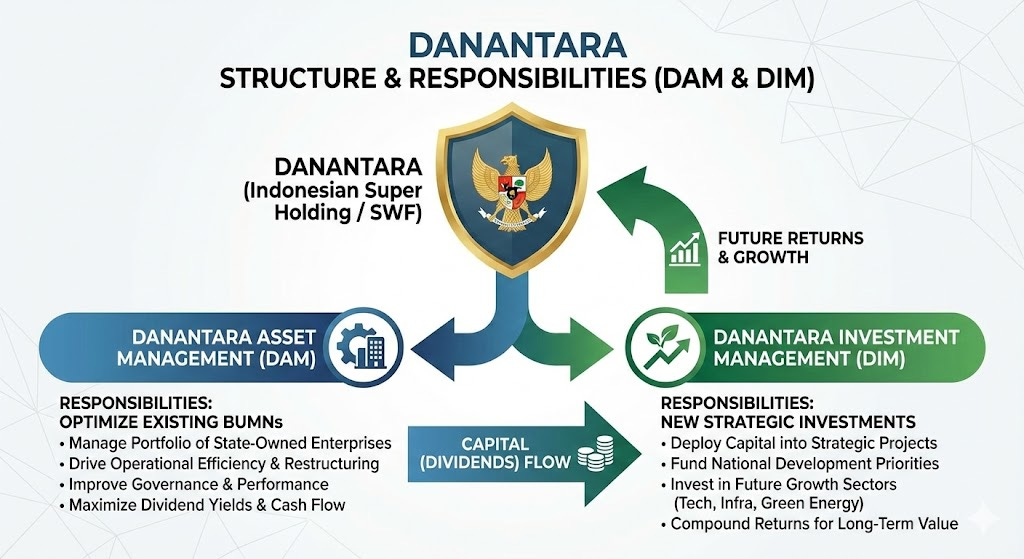

The Engine Under the Hood: DAM vs. DIM

We know that Danantara is divided into two distinct arms with very specific mandates to drive national growth:

DAM (Danantara Asset Management): Its job is to manage the existing portfolio of BUMNs. The mandate here is ruthless efficiency—streamlining the structure (e.g., consolidating 1,000 entities into 200) and optimizing assets to maximize dividend payments.

DIM (Danantara Investment Management): Its job is to take those cash flows and reinvest them into new, strategic national projects for future growth.

This creates a powerful, self-reinforcing incentive loop.

DAM has every incentive to force its BUMNs to be profitable to fuel DIM’s investments.

Not Just “Omon-Omon”

You might be thinking, “This sounds good on paper, but is it just omon-omon (empty talk)?”

According to Andi Fahrurrozi, the Director of GMFI, this shift is real and proven firsthand.

He shared a candid story that highlights the difference: This Rights Issue scheme involving the asset inbreng wasn’t a new idea; GMFI had actually been trying to execute this since 2023.

Back then, however, they hit a brick wall. For those newer to stock investing, Rights Issue is a corporate action, that is inorganic, partially as a solution to add equity to the company (note that the company’s operating with a negative equity). Now because it is a state owned enterprise, management of the company would face a number of blockers that are usually not faced by a normal non-state owned company.

Number one is bureaucracy.

You might think that if you have a state-owned enterprise wanting to do a corporate action like rights issue, you would require the approval from the ministry of State Owned Enterprise. Well, it turns out, back in 2023, they also had to get the approval from DPR (House of Representative) due to the complex ownership structures. Which ultimately failed.

Fast forward to today: under the Danantara framework, what was once an impossible bureaucratic climb became a super-quick execution. Because both entities now sit under the same “parent,” the transaction didn’t need to jump through the old political hoops. It became a streamlined process of moving assets from the left pocket to the right pocket to unlock value.

This proved to us that the “Danantara Effect” is not just a slogan—it is already actively de-bottlenecking the state’s most sluggish assets.

Your Edge vs. “The Sudirman Boys”

This brings me back to you.

At Recompound, we serve hundreds of clients who are high-performing professionals across various industries. Believe it or not, your edge is often much sharper than that of the professional fund managers sitting in high-rises on Sudirman Street.

Why? Because the big institutional firms often cannot—or will not—invest in smaller-cap companies that haven’t yet hit their radar.

Furthermore, the “Sudirman boys” often flex their expensive Bloomberg Terminals, assuming that a $24,000-a-year subscription gives them an insurmountable advantage.

But here is the funny story: no amount of satellite data or premium news feeds can beat info lapangan (first-hand, on-the-ground intel).

While they are looking at spreadsheets and terminal screens, you are looking at the reality of your industry.

You know the supply chain bottlenecks before they show up in a quarterly report. You know which competitors are cutting corners and which are truly innovating. You understand your sector’s business process end-to-end.

That is a proprietary advantage that no machine can replicate.

So, if you have a unique business insight based on your professional experience—whether it’s a shift in consumer behavior or a new regulation impacting your field—don’t be shy. Please share it with us in your WhatsApp group!

We are always happy to learn from you, because at the end of the day, the best investment insights don’t come from a terminal; they come from the people building the businesses.

⚠️ Important Disclaimer: We Are NOT Telling You to Buy GMFI

Before you rush to your broker app, please pause. While the turnaround story is fascinating, we are not insinuating that you should buy GMFI stock right now. There are still significant uncertainties and risks that need to be resolved before the company becomes an investment-grade dividend payer:

Retained Earnings are Still Negative: Even after the Rights Issue improves the equity, the company still holds a massive deficit in retained earnings. By our calculations, it would take approximately 15 years of organic earnings just to clear this deficit and turn it positive.

Dividends are Far Away: By law, a company cannot pay dividends while its retained earnings are negative. Unless there are further inorganic corporate actions (like a Quasi Reorganization) to wipe this slate clean faster, shareholders will be waiting a very long time for cash returns.

Execution Risk: The “Quasi Reorganization” path is complex and requires further regulatory and shareholder approvals. Until those are concrete, the timeline remains speculative.

Based on the risks that we have identified earlier, you might be questioning “Why are we playing it safe?” It might be the case that there will be significant upward price movements tomorrow, no?

Well, we believe that playing it safe, at least in the stock market, is the single most important attribute that allows compounding to do the heavy lifting over time.

We wrote a separate piece explaining what “playing it safe” actually means in practice—and why most investors misunderstand it entirely.

If you’re curious, you may find it worth reading.

P.S. There is another BUMN with much less execution risk compared to GMFI, is still largely unnoticed by the market, its existing business valuation is already cheap and we are currently actively studying it. It has the potential to benefit even more from this Danantara restructuring wave, with much lower risk compared to GMFI.

Visit core.recompound.id to learn more.