Disclaimer: This article is intended for educational and informational purposes only. Nothing in it constitutes — and it should not be construed as — financial, investment, tax, or legal advice, nor as an offer, solicitation, or recommendation to buy, sell, or hold any security or currency. Specific companies and tickers mentioned below (including the banks and blue chips in the tables) are used purely to illustrate a point, not as endorsements or recommendations.

Figures such as index levels, exchange rates, and valuation multiples move constantly and may be out of date by the time you read this. Any forward-looking statements are opinions, not predictions. All investing carries risk, including the possible loss of capital, and past performance never guarantees future results. Please do your own research, and consider speaking with a licensed professional before making any decision. Reader’s discretion is advised.

If you find it useful, restack or share this article to your circle :)

We normally keep our monthly letters between us and our clients. This month we are making an exception, because the question landing in our WhatsApp groups is the same question landing in every Indonesian investor’s group chat right now. So we are publishing our answer for everyone.

First, what just happened. Since mid-May 2026, the broad market has fallen roughly -12%. On 5 June alone, the IHSG dropped -4% in a single day. Measured from the January 2026 peak, the index is now down about -39%. This is no longer an ordinary correction. By depth, it now sits alongside the worst Indonesian sell-offs of the last three decades.

We will not pretend this is comfortable. It is not. But we have been here before — not this exact scene, but this exact feeling.

The question everyone is asking

“I don’t really trust the government. So why keep holding, and not sell everything now?”

It is a fair question, and we want to answer it directly rather than wave it away. Distrust of policy is reasonable; many of you have lived through enough market cycles to have good reason for doubt. But notice that “I don’t trust the government” and “therefore I should sell everything now” are two different statements. The first is a worldview. The second is a market-timing decision — and market timing is a far harder, far less forgiving game than most people realize.

Below are five reasons we think panic-selling at this level is not the wise move.

Reason 1 — Nobody can time the exact bottom, and the news flow is the worst possible guide

We say this as people who watch this market every single day: we do not know where or when the bottom is, and neither does anyone shouting on social media. Kita bukan dewa. If we are honest, the loudest market “signals” — viral posts, doom threads, confident predictions — have historically been a contra-indicator, not a guide.

You don’t have to take this on faith. In early 2025, sentiment reached what we can only call absolute madness — the moment Danantara was first formed and Trump announced his tariffs, the consensus was that Indonesia was uninvestable. That precise moment of maximum skepticism marked the absolute bottom of that cycle. Those who sold into the panic locked in the loss. Those who held, and those who added, recovered and then some.

Right on cue: “Sell Indonesia” hits the front pages

On 5 June, the Straits Times ran a Bloomberg piece titled “’Sell Indonesia’ sweeps trading desks as Prabowo tightens grip”. Foreign investors are now openly giving up on Indonesia — what traders call capitulation. A detail worth noting: the fund manager quoted in the piece, by his own account, exited Indonesia back in 2024 — the bearish view is two years old. Only the megaphone is new. And that is how this genre works: the “investors flee” story gets written after the fall, once the gloomy narrative is safe to print.

The timing of these headlines tells us a lot. We went back through every Indonesian crisis since 2008 and matched the loudest foreign "giving-up" headline against the actual market bottom:

Read the middle column again. In all five resolved episodes, the loudest foreign capitulation printed within roughly three weeks of the bottom — sometimes just before it, sometimes just after. And a buyer on the very day the doom article ran — not at the perfect low — was up between +14% and +70% one year later, five out of five times. The lag is the signal: these stories need a large drawdown to already exist before they can be written. By the time they are printed, the sellers are usually almost done selling.

One honest caveat, because we promise no cherry-picking: 1998 is the counterexample — the year the apocalyptic coverage was right, the economy contracted ~13%, and buying the headlines was a value trap. The 1998 headlines read exactly like the 2026 ones; the difference sat in the fundamentals underneath, never in the headlines. Which is exactly why Reasons 2 and 3 below matter more than any base rate. (And on the specific fear that this is “the precursor of 1998”: the leading indicator of a 1998-style collapse is not the exchange rate — it is whether a “dollar bomb” of unhedged foreign-currency exposure sits on the banks’ balance sheets. FY2025 Net Open Positions: BBCA ~0.1%, BBNI 1.1%, BMRI 1.8%, BBRI 2.5% of capital, against a 20% regulatory cap, with industry capital adequacy around 26% and bad loans near 2%. The bomb is not on the balance sheets this time. Toby wrote the full analysis in The Dollar Bomb — worth ten minutes if 1998 is the fear keeping you up at night.)

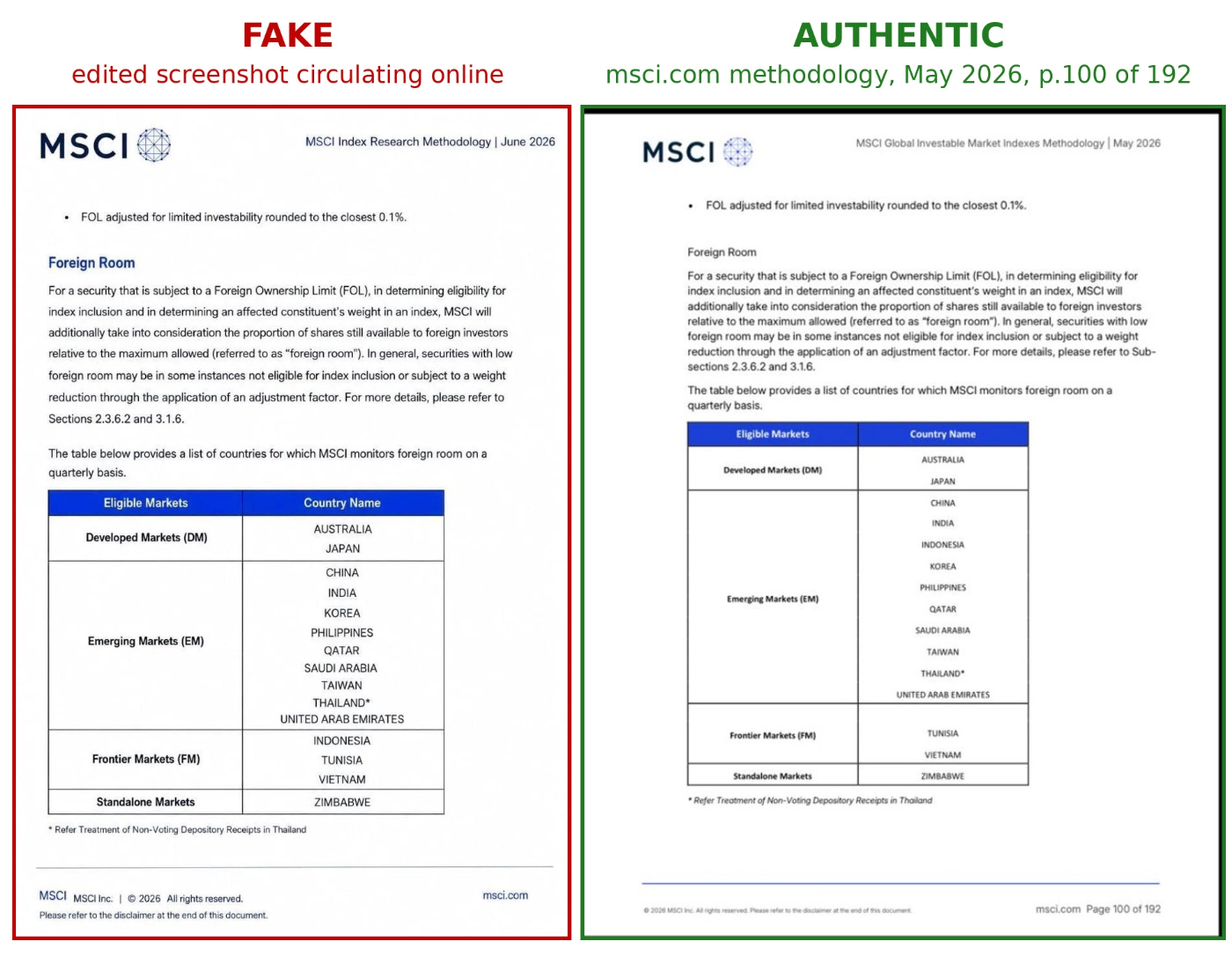

A live example — beware of the hoaxes circulating right now

We wish this were hypothetical. It is not. In the past days, an edited screenshot of an MSCI document has been spreading on social media and group chats, claiming that Indonesia has been reclassified to MSCI Frontier Markets. It looks official. It is fake.

The authentic document — the MSCI Global Investable Market Indexes Methodology, May 2026 (page 100 of 192, available directly at msci.com) — lists Indonesia exactly where it has been: under Emerging Markets, alongside China, India, Korea and Taiwan. MSCI has made no announcement changing Indonesia’s market classification. The fabricated version even carries a document title MSCI does not use and strips the page numbering.

Think about what this means: someone created a fake official-looking document to spread panic in a falling market. Whatever their motive — driving prices lower to buy cheaper, or simply chasing clicks — the people who sold because of that screenshot turned a hoax into their own permanent loss. Before acting on any explosive claim, check the primary source. Stay safe out there.

Reason 2 — The domestic economy is still genuinely strong

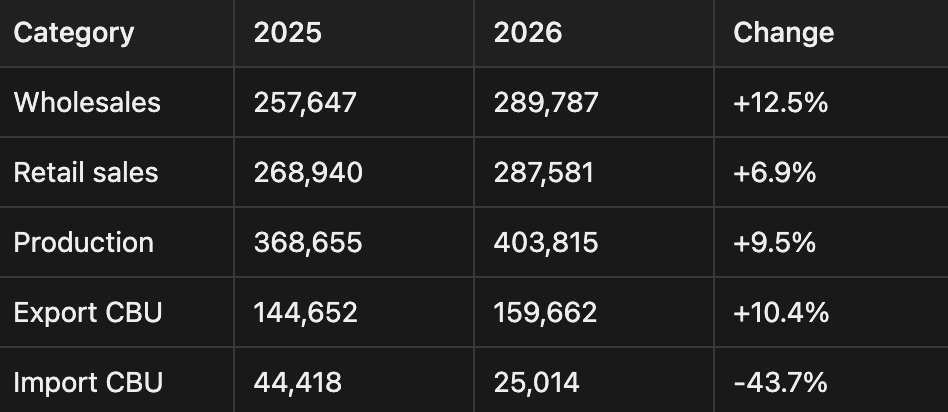

This is the part the market narrative is currently ignoring. Strip away the headlines and look at what Indonesians actually bought, produced, and exported in the first four months of 2026. The real economy is not in crisis. It is growing.

We know some of you don’t trust government statistics right now. Fair enough. So notice what we did: none of the numbers below come from the government. Car sales come from GAIKINDO, the carmakers’ own association. Motorcycle sales come from AISI, the manufacturers’ association. The PMI is compiled by S&P Global, a private American firm. And the banking data comes from BCA’s own published monthly figures. These are private-sector bodies counting their own units sold and their own loans booked, with no incentive to flatter anyone.

Car sales (GAIKINDO, YTD Jan–Apr 2026 vs 2025):

Motorcycle sales (AISI, YTD Jan–Apr 2026 vs 2025):

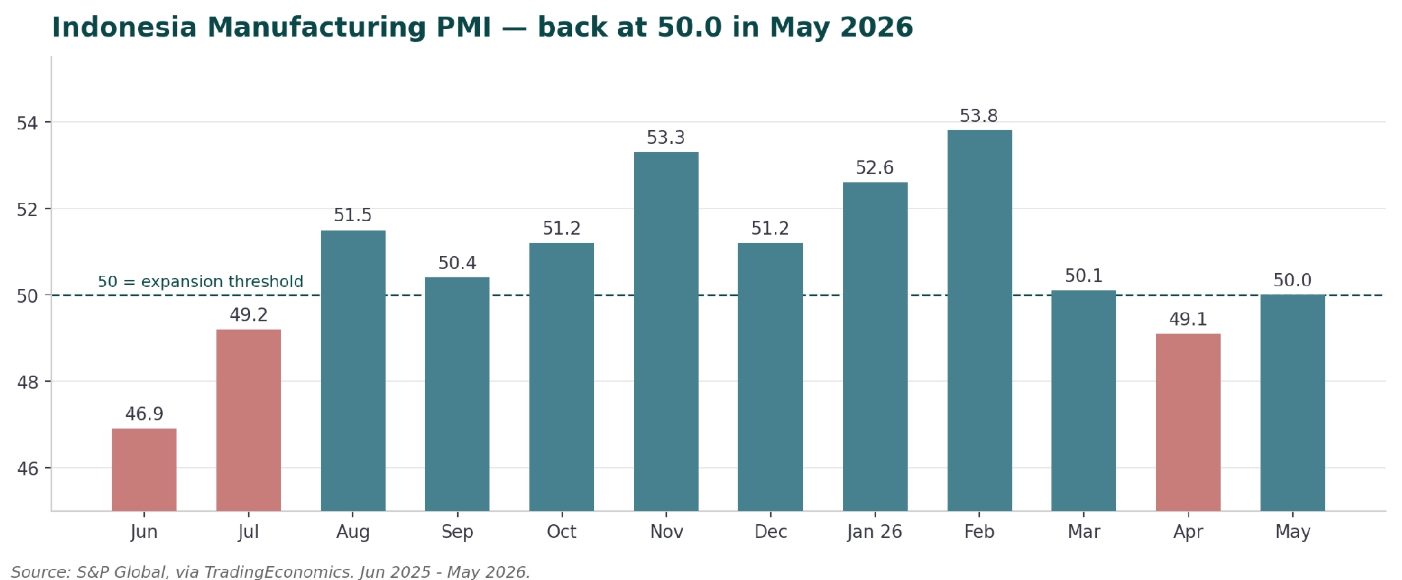

Manufacturing is steady: Indonesia's S&P Global Manufacturing PMI rose to 50.0 in May 2026 from April's 49.1, with new orders expanding for a second straight month at the fastest pace since February. There is genuine pressure — export orders are softer on the Middle East conflict, and input-cost inflation is high — but this is an economy operating at, not below, capacity.

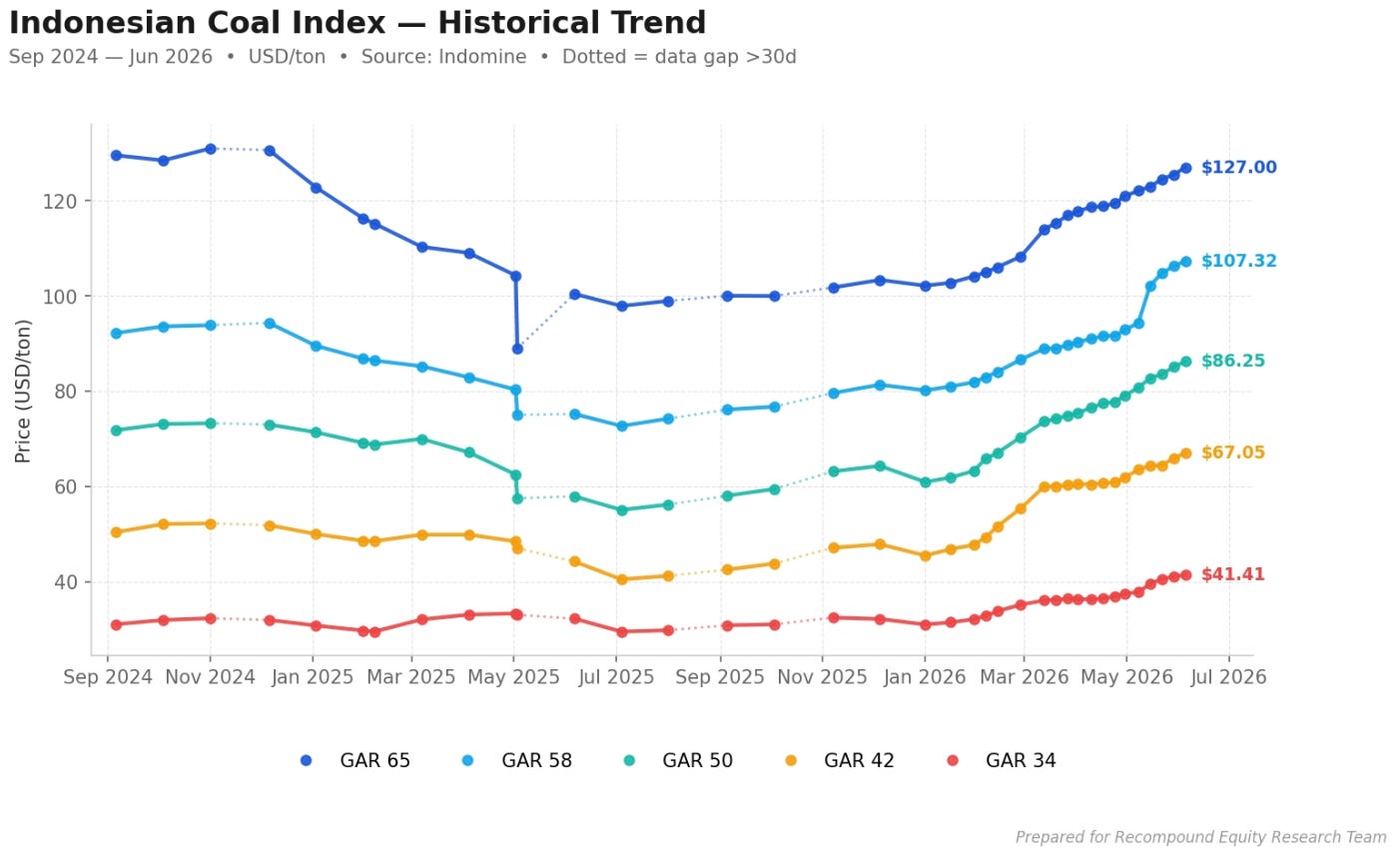

Commodities, which drive a large share of Indonesia's export earnings, are rising, not collapsing. The Indonesian Coal Index has turned firmly upward: GAR 65 is back to $127/ton and the lower grades have rallied hard off their mid-2025 lows (GAR 50 from ~$55 to $86).

And the bellwether of Indonesian banking is fine. BCA’s own 4M2026 figures show loans +4.5%, third-party funds +8.6%, operating profit +3.4%, and an annualized ROE of roughly 24.5% — essentially flat versus a year ago. The share price is down sharply; the bank’s earnings power is not.

Put plainly: the prices are behaving like a crisis. The economy is not. That gap is exactly where patient capital gets paid.

Reason 3 — Valuations are now back to GFC-2008 and Covid-2020 levels

Before the numbers, the simplest way to think about what a stock actually is.

Imagine someone offers you a house. Its fair value — the land and the building — is around Rp2 billion, and you have checked that it reliably rents out for Rp100 million a year. But the owner is trapped by debt and must sell fast, so he offers it to you for Rp1 billion. Would you take it? Of course. Now imagine that the day after you buy, a neighbour with an identical house panic-sells his for Rp900 million.

Do you rush to dump yours too — just because someone else sold cheaper, and maybe the next neighbour will sell at Rp700 million? Of course not. Your house still rents for Rp100 million a year. The falling sticker price next door changed nothing about what your house earns you.

A stock is exactly that house. It is a small ownership slice of a real business that earns real money. When the share price falls but the business keeps earning — keeps lending, selling, mining, paying dividends — a lower price is not a danger, it is a discount. This is the whole of value investing and nothing more: work out what a business is worth, and only buy when the price sits well below that.

So the only question that matters is how cheap that “rent” has become. This is the most striking finding of the month, and it surprised even us.

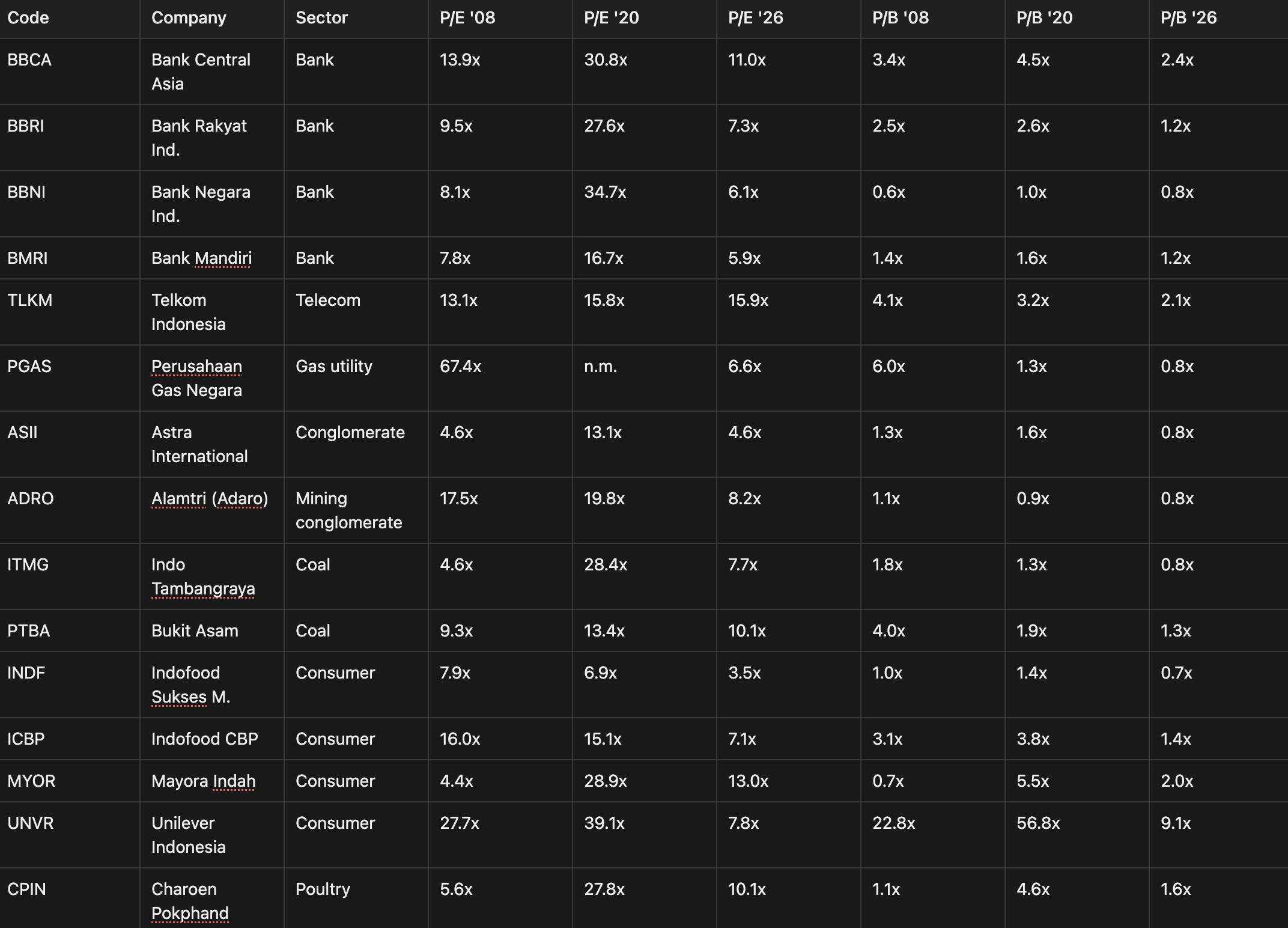

We pulled the full history for Indonesia’s largest, most systemically important “too big to fail” companies and compared today’s valuations against the two worst crises in living memory: the 2008 Global Financial Crisis and the 2020 Covid crash. Across the 25 biggest blue chips we measured, the aggregate price-to-book is now ~1.3x (at 5 Jun 2026 closing prices) — below the 2.0x at the end of 2008 and the 2.6x at the end of 2020. It is even below the price-to-book at the worst daily closes of both crises (~1.6x). On book value, these blue chips are cheaper today than they were at the bottom of 2009 and the bottom of 2020.

Here is the company-by-company picture:

Look at the banks — all 2026 multiples at 5 Jun 2026 closing prices. BBCA at 2.4x book versus 4.5x at end-2020. BBRI at 1.2x versus 2.6x. BBNI below book at 0.8x. Indofood at 3.5x earnings and 0.7x book — cheaper than at either crisis. These are not failing businesses. They are the same dominant franchises they were six months ago, now on sale.

We will be honest about the one exception in the table: Telkom (TLKM) is not cheaper than its crisis multiples on earnings — its Telkomsel profit has structurally declined, and we show it precisely because we are not cherry-picking. Cheap usually has a reason; the job is to separate the temporarily-cheap from the permanently-impaired. For most of this basket, we believe the cheapness is the market’s mood, not the businesses’ fundamentals.

“But 2008 and 2020 were global crises. This one is domestic!”

True — but it means less than it sounds. No crisis ever happens the same way twice. 2008 was a banking collapse imported from Wall Street. 2020 was a virus nobody had ever traded through. 1998 was a currency and political implosion. 2025 was a tariff shock plus a sovereign-wealth-fund scare. Each one had a brand-new shape, a brand-new reason why “this time it’s different and therefore unrecoverable” — that novelty is precisely what makes a crisis a crisis. If it looked exactly like the previous one, nobody would panic, and prices would never get this cheap.

What repeats is not the cause. What repeats is the arithmetic: dominant businesses, still earning, priced at or below book value — and the eventual reversion once fear runs out of sellers.

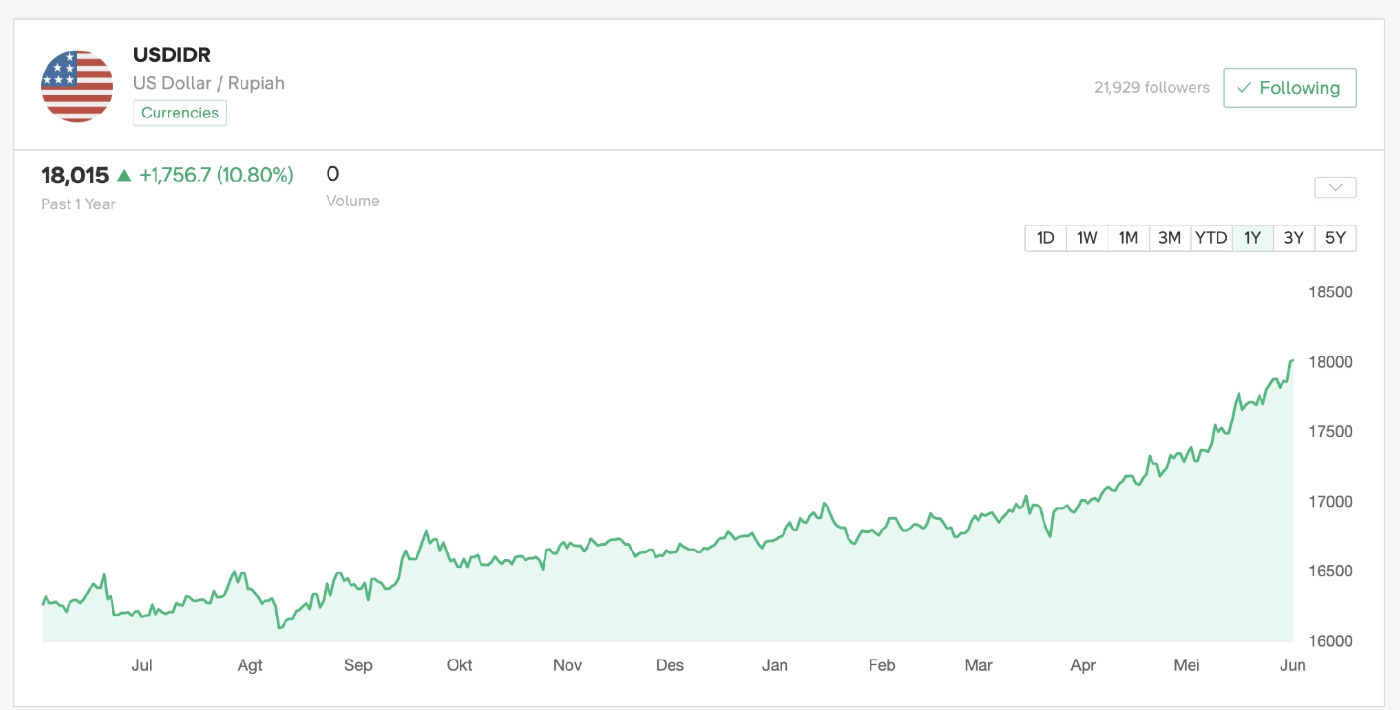

“You haven’t addressed the rupiah! USDIDR is past 18,000!”

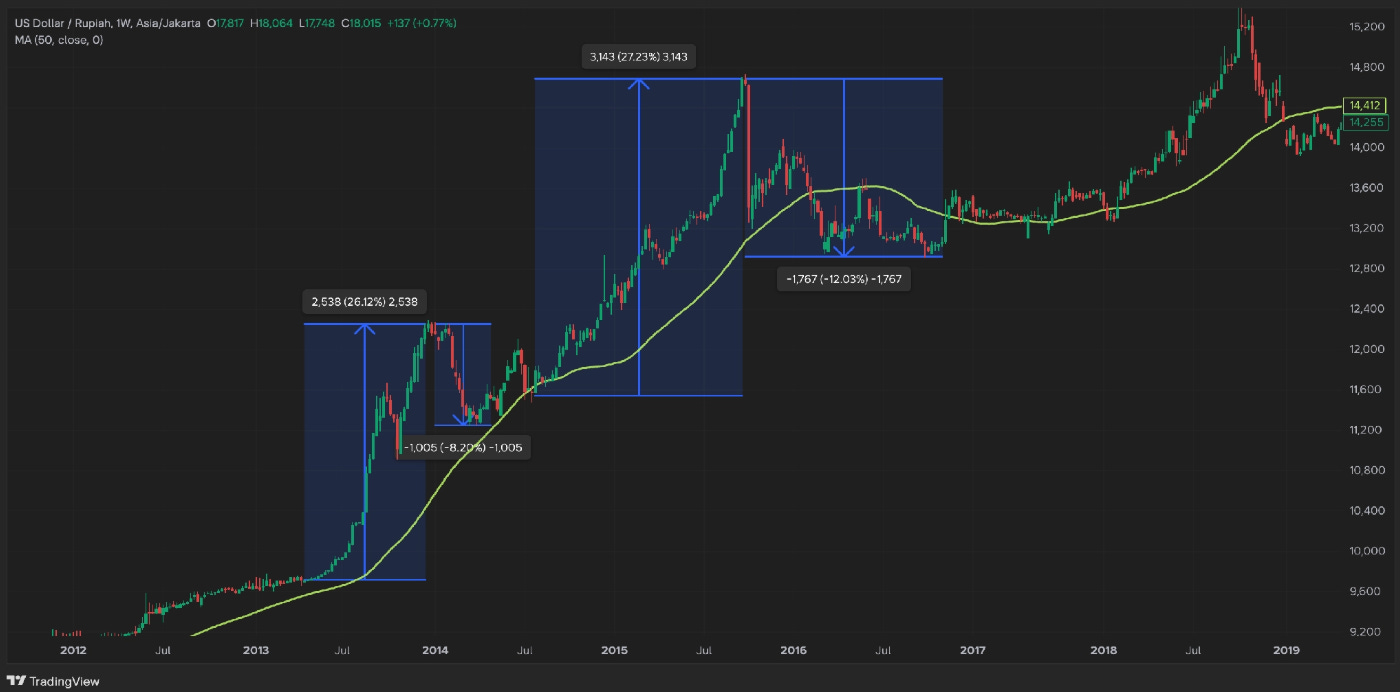

No — and here history repeats itself very consistently. Look at every past time the rupiah weakened rapidly. 2008: USDIDR spiked +39% (to ~12,650) at the very same time the stock market crashed — then gave back -29% as the recovery took hold. 2013 taper tantrum: +26%, then -8% back. 2015: +27%, then -12% back. 2020 Covid: +21% in weeks (to ~16,500), then -16% back within months. The same shape, four times in a row: the currency spikes together with the equity bottom, then recovers swiftly.

Rapid rupiah depreciation is a byproduct of foreign capital rushing out — the same selling that crushes stock prices — not a precursor of some second crisis still waiting to happen. Historically, the moment the currency is falling fastest has been close to the moment of maximum fear, and therefore close to the moment of maximum opportunity in equities. We watch the rupiah — it matters for importers and for inflation — but we read today's 18,000 print as the thermometer of the panic, not the forecast of the next one.

Reason 4 — After crises settle, the market has always recovered

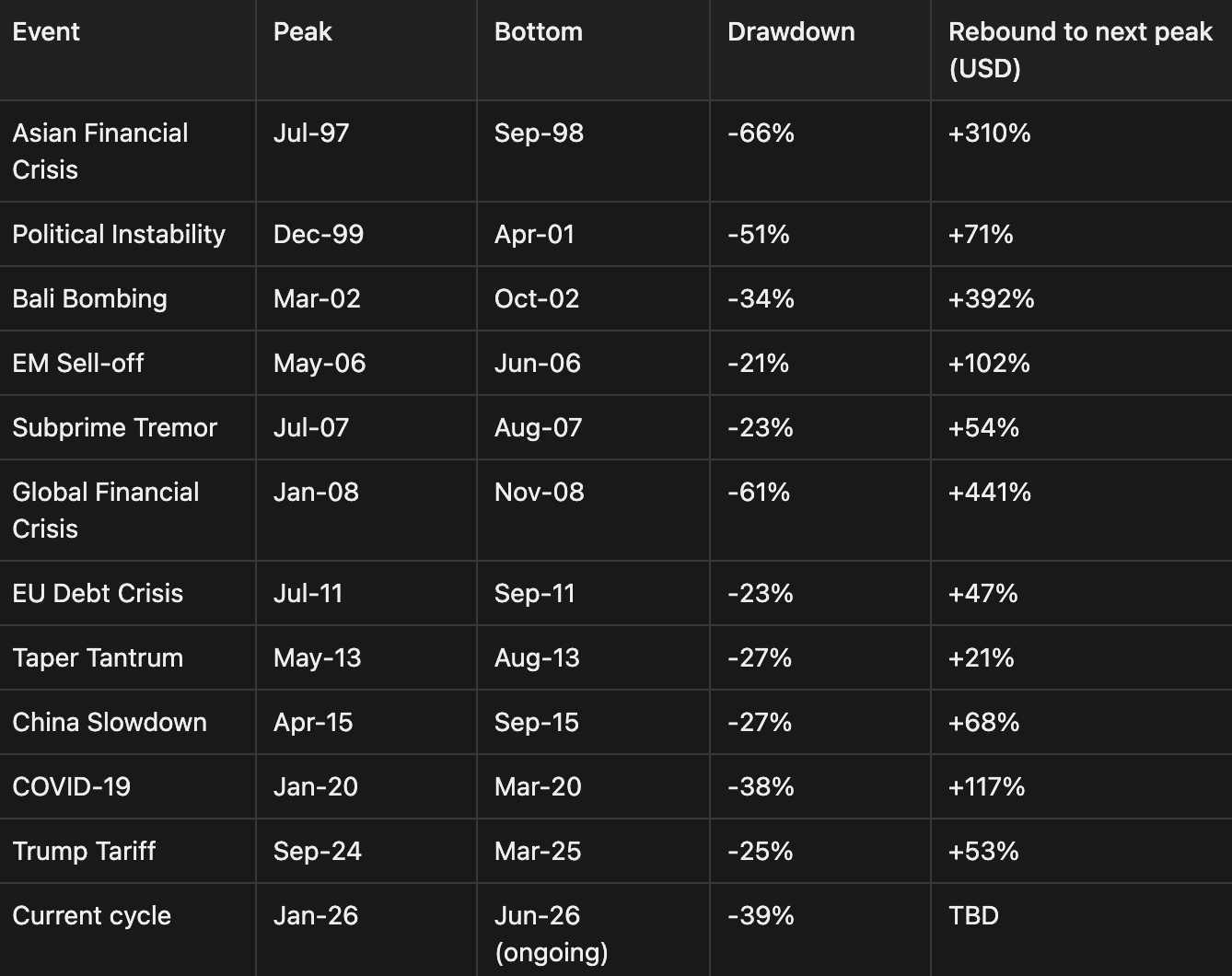

We are not asking you to take this on optimism. We are asking you to look at the record. Here is every major Indonesian market drawdown since 1997, the depth of each, and what happened afterward:

Twelve crises. Every single resolved one was followed by a recovery — and the deepest drawdowns produced the largest rebounds (GFC: -61% then +441%; AFC: -66% then +310%). We cannot promise this time follows the pattern, and we won’t. But the burden of proof sits with the person arguing “this time the recovery never comes” — not with the person who has three decades of Indonesian market history on their side.

Reason 5 — Even a frontier downgrade is already in the price

One fear deserves to be addressed head-on, because it is the engine of this whole sell-off: will MSCI demote Indonesia to Frontier Markets? Honestly — we think that is the wrong question. Whether the downgrade happens is MSCI’s decision, on MSCI’s timeline, and nobody on your feed knows it. The investable question is different: has today’s price already assumed the downgrade happens?

First, for the record: we think the odds of demotion are lower than the panic implies, because the exchange is not sitting still. In the space of months, BEI and OJK have delivered exactly the reforms MSCI asked for: disclosure of every shareholder above 1%, the minimum free float raised from 7.5% to 15% (compliance by March 2027–2029), and a Hong Kong-style High Shareholding Concentration list that names tightly-held companies publicly. MSCI’s May review kept Indonesia on hold, under restrictions — a yellow card, not a red card — while it assessed these reforms.

But let’s be conservative and assume the worst-case scenario anyway — with numbers, not feelings. Take Bank Mandiri (BMRI), one of Indonesia’s largest banks, as an example.

One of the textbook ways to ask “what multiple is fair for a company?” is the Gordon Growth Model:

In words: r is the yearly return an investor demands before bothering to own the stock. Its base is the 6.9% government bond yield — the risk-free alternative — and note that 6.9% is itself already a pessimistic number: it carries this year’s panic inside it. On top of that base, shareholders demand an extra premium: roughly the 4.3 points that even safe US equities command over bonds, plus another ~2.4 points for Indonesia-specific risk (derived from Indonesia’s sovereign default spread of ~1.8 points at its Baa2 rating, scaled up by ~1.3x because equities swing harder than bonds). Indonesia’s equity risk premium therefore sits near 6.7%, and the total hurdle at 13.6%.

Even against that already-pessimistic bar, with BMRI paying out 80% of earnings and growing at a deliberately harsh 3% — the bank compounded earnings at double digits over the past decade, and its retained profits alone fund ~4% — the fair multiple is 7.5x earnings.

BMRI actually trades at 5.8x (price as of 5 Jun 2026). Run the formula backwards: what hurdle rate would make 5.8x fair?

Today’s price is only “fair” if you demand a 16.6% return from Indonesian equities, permanently. That is three full percentage points of additional, permanent risk silently baked into the price. How big is three points? A BI rate hike is 0.25. A one-notch sovereign downgrade moves the risk premium by roughly half a point. The taper tantrum and Covid — real crises — lifted Indonesia’s equity risk premium by one to one-and-a-half points at their worst. Three points is not “more bad news”; it is a re-categorization — the market silently moving Indonesia into a different risk class altogether. And the only candidate event of that size on the table is the frontier downgrade. The fear is not hypothetical; it is literally the number inside the price.

Which leads to the fork: if the downgrade never comes, today’s prices are pure panic, and panic gets repriced. If it does come, today’s prices already contain it — the bomb has already gone off, and the market is trading at post-explosion prices. And while everyone waits, these companies keep paying: BMRI’s dividend yield alone is already in double digits — around 12% at the 5 Jun 2026 price, based on last year’s dividend.

“But won’t the forced selling cause another leg down?”

A sharp objection: the fear may be priced in, but the mechanical selling is not. Index funds do not sell on fear — they sell on the effective rebalancing date, when the rule says they must. We saw this in May: the MSCI changes were announced on 13 May, yet the roughly US$1.1 billion (~Rp19.5 trillion) of passive outflows hit on the 30 May effective date — and prices still moved on that day, even though everyone had known for two weeks. So yes: if a downgrade eventually happens, there will be forced selling that has not happened yet. Another leg down from that flow is a real possibility. Three things keep it in perspective.

First, the downgrade is a tail risk, not the base case — the exchange is visibly fixing what MSCI complained about, and reclassification is a slow, multi-review process. What the market is doing today is charging a near-certain discount for an unlikely event.

Second, even in that scenario the seller is limited. After the May purge, Indonesia is already down to roughly 0.5% of the EM index — the passive money that can still be forced out is a known, finite amount: a one-time seller with a deadline, not a permanent change in the businesses. The companies do not know they got downgraded. Index membership changes the price of a stock, not the business behind it.

Third, run the simple math on what a flow-driven crash actually does to a long-term owner. Imagine a stock at 1,000 paying a 100 dividend — a 10% yield. Forced selling cuts the price to 500: same business, same dividend, now a 20% yield — and every rupiah of dividend reinvested buys twice the earnings it bought before. A seller who must dump a cash-generating asset for non-business reasons is handing value to whoever buys it. The cost is a temporary drawdown; the gain is a permanently higher return on every rupiah invested at those prices.

Does any of this actually work? The honest scoreboard

You might reasonably say: these reasons are nice, but a philosophy is only as good as its behavior in a storm. Fair. So here is ours, in this storm.

Measured from the February 2026 peak, our clients’ overall portfolio drawdown is around -15% as of 5 June 2026, versus the broad market at roughly -40% — helped greatly by the dividends the companies kept paying through the chaos. (You can see the up-to-date comparison in the Portfolio Resilience section at www.recompound.id, updated daily. Past performance does not guarantee future results.)

In a market that fell -40% from its peak, holding the decline to well under half of that is not luck; it is the direct output of buying good businesses with a margin of safety and sizing every position so the bear case is survivable. And remember the arithmetic of holes: -15% needs +18% to climb out; -40% needs +64%. The portfolio that falls less needs far less heroism to recover.

Price swings are the entrance fee of long-term investing. The real risk is losing money permanently — not a price that is temporarily down.

So what should you do?

This is a public article, so we will not tell you to buy or sell anything. What we can do is leave you with the questions we ask ourselves, and the math that goes with them.

“Shouldn’t I just convert everything to USD?” Think through the mathematics of that switch. It means selling Indonesian businesses at 1.3x book — cheaper than the bottoms of 2009 and 2020 — in order to buy a currency at 18,000 (5 Jun 2026), after it has already risen +10.8% in a year. That is selling low and buying high, simultaneously. And as we showed in Reason 3, the rupiah’s sharpest weakness has historically arrived together with the equity bottom and then reversed. Currency diversification as a long-term structural decision is perfectly sensible — made calmly, in normal times. As a crisis response, it has usually meant locking in both sides of the loss at once.

“What’s the point of buying cheap when there’s no catalyst in sight?” The answer is counterintuitive: prices are only this cheap because no catalyst is visible. The moment a catalyst becomes obvious to everyone, the price has already moved and the discount is gone. 2025 was the textbook case: at the peak of Danantara skepticism and the Trump tariffs, no catalyst was in sight anywhere — that was precisely the bottom. Only after the market recovered did everyone busy themselves explaining what the “catalyst” had been. The market moves first; the narrative catches up later.

“And while waiting?” You are paid to wait. At roughly 8x earnings (5 Jun 2026 prices), the blue-chip basket’s earnings yield is about 12% against a ~6.5% government bond, and BBCA alone now pays a ~6.5% dividend yield — essentially the risk-free rate, with growth on top. Even in the skeptics’ sideways scenario, profits keep coming and dividends keep landing. Those who insist on visible signs of improvement will buy after the recovery, not before it.

What we will not do — and what we’d gently suggest nobody does — is panic-sell quality businesses into a fearful market to chase a bottom nobody can see. That is the one move with a reliable track record: of destroying long-term returns.

Closing

Look — we are humans too. We read the same headlines you do, every day, all day. Absorbing this much negative energy is draining, and we will not pretend otherwise.

But we have been doing this for four years — through the Covid hangover, the Russia-Ukraine war, the Danantara panic, the Trump tariffs, the Iran war, and now this. What carried us through every single one was not bold talk, and certainly not an ability to predict the future. It was discipline. Buy good businesses below their value, size them so the bear case is survivable, collect the dividends, and refuse — absolutely refuse — to panic-sell the bottoms or FOMO-buy the tops.

Tough times don’t last. Tough people do.

Cheers!

References

Bloomberg / The Straits Times (2026). “’Sell Indonesia’ sweeps trading desks as Prabowo tightens grip.” 5 June 2026. [The capitulation headline discussed in Reason 1.]

MSCI (2026). MSCI Global Investable Market Indexes Methodology, May 2026, p. 100. msci.com. [Indonesia’s authentic Emerging Markets classification; the basis for debunking the circulating hoax screenshot.]

GAIKINDO (2026). Indonesian automotive wholesales, retail, production and trade statistics, Jan–Apr 2026. gaikindo.or.id.

AISI (2026). Indonesian motorcycle domestic and export statistics, Jan–Apr 2026. aisi.or.id.

S&P Global (2026). Indonesia Manufacturing PMI, May 2026 release (50.0, up from 49.1).

Bank Central Asia (2026). Published monthly financial figures, 4M2026. [Loans +4.5%, third-party funds +8.6%, operating profit +3.4%, annualized ROE ~24.5%.]

Indomine (2026). Indonesian Coal Index by grade, Sep 2024 – Jun 2026. [GAR 65 at $127/ton; GAR 50 from ~$55 to $86.]

Stockbit; Recompound analysis (2026). Blue-chip P/E and P/B comparison, year-end 2008 and 2020 vs 5 June 2026.

Limanto, T. (2026). The Dollar Bomb. Recompound Blog, 5 June 2026. https://blog.recompound.id/p/the-dollar-bomb [Net Open Position analysis: why 2026’s banks are not 1998’s banks.]

Bloomberg via Free Malaysia Today (2026). BEI/OJK market reforms: >1% shareholder disclosure, 15% minimum free float, High Shareholding Concentration list. 3 April 2026.

Damodaran, A. (2026). Country risk premiums and sovereign default spreads. [Basis for the ~6.7% Indonesia equity risk premium used in the Gordon Growth exercise.]

nice insight. I do also think Indo is not hard sell at this point. Valuations are at “obral” sale position. But the question remains when will global capital and private sector confidence returns, because these what made Indo’s valuations rerated in the past.

Nice! I remember trading indo quite fondly. Now it’s a bit harder that I am no longer in the region. I recently wrote a 3 part series on global investing, here is the Asia edition one (if you like, you can find the links to the Europe one and Americas one as well):

https://rudajev.substack.com/p/episode-29-tour-du-globe-series-asia