KelaSaham 3 Key Lessons from 6 Years of Stock Investing

Don't read this article if you are into trading instead of investing

Disclaimer: The articles on this page are intended for reference and educational purposes only and should not be considered as recommendations for specific financial or investment decisions. Each individual is fully responsible for their own financial and investment decisions.

Six years might still be a relatively short time compared to senior investors like Mr. Lo Kheng Hong, who has been investing for 30 years, or Warren Buffett, who has been investing in stocks for more than half a century.

We have learned a lot from these successful investors—from how they select stocks, how they manage capital allocation, to how they maintain a long-term view of investing in a company.

Throughout our process of learning and trying to find the right investment style, we’ve had our fair share of ups and downs. These experiences taught us a few important lessons that we’d like to share in this article. The lessons are also meant to be really intuitive and simple conceptually. However, we observe that they are sometimes very difficult to execute in practice and tend to get overlooked by investors alike.

These lessons are summarized into three key points:

1. Buy the Future!

“Never, ever invest in the present. It doesn’t matter what a company’s earning, what they have earned.” – Stanley Druckenmiller

One of the most significant lessons we’ve learned was when we decided to allocate capital to invest in one of Indonesia’s largest tobacco companies, PT Gudang Garam Tbk (GGRM).

That decision was based on a simple rationale: GGRM’s valuation at the time seemed cheap when we looked at its past performance. The company had a market cap of Rp 46 trillion, and based on its historical track record, GGRM was trading at a PE ratio of around 8-9x.

However, what we should have focused on was its future valuation, say 1 to 2 years ahead, while considering its prospects.

After we made the purchase, the company’s performance continued to decline due to shrinking sales volumes, difficulty raising prices in a weakened economy, and squeezed margins from rising excise taxes, along with poor capital allocation decisions made by the management, as we discussed in a previous article.

Only after that mistake did we realize how crucial it is to "buy the future." In hindsight, there were plenty of reasons why we should have avoided allocating capital to GGRM in the first place.

The company’s cigarette sales had already peaked, making future growth challenging. On top of that, the unfavorable macroeconomic conditions and the rise of illegal cigarettes further compounded the problem.

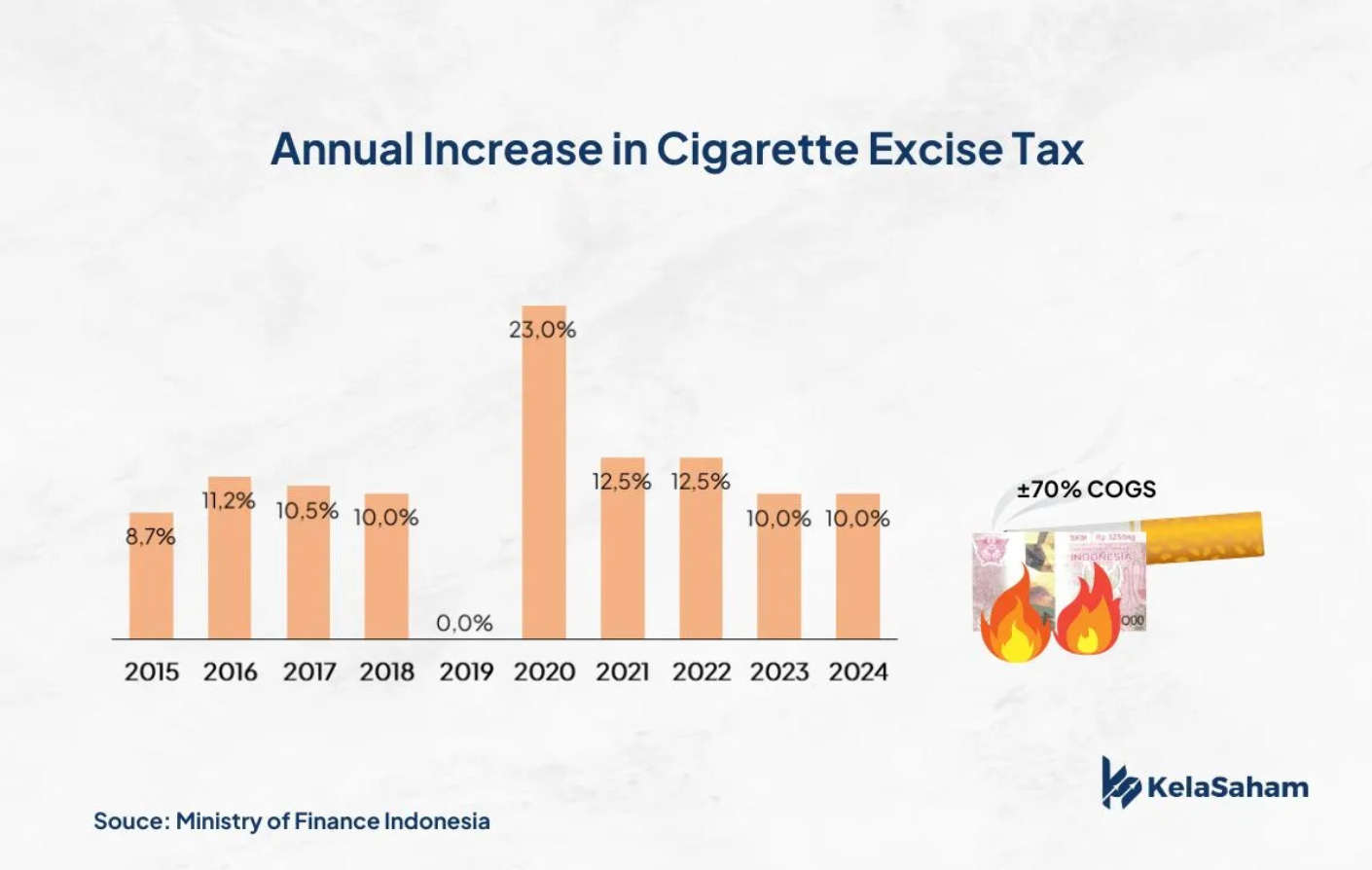

Their biggest cost, excise taxes, kept rising as the government hiked rates, further squeezing the company’s margins because they couldn’t pass on the full cost to customers.

For context, excise taxes make up the largest component of a cigarette company’s cost of goods sold (COGS), accounting for up to 70% of their production costs.

The significant cost of excise taxes has also fueled the growth of the illegal cigarette market. Since illegal operators evade paying taxes to the government, they can sell their products at lower prices, attracting many customers to switch to illegal cigarette.

Internally, the controlling shareholders also allocated capital to unrelated ventures like airports and toll roads, both of which are capital-intensive and typically take a long time to generate returns.

For GGRM we invested a huge amount of money and making this mistake is very costly to us, however, we managed to learn more about investing precisely because we made this huge investment

2. High and Stable Return on Capital (ROC)

“The ideal business is one that earns very high returns on capital and that keeps using lots of capital at those high returns. That becomes a compounding machine.” – Warren Buffett

Return on Capital (ROC) refers to the return generated from the capital invested in the business. The higher the ROC, the quicker we, as investors, can recoup our initial capital.

For instance, if we invest in government bonds with a coupon yield of 7%, it would take 14 years to get our money back (100/7 = 14 years).

However, if we invest the same amount in a company that generates a 7% yield, where that return is reinvested 100% and continues to generate the same return long-term, we would get our capital back in just about 10 years (thanks to the Rule of 72), which is 4 years faster. If the company generates a higher return, we’ll get our capital back even quicker.

It’s important to note that the key here is not just having a high ROC, but it must also be stable. If ROC is high only for one year, it’s likely not due to the company’s core business performance—it could be because of one-off events like asset sales, subsidiary divestments, or non-recurring financial gains.

Not many companies fall into this category. After analyzing over 100 companies, we found that only a few could consistently maintain an ROC of over 15% in the long term.

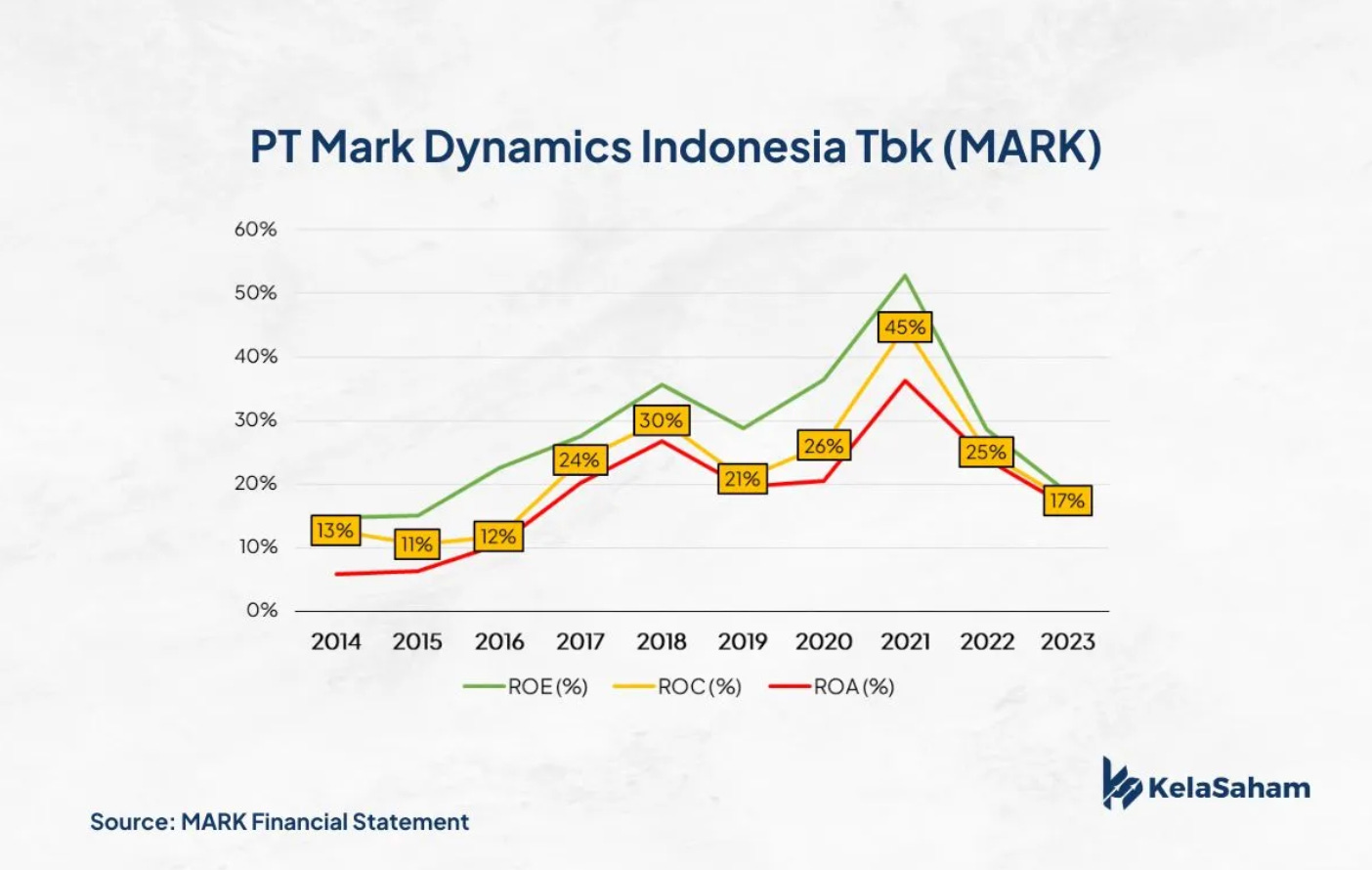

One company that fits this category and has made it onto our investment watchlist is PT Mark Dynamics Indonesia Tbk (MARK).

At the time, MARK reported weaker performance as its profits declined significantly from 2021 to 2023 due to an oversupply of nitrile rubber gloves, caused by the surge in demand during the pandemic. We were confident that once supply normalized, demand would stabilize as rubber gloves are essential to the healthcare industry. Unfortunately, we didn’t make the purchase when the stock price dropped, missing a golden opportunity.

The next question is, “How can we identify companies with high and stable ROC?”

That’s where our role as investors comes in to learn how. At KelaSaham, we’ve developed a comprehensive analytical framework to help identify companies with high and stable ROC. Feel free to visit our program section

3. Cheap Valuation

“On the margin of safety, which means, don’t try and drive a 9,800-pound truck over a bridge that says the maximum capacity is 10,000 pounds. But go down the road a little bit and find one that says maximum capacity is 15,000 pounds.” – Warren Buffett

Margin of Safety (MOS) is achieved when we buy a stock at a price significantly below its intrinsic value, with the aim of safeguarding ourselves from human error, bad luck, or the unpredictable pace at which the world changes.

MOS provides a “cushion” because investing inherently involves risk and incomplete information. It’s impossible to predict the future with absolute accuracy.

By purchasing stocks with a MOS, we give ourselves some margin for error in the face of this uncertainty. Another key lesson we’ve learned is that when a company’s future prospects are bright, combined with a high and stable Return on Capital (ROC), its current valuation will likely include a built-in MOS.

So far, before making an investment decision, we always consider MOS. What kind of MOS does the company offer? How large is the MOS?

That said, we’ve also made mistakes in assessing the fair value of a stock. A prime example is GGRM, which we discussed earlier. What we thought was a sufficient MOS turned out not to be enough because we were too focused on assessing the company’s past performance instead of its future potential. This mistake eventually led us to realize a loss on our GGRM investment.

Therefore, beyond identifying companies with bright prospects and high, stable ROC, it’s also critical for investors to accurately assess the fair value of the stock they intend to buy.

What we’ve learned over the past six years has made us realize the importance of evaluating a company’s prospects. These prospects should not only be assessed on a quarterly basis but also from a long-term perspective.

If you can clearly see promising prospects for a company, you should pay closer attention because there lies the potential for rewarding returns. However, it’s essential to strike a balance between strong prospects and an attractive price.

Without that balance, the returns you achieve will likely fall short of being truly satisfying.

| A guest post by

|