Hi 👋 welcome to Recompound Blog - The Investment Mindshift. We help you better your mindset on investment and economics one article at a time. More: Our Values | Advisory | Get to know us | Picks

Warning: disturbing content is shown in this article. Reader’s discretion is advised.

In case you missed it, head over to slippery slope article which is a common logical error that usually fuels erroneous and fearful arguments on people’s dinner table. Also trying something new this week, which is polls.

Fear sells. Browse social media or tune into market chatter today, and you’ll find no shortage of commentators warning that “another 1998” is around the corner. These fear-based influencers draw parallels between the late-90s Asian Financial Crisis and current events, stoking anxiety that Indonesia might relive that nightmare.

It’s true that volatile currency moves or economic dips can evoke flashbacks of 1998’s turmoil. And to be fair, the 1998 crisis was multi-causal and incredibly complex – a perfect storm of economic and political factors.

This article won’t cover every nuance, but will focus on the key contributing factors behind the 1998 meltdown, and examine whether those conditions exist today. In doing so, we’ll separate grounded facts from fear-driven fiction.

The goal of this writeup is a thoughtful, confident (but never arrogant) look at whether history is set to repeat – or if Indonesia is better prepared this time.

The 1998 Crisis: A Perfect Storm

In 1998, Indonesia experienced one of its darkest economic episodes. The Asian Financial Crisis brought the nation to its knees: the currency collapsed, banks failed, and the streets erupted in unrest. Shops were looted and fires burned in Jakarta as ordinary people panicked.

What made this crisis so severe? It turns out it was the result of several factors coming together – a “perfect storm” of policy missteps and vulnerabilities feeding on each other.

Let’s break down the key triggers that led to the meltdown.

The Collapse of a Currency Peg

One major trigger was the free-fall of the rupiah. For years before the crisis, Indonesia had effectively pegged its currency to the US dollar, keeping the rupiah in a tight trading band.

This fostered a false sense of security. Businesses gorged on U.S. dollar loans, confident the rupiah’s value would remain rock-solid. In the early 1990s, with the rupiah stable and domestic returns high, Indonesian companies racked up huge foreign debts – much of it short-term and unhedged against currency risk.

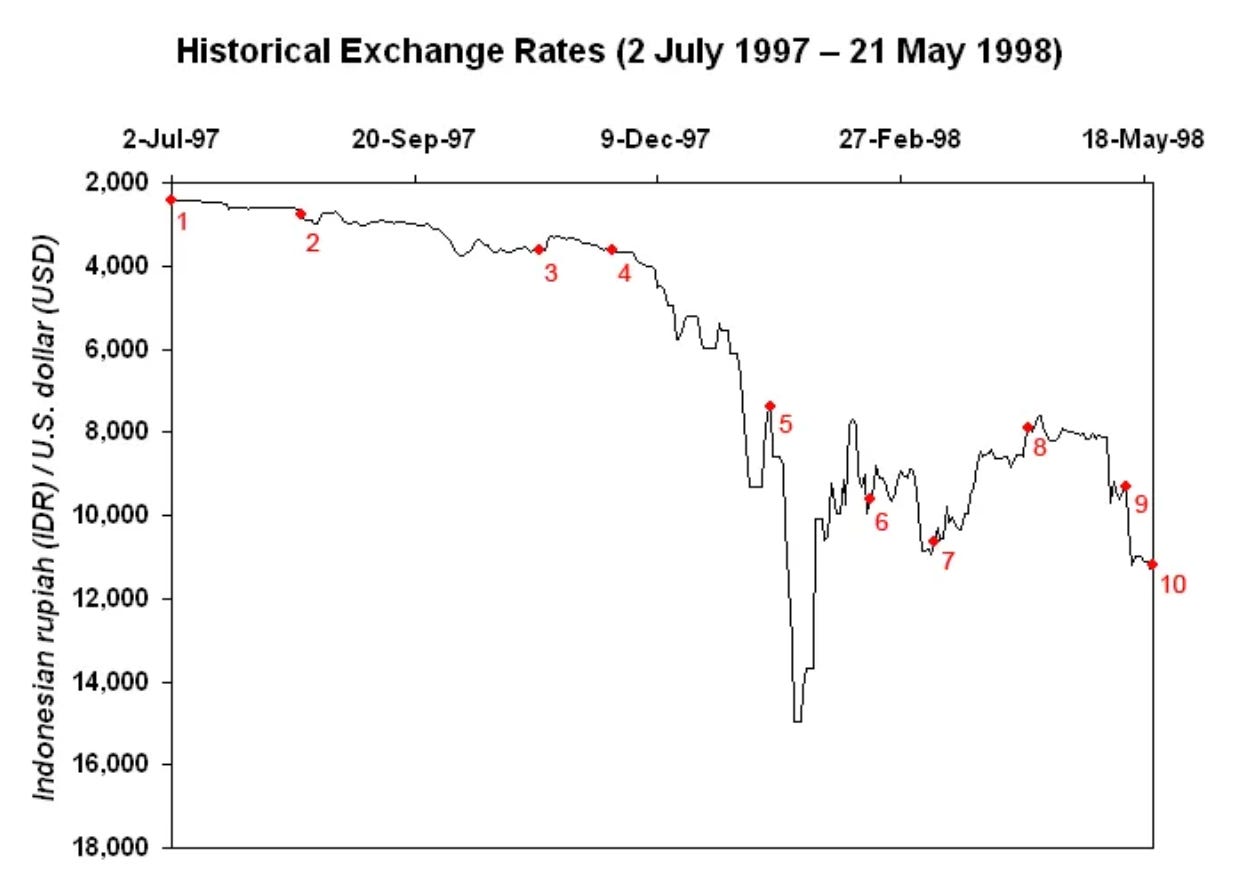

By end of 1997, Indonesia’s external debt had ballooned to around $140 billion (about two-thirds of GDP), a significant chunk of it due within a year. This was a ticking time bomb. When Thailand’s baht devaluation in July 1997 sparked regional contagion, Indonesia’s overvalued rupiah became a prime target. Foreign investors pulled out en masse, and confidence evaporated. The rupiah plunged over 80% against the dollar within months – tumbling from roughly 2,400 per USD to around 14,000 at the peak of the panic. Such a drastic collapse meant any company with dollar-denominated debt saw its debt burden skyrocket in rupiah terms, pushing many toward insolvency.

To make matters worse, Bank Indonesia hiked interest rates sharply in a desperate attempt to defend the currency and stem capital flight. At one point, interest rates soared into the high double-digits, even above 50% – a move that crushed local businesses and banks by making domestic loans prohibitively expensive. In short, a brittle currency peg, once broken, wreaked havoc: the rupiah’s crash inflated debts, strangled credit, and set off a wave of corporate failures. (sources: imf.org factsanddetails.com)

Fragile Banks and Insider Lending (Pakto 88)

Even before the currency crisis hit, Indonesia’s banking sector was dangerously fragile. A decade of loose regulation had sowed the seeds of disaster.

In October 1988, the government introduced a deregulation package known as Pakto 88 (Paket Oktober 88) that made it absurdly easy to start new private banks. The required minimum capital was set at just Rp 10 billion (around USD $5 million at the time) – effectively an open invitation for anyone with means to open a bank. And open banks they did: by the mid-1990s, Indonesia had around 240 commercial banks, nearly double the number from a few years prior.

Many of these were owned by politically connected businessmen (the Southeast Asian “godfathers” that writer Joe Studwell chronicles), who often treated the banks as their personal piggy banks. Credit was dished out recklessly, frequently to the banks’ own shareholders and their pet projects.

This insider lending boom led to a veneer of rapid growth – but beneath the surface were piles of bad loans waiting to go bust.

By 1997, cracks were already showing: some banks were technically insolvent, carrying non-performing loans that they tried to hide with creative accounting. The banking system was undercapitalized, poorly supervised, and ripe for trouble.

When the rupiah collapsed and borrowers could no longer repay their dollar loans, these weak banks were the first dominoes to fall. Liquidity dried up and bank runs began as depositors lost trust. The government initially closed 16 small banks in November 1997, hoping to stem the bleeding, but that actually spooked the public into thinking all banks might be unsafe.

By early 1998, the banking crisis was in full swing – a multitude of banks failing or being bailed out. In essence, Pakto 88’s well-intended deregulation had backfired disastrously: too many banks, too little oversight. The party of easy credit ended with a massive hangover, and taxpayers later footed the bill for a ~$50 billion bank bailout. (sources: kabar24.bisnis.com idntimes.com imf.org).

The Snowball into Socio-Political Crisis

What began as an economic collapse quickly spiraled into something much bigger. The crisis was complex and self-perpetuating: a collapsing rupiah revealed deep banking vulnerabilities; financial panic was amplified by poor policy decisions; panic gave way to widespread unrest; and political instability, in turn, worsened the economic free fall. It was a full-system failure.

By the close of 1998, the economy had contracted by a staggering 13–15%. The rupiah, once trading at Rp2,500 per dollar, had devalued to between Rp8,000 and Rp10,000. Inflation reached nearly 70%, and millions were pushed into poverty. By every metric, it was the most devastating economic crisis in Indonesia’s modern history

As inflation surged and unemployment soared, the financial crisis morphed into a socio-political breakdown.

Public frustration reached a breaking point. After more than 30 years under Suharto’s rule, trust in the government had completely eroded. Nationwide, mass protests and riots broke out—fueled in part by racial scapegoating.

In May 1998, following days of unrest and the tragic killing of student demonstrators, Suharto stepped down, marking the end of an era — and for those who lived through it, the scars remain, along with a deep sensitivity to any signs of history repeating itself.

2025: Why It’s (Hopefully) Different This Time

Given that grim history, it’s only natural to ask: Could it happen again?

The honest answer is that today’s conditions are dramatically different from 1998’s. Indonesia spent the past two decades learning hard lessons and building defenses.

Let’s compare some fundamentals from then versus now, with a data-driven approach:

Healthier Foreign Exchange Reserves & Exchange Rate Regime

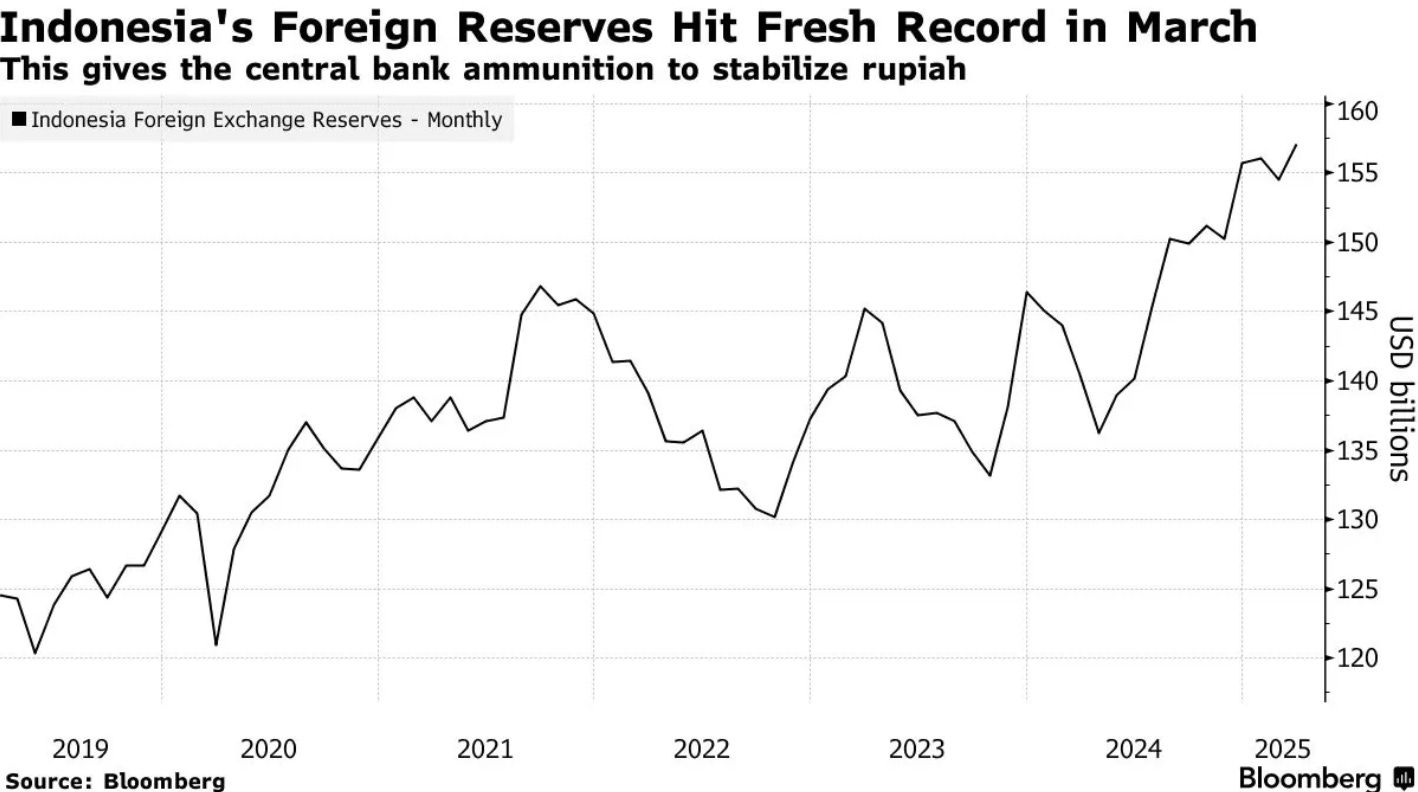

In 1997, Bank Indonesia’s war chest of forex reserves was about $20 billion – not nearly enough to withstand sustained speculative attacks.

Today, reserves hover around $150 billion , a level that provides a massive buffer against external shocks. This alone is a game-changer. It means the central bank can smooth out volatility in the rupiah without quickly running out of ammo.

And speaking of the rupiah, Indonesia no longer maintains a rigid peg like it effectively did in the 90s. Since the early 2000s, the rupiah has been on a free float system.

Yes, Bank Indonesia still intervenes to prevent extreme swings, but there’s no unsustainable promise to hold a fixed value. The currency is allowed to find an equilibrium that reflects market reality.

The result? Recent episodes of rupiah weakness have been nowhere near the chaos of 1998. For instance, during global volatility in 2024, the rupiah did depreciate – even hitting ~Rp16,600 per USD at one point – but policymakers calmly managed it and the rupiah gradually.

Officials have been quick to point out that the nature of the pressure is different: today’s rupiah moves are largely driven by temporary global sentiment (stronger US dollar, etc.), not a reflection of Indonesia’s own economic health.

Indeed, compared to many peers, the rupiah’s depreciation has been relatively moderate and orderly. In 1998, by contrast, the rupiah’s collapse was a sudden free-fall fueled by a loss of confidence in the country’s fundamentals.

Bottom line: a speculative attack on the currency would face a much stronger defense today, and a floating exchange rate acts as a safety valve that didn’t exist in the 90s. (source: jombangnews.co.id)

Healthier Banking System

Perhaps the biggest improvement since 1998 is the strength of the banking sector. Post-crisis, Indonesia undertook major financial reforms. Dozens of weak banks were merged or closed, and surviving banks were recapitalized.

An independent regulator (OJK – Otoritas Jasa Keuangan) now oversees banks, and Bank Indonesia itself was made more independent and focused on safeguarding stability. The difference is stark: Back then, many banks were essentially walking zombies – undercapitalized, drowning in bad loans, and kept alive only by opaque support.

Today, Indonesian banks are much better capitalized and regulated. As of early 2024, the average Capital Adequacy Ratio (CAR) of banks stood around 26% – a very comfortable buffer above minimum requirements. (By comparison, global Basel standards often require about 8-10% minimum, so 26% is robust.) This capital cushion means banks can absorb losses far more easily without collapsing. Non-performing loans (NPLs) are also low (around 2-3% of total loans in recent years), reflecting more prudent lending.

Crucially, the era of wild insider lending is largely over – regulators enforce limits on lending to related parties and big debtors, to prevent a repeat of the 90s cronyism. Indonesia also set up a deposit insurance scheme (LPS, established in 2005) to protect depositors up to a certain amount, replacing the blanket guarantees of 1998 with a more sustainable system.

This reduces the risk of bank runs, as small depositors know their money is safe even if a bank fails. All told, the banking sector in 2025 is on far sturdier footing. It’s not immune to stress, of course – banks are exposed to economic cycles – but the likelihood of a systemic banking meltdown like in 1998 is much lower. Even in a severe scenario, authorities now have established frameworks for dealing with troubled banks (from capital injections to orderly resolution) so that confidence can be maintained.

The phrase “too big to fail” was not even in the Indonesian vocabulary in 1998; now, there’s clarity on how to handle such situations if they arise. (source: ojk.go.id)

Healthier Debt Profiles

Another big difference lies in debt profiles. In the late 90s, Indonesia’s external debt (government + private) was huge relative to the economy – as mentioned, about 2/3 of GDP in 1997. Much of that was corporate short-term debt that evaporated when the crisis hit.

Today, external debt in absolute terms is higher (around $400 billion in 2022), but Indonesia’s economy is also much larger now. That external debt is roughly one-third of GDP – about half the relative level of 1997.

Moreover, the composition has improved: a larger share of today’s external debt is long-term (such as 10-year government bonds held by foreign investors, or long-term project loans), as opposed to the hot-money short-term loans that dominated in the 90s. Corporations, having learned from 1998, are also more careful – many have hedging strategies or borrow in local currency when possible.

On the government side, debt is very much under control. Indonesia’s government debt-to-GDP is around 39% as of 2024, which is considered quite prudent (for context, many developed countries are over 60-100%). In fact, Indonesia has a self-imposed fiscal rule (temporarily suspended during COVID, but now reinstated) capping the budget deficit at 3% of GDP, precisely to prevent debt from getting out of hand.

Back in the 90s, the government’s debt was relatively low before the crisis, but exploded afterward due to bank bailouts. Now, with healthy debt levels and better tax revenues, the government has fiscal room to maneuver if a crisis hits – they can spend to stimulate or support banks without immediately wrecking the national balance sheet. Another aspect is the current account balance – in the 90s, Indonesia often ran a current account deficit (meaning it relied on foreign capital inflows to finance growth). These days the current account is much closer to balance (small deficit or surplus in recent years), reducing reliance on volatile foreign funding.

All these factors make the country much less vulnerable to a sudden stop of capital. It’s like the difference between someone with high-interest credit card debt and no savings (1998 Indonesia) versus someone with a reasonable mortgage and a solid emergency fund (2025 Indonesia). One is far more likely to get into a debt spiral if income falters. (sources: imf.org macrotrends.net ceicdata.com)

Better Monetary Policy Tools and Crisis Management

In 1997-98, policymakers were caught wrong-footed, partly because they lacked the tools or institutional framework to respond effectively. That has changed. Bank Indonesia now has a clear mandate to maintain stability (inflation targeting is in place) and a more flexible toolkit. The bank can adjust interest rates proactively (not just defensively) and use macroprudential measures (like reserve requirements for banks) to cool or stimulate the economy as needed.

Importantly, the central bank and government have established protocols for crisis mitigation. For example, Bank Indonesia routinely states that it will intervene in currency and bond markets to smooth volatility, and it coordinates closely with the Ministry of Finance on maintaining market confidence. In late 2022 and 2023, when global rate hikes put pressure on emerging markets, Indonesia was able to proactively raise its interest rates, use its reserves to stabilize the rupiah, and even deploy bilateral currency swap lines – all without panic.

Contrast that with 1997, when policy responses were often delayed, reactive, and undermined by political interference. Another vital improvement: transparency. Indonesia’s economic data is now more transparent and timely, and the government openly communicates its policies, which helps prevent the rumor mill from spiraling out of control (unlike in 1998, when misinformation and lack of data fueled fear). Finally, institutions have been strengthened – for instance, an independent Financial System Stability Committee now exists to coordinate responses if financial stability is threatened, a mechanism born directly out of the lessons of 1998.

In sum, the pillars that held up the 1998 crisis (a rigid currency peg, rampant unhedged foreign debt, flimsy banks, and a governance vacuum) have either been removed or vastly reinforced. Indonesia in 2025 is certainly not perfect – it still has areas to improve (for example, boosting exports to reduce reliance on certain capital flows, or improving tax collection for more fiscal space). But it’s a far cry from the precarious position of the late 90s. A repeat of 1998 would require a similar constellation of vulnerabilities, and those just aren’t present to the same degree.