Disclaimer

Disclaimer: this is an opinionated article, supported by various datapoints that can be found publicly. Its sole intention is to express our opinion regarding the industry to our readers. It should not be construed as financial advice. Any stocks that are mentioned in this article is not a buy, hold or sell recommendation. Views expressed by the author is personal and does not necessarily reflect the view of the company.

First of all, let me be clear at the very beginning of this article that: I hope I am wrong.

I do not wish P2P Lending to go bust considering that it has been a popular investment option amongst many working class in Indonesia. However, I do wish that through this writing, people are made to be more aware of the risks they are taking when investing in P2P. Let’s begin.

What is Peer to Peer (P2P) Lending?

According to Otoritas Jasa Keuangan (OJK)(https://sikapiuangmu.ojk.go.id/FrontEnd/CMS/Article/20566), P2P Lending is an online platform that provides facilities for lenders to offer direct loans to borrowers.

The aim of this platform is to provide loans which are more accessible compared to traditional financial institutions like banks. Borrowers do not need to provide a collateral on their loans.

Over the past few years, P2P has been advertised as an investment option which is relatively “safe” with higher returns compared to time deposits / fixed income / equity, with many influencers endorsing the product.

However, being equity investors ourselves, we have had the opportunity to study business models of many publicly listed companies in Indonesia.

Looking closer at P2P Lending’s business model, notably backed by VC money, we knew that this model is likely to be unsustainable in the long run. Especially when no additional funding is available (from VCs / IPOs / rights issue / private placement), it is just a matter of time before many of these companies go boom boom ciao.

P2P Lending: Business Model

The P2P lending business model is very simple:

From the figure above, we can intuitively and simply describe P2P companies obtain gross margin from interest charged to borrowers minus their interest they pay to lenders (cost of funds). Put it simply:

Gross Profit = Loan interest - Cost of Funds

Reminder that loans in P2P lending are given to borrowers without any backing of collateral. This, in my opinion, is one of the main reasons why VC backed P2P lending business is unsustainable in the long run.

Lets have an example of loan interest & cost of funds of a P2P lending company Rupiah Cepat:

A typical 1-month Rp 5.000.000,- loan costs the borrower Rp 300.000,- which is 6% per month. If you annualise it, the interest is 72%.

What about the cost of funds it pays to the lenders?

For a 1-month loan, it pays 13% per annum to the lender.

Put simply, Rupiah Cepat’s gross margin is: 72% - 13% = 59%. On the surface, this seems like a nice margin. Who doesn’t want to be a P2P then? Well, let’s flash out one critical assumption.

Critical Assumption Out of the loans disbursed to the borrowers, 100% (all loans) got paid back on time to the P2P platform with interest. Then you can have the fat margins that we showed.

Now, you might be wondering: who in their right mind would take a loan with 72% per annum interest and pay them back on time? There must be some people failing to pay back their loans, right?

Apparently, on their website, Rupiah Cepat claims that their TKB90 is 100%.

At first glance, wow! This company is awesome that it can make all borrowers pay back their 72% interest p.a. loans on time. However, is this really true? Is there a catch that we are missing out? I think there is.

Why I don’t trust TKB90 figure stated on the website of P2P lending companies

First of all, what is TKB90?

Here’s the definition of TKB90 according to OJK:

TKB90 = 100% - TKW90

TKW90 means: how much loans have defaulted or have failed to be paid back beyond 90 days past the loan’s due date.

However, there is a question remained to be answered regarding TKB90:

What does “penyelenggara P2P Lending dalam memfasilitasi penyelesaian kewajiban pinjam meminjam” actually mean?

If a P2P were to write off its receivable interest, does it get included to TKW90?

If not, this is really problematic because P2P companies are private companies and we don’t have their write off data. They can simply write off debts using VC money to maintain a “spotless” TKB90 figure.

What we know for sure is 100% TKB90 does not mean 0% default a.k.a. gagal bayar (galbay) because of the absurdly high interest charged to borrowers.

By now, we hope you understand that it is impossible to assess the business quality of a P2P lending company without having access to their financial statement*. Data of these private companies are limited and as a result we also cannot trust TKB90 figure.

*In the case of Rupiah Cepat, you could look at their annual report in their website but we find that data is insufficient to make definitive conclusions on the health of the company

If we cannot trust the figure, how do we assess the business quality with limited data? We have a solution.

Using publicly listed companies in Indonesia as case studies to evaluate the health of P2P Lending’s Business Model

One of the biggest benefits of investing in publicly listed companies is that their financial statements are publicly available and audited by third party institutions.

These two companies immediately came into our minds due to their business model similarity to the P2P Lending business:

PT Bank BTPN Syariah Tbk. (BTPS)

PT Adira Dinamika Multi Finance Tbk. (ADMF)

Let’s discuss about the two of them briefly.

The purpose of this exercise is to find out what works and what does not work in order to succeed in the lending business.

Case Study 1: PT Bank BTPN Syariah Tbk. (BTPS)

Bank BTPN Syariah is a tier three Sharia bank in Indonesia providing ultra-micro business loans (branded as “Tepat”) for the un-bankable women population in rural Indonesia, with no collateral (same as P2P lending).

Here are the reasonings provided by the management for some of the questions you might ask:

Why specifically target women? Because BTPS believes that women are more disciplined and more likely to spend their business profits on their families rather splurging on themselves

Why business loans only? Because they are less risky compared to consumer loans i.e. the loans are used to build cashflow generating businesses to pay back the loan with interest

BTPS Loan Interest Rate:

As of 2022, BTPS charges 46% per annum for its loans, which is slightly lower compared to RupiahCepat’s 72%.

Now, where does BTPS get the money to lend to these ibu - ibu ?

Because BTPS is a sharia bank officially recognized by OJK, it is able to collect public funds and store them at low interest rate in the form of time deposit or current account.

There are 2 types of public funds in BTPS:

Mudharabah: acts like a time deposit with a 4% interest rate per annum

Wadiyah: acts like a current account with a 0% interest rate per annum

As of 2022, the blended cost for these 2 funds is 2.9% per annum, which is ~4x smaller compared to Rupiah Cepat’s 13%

So in theory, BTPS’s gross margin should be 46% - 2.9% = 43%, assuming 100% repayment rate.

Case Study 2: PT Adira Dinamika Multi Finance Tbk. (ADMF)

Disclaimer: Adira is one of the companies we invested and we wrote an extensive article discussing its business model and why we invested into this company in this

blog: https://blog.recompound.id/p/recompound-investment-team-admf

PT Adira Dinamika Multi Finance Tbk (ADMF) is a consumer financing company specializing in automotive financing.

It provides financing for the purchase of new / used cars / motorcycles for everyone who are not willing / able to pay lump sum.

Besides automotive financing, Adira also provides consumptive loans where borrowers are able to obtain loans just like in P2P lending, but with a mandatory need to submit a collateral in the form of vehicle ownership certificate (BPKB mobil / motor).

By combining the 2 models, Adira is able to obtain a blended yield of 28% per annum.

Now, where does Adira obtain the money it needs to support its financing business? It is mainly from these sources:

Corporate bonds that they issue to the general public

Joint financing with Bank Danamon. This is possible because Bank Danamon owns 92% of Adira

As of 2022, blended cost of funds from the 2 sources is: 6.79%

So in theory, ADMF’s gross margin should be 28% - 7% = 21%, assuming 100% repayment rate.

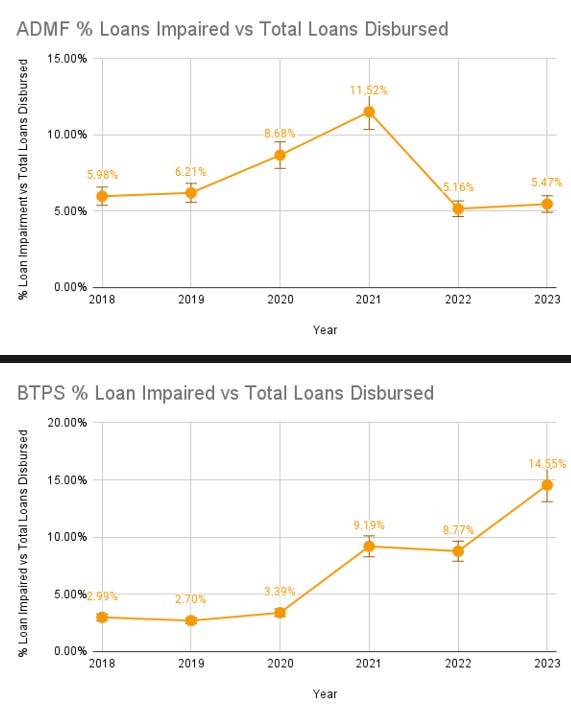

Comparing the 3 Models Together

Now, having this setup, let’s compare the loan quality between BTPS vs ADMF. Sadly no audited loan data for Rupiah Cepat is available 😟

To evaluate loan quality, we use the metric “% Loan Impaired vs Total Loans Disbursed”. This means: out of the loans disbursed, how much of them have been impaired? A loan is impaired when the company thinks the borrower has no chance in paying back the loan.

These are several reasons why, in our opinion, this metric is more credible compared to TKB90:

Writing off a loan from the books means the loan is almost impossible to salvage, hence slashing the company’s asset and earnings, making them look bad to the general public & their investors (remember they are public companies!). Any public companies in their right mind would be incentivised to not impair their loans unnecessarily

These figures have already been audited by third party institutions —> less chance for fraud

Some observations:

ADMF’s loan quality has already recovered from the COVID-19 pandemic and is now doing even better.

BTPS is still unable to recover its loan quality. Even after the pandemic is over, their loan quality is getting worse.

After seeing these 2 figures, you must be wondering:

BTPS’ loans are for productive usage whereas Adira’s loans are for consumptive reasons (buying new cars, motorcycles, gadgets). Hence Adira’s loans should be more risky, right? This turned out to be wrong

BTPS’ having a very low cost of funds does not help

But how the hell does Adira maintain its loan quality so well?

Yep, you guessed it, collaterals!

The importance of collateral in a lending business

If you think about it, a lending business acts like an investor (fixed income manager to be precise):

They aggregate money from a “money supplier”: either a third party / public

Using this money, they perform “investments” by giving out loans and obtain some returns in the form of interest

And in return, the company compensates the “money supplier” with some interest lower than the interest obtained from their loans.

The margin of these 2 interest becomes their gross profit

Having no collaterals attached to the loans means the lending company invests their money with ~0 recourse.

In the investment world, having a large “margin of safety” means: if something goes wrong to the investment, the losses can be minimized.

In lending businesses, collaterals act as a “margin of safety” for the lending company. In the case of a loan default, the lending company is able to seize the borrower’s collaterals and pawn them to recover the loan principal.

A mini simulation of Rupiah Cepat’s business model having no collateral in their loans

To illustrate the importance of having collateral, let’s do a simulation using Rupiah Cepat’s lending business with the following specification:

10 loans, 5 mio IDR principal

1 year tenor

59% loan interest margin, already subtracted with interest paid to lenders (13%)

Borrowers either pay back in full or they default with no payment made

Btw this assumes 0 operational expenditure, we’re being conservative here

Some statistics:

Total money disbursed by Rupiah Cepat: 50,000,000 IDR

Number of defaulted borrowers: 4 (40% of population)

Principal + Return from Interest: 47,700,000 IDR

Total return: -2,300,000 IDR

From here we can easily see that it only takes 40% of population not paying back their loans to make Rupiah Cepat’s business unprofitable. If we account for operational expenditure (salaries, rent, utilities, etc), it is easy to see that the 40% figure should definitely be less.

In the event of force majeur events like COVID-19, percentage of population not being able to pay back their loans would easily skyrocket, damaging their business.

This is why having collaterals is really important to protect the company’s loan principals.

Why VC-backed P2P lending businesses might not work

No Collateral

Having the backing of collaterals from the borrowers minimize the risk of lending business by a huge margin, especially during difficult times like the COVID-19 pandemic.

Now, you might be wondering, why can’t Rupiah Cepat introduce collaterals to their loans just like ADMF’s vehicle ownership certificates (BPKB mobil / motor)? It is not that easy.

ADMF has been in the automotive financing industry since 1991 (that’s 30+ years), and through this long experience it has created a strong business moat of extensive relationships with many automotive dealers across the country.

By using this moat, ADMF can easily pawn the BPKB of a defaulted loan to one of their dealers at a competitive price. The dealer can then resell the used vehicle to a new customer using Adira’s financing plan, providing Adira a new source of income.

Having to submit a collateral is also a self-filtering mechanism to weed out bad borrowers. Because if a borrower already owns a car / motorcycle. They are more likely to come from a better social surrounding, hence having a better probability to payback loans.

Grow, grow, grow

VCs put a lot of emphasis on growth because they need to generate returns for their investors (it is not their fault, but it’s their job). The premise of their investments is that they believe startups should grow exponentially fast. This includes fintech startups in the P2P business.

So when startups are forced to grow at a really fast pace, I think that it is difficult to get really good quality debtors who won’t default easily and abuse the system.

Unfortunately, fancy buzz words and tech jargons like machine learning or artificial intelligence or large language models aren’t really going to change reality. As a matter of fact, I was the data scientist who was responsible for building machine learning models to “evaluate” credit risk of GoTo’s Buy Now Pay Later product, back in the day.

In reality, it is difficult to find high quality debtors at scale. I think the way to solve this is by:

Building a wide extensive network.

Having collateral.

For borrowers: expensive loan interest compared to the competition

As a reminder, Rupiah Cepat’s loan interest is: 72%. ADMF provides the exact same consumptive loan product at 43% interest rate. The borrowers just need to register their motorcycle as a collateral, and the fresh cash will be instantly deposited to their bank account.

There is no reason for any normal person to borrow from P2P lending, unless they do not own a motorcycle.

For lenders: expensive cost of funds compared to the competition

You might be wondering why BTPS and ADMF do not provide 13% interest rate to you as their lenders.

Because they don’t need to!

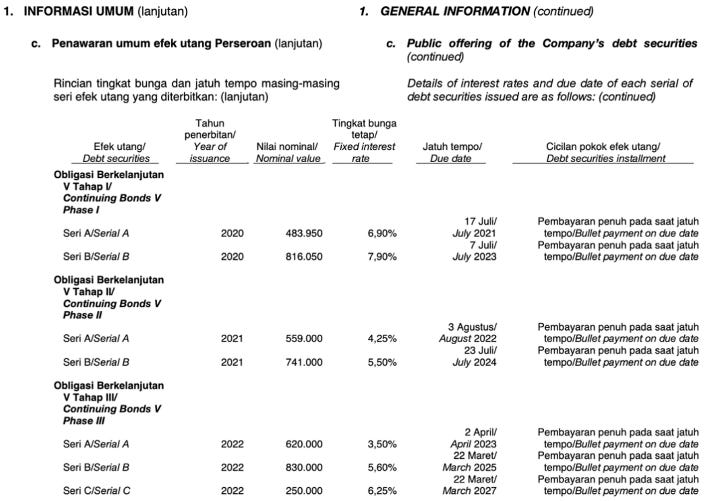

The higher interest rate it needs to give out to lenders, the less profit margin they will get. A case in point, you can take a look at ADMF’s interest bearing debt that is issued periodically to the public as follows.

The interest they pay on the bonds they issue is notably lower. As a result, interest expense can be maintained well.

In the case of BTPS, it is able to obtain an affordable source of funds (because of its status as a sharia bank) to deploy although their loans are currently struggling due to not having collaterals.

But hold on, my P2P investments are insured. My capital should be safe!

Some P2P lending companies for example, Investree integrate insurance to its loans in order to protect its lenders’ capital from downside risks. However, it is not all rosy there.

Here are terms of the insurance, taken from Investree’s FAQ site:

If you read the terms carefully, we know that lenders would get a 75% to 90% of principal that is given out to the P2P company. That sounds safe and reassuring (barring the 25% loss from a supposed fixed income product), but I think there are a couple of points that I’d like to make.

What would happen to insurance coverage if a P2P company stops paying insurance premium?

Insurance companies are businesses. When they enter an agreement with P2P companies with inherent risk, it is reasonable that they would want to limit their payout (claims) as well. I honestly do not think that if a P2P company stops paying its premium, an insurance company would disburse the losses (from defaults) back to the P2P company.

Even if suppose you get disbursement from insurance companies, aren’t you going to use the funds for operational expenditure?

If you need to rely on funds from insurance companies, I think it is likely that there are many defaults that render P2P platforms to be unprofitable. If that is the case, how much funds are you going to allocate to sustain your operations and stay solvent as a company? I think it is reasonable to assume that lenders would eventually get even less cut.

Eventually, it all goes back to the company’s balance sheet.

Is it healthy enough to pay an extra cost (insurance premium) given that:

They have to pay high interest to the lenders

Their borrowers are likely to default if they don’t use collateral?

The politically correct answer is: I don’t know because the loan numbers aren’t public.

My honest answer is: I doubt so.

How would a P2P company solve this unpleasant situation?

I think most probably they will end up shifting to a couple of business models that are different but “adjacent” to P2P. For example:

KoinWorks is coming up with its own digital bank, KoinWorks Neo. https://neo.koinworks.com/en/

Akseleran planned to acquire a multifinance company PT Pratama Interdana Finance (PIF). https://www.cnbcindonesia.com/mymoney/20230704141235-74-451147/akuisisi-multifinance-akseleran-pede-raup-untung-pasca-ipo

Get more external funding from VCs.

Ultimately, the signs are there in saying that players in P2P industry are exploring different business models so that they can have better profitability. We hope that they will succeed.

I have some investments in P2P, what to do?

Talk to your financial advisor. Let us be clear: Not all P2P is bad, just make sure you are aware of the fine prints of the P2P products you buy.

This article is merely my opinion that rests on assumptions I think are valid, but might not be 100% correct. Despite this, I still think that notable P2P companies might go bust in the foreseeable future.